November 2012 will be remembered by Australian sunlovers for two noteworthy events: 1) a solar eclipse visible across most of Australia, and 2) the month cumulative Australian PV installations reached 2 gigawatts (GW) (equivalent to 2,000 Megawatts or 2,000,000 kilowatts).

This threshold has been reached in previously only-dreamed of rapidity, and has been paradoxically accellerated rather than decelerated by the removal of government incentives. (Politicians take notice, there are tens of thousands of solar voters in your electorate.)

Take, for example, the case of Queensland. The graph below shows Clean Energy Regulator data released this time last year (red dotted lines), compared with the finalised figures once all installations were accounted for (solid red line), compared with installations registered so far this year. A few things are noteworthy: 1) July-December 2011 were very steady, at comparably low levels; 2) installations in January-June 2012 were significantly greater than at the same point last year, even before all installations are accounted for. So what led to these conditions, and how is this relevant to today?

Well, last year’s reduction in solar multiplier (from 5x to 3x) set off a significant surge in installations, which pulled forward customers that might have otherwise bought in an orderly fashion, plus many that might never have bought solar but wanted to maximise their use of available government incentives. In the first half of this year, Queenslanders began to suspect that soon-to-be-Premier Newman would axe the feed in tariff – this suspicion alone was sufficient to cause people to start people buying, then this year’s multiplier reduction (from 3x to 2x) accelerated the market. Fearing an overheated market, Premier Newman confirmed Queenslander’s suspicions and slashed the feed-in tariff, but not before nearly 100,000 people had applied for it.Such behaviour plays out internationally as well as locally (witness SA, VIC, WA, and NSW), and can be easily understood in terms of human behaviour. Most people are happy to wait for a better deal, knowing that PV prices are likely to continue to decline. However, when governments remove incentives, people will act very quickly to ensure they get the best possible deal. The nature of the SRES and state feed-in tariffs has been for steep step-declines in incentive levels that have in all likelihood resulted in more PV installed now than might have otherwise been the case.So today’s 2GW milestone should not be taken as evidence that no further support for PV is needed; to the contrary, PV retailers in many states are struggling to re-write business models to accommodate lower volumes now that the second-last boom has bust. There will be much less work once the backlog of Queensland systems are installed, and

SunWiz/Solar Business Services’ Forecast suggest 2013 volumes may only be half their 2012 level (predicted to exceed 900MW this year), with South Australia (the only major state with a reasonable feed-in tariff) to eliminate its tariff in Q3 2013. Today’s milestone provides evidence of the need for a smarter way to gradually and incrementally reduce PV support in line with market conditions, rather than causing another bust by creating an incentive-reduction boom.

This is important in today’s context. The Climate Change Authority is seeking a way to contain SRES costs (SunWiz was honoured to be invited by the CCA to represent the PV industry at its RET Review roundtable). We have argued that the solar booms have been caused by tariff and multiplier reductions which have (finally) almost played out, but the CCA is still fearful of an overheated PV industry acting to impact on retail electricity prices (even while it acknowledges that the impact is offset by a near-equivalent reduction in wholesale electricity prices). However, the main problem with the CCA’s proposal to apply a solar ‘divisor’ to the entire system capacity (not just the first 1.5kW) is that it will need to be fore-communicated by the minister well in advance so that the PV industry can advertise updated pricing to new customers.

The minister will need to guess at the level of divisor required to ‘tame’ the industry, even when the market conditions shift faster than the minister can respond. The reduction but is likely to be infrequent and thus aggressive (without any ability to undo the divisor). History has proven that, given this warning of steep reduction in incentives, demand for PV will spike, creating an installation rush followed by a bust.To avoid this scenario playing out, what is needed is a more gradual adjustment – some ideas being considered by the industry include the STC price (which would behave differently if the SRES had a soft, rolling annual cap), or annually reducing the deeming period from 2016 to coincide with the RET’s end in 2030. We would prefer there to be no change to SRES, particularly because SRES’s contribution to electricity prices has peaked; but if a change must be made, the entire industry would prefer to avoid a perpetuation of the boom-bust that plays out when a steep reduction in incentives occurs. We have written to the CCA arguing that small-commercial PV is unlikely to materially impact electricity prices and should be retained within the SRES, that perpetually adjusting incentives to push paybacks beyond 10 years will leave nobody to maintain systems or meet warranties on existing systems, and that the solar divisor is a blunt instrument that will be counterproductive.

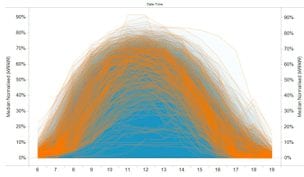

Whatever happens, there must remain an incentive to use accredited product and installers, and to register systems so we can bring you good news like today’s. For with 2GW on the grid, PV now has a material impact upon the electricity market (in which 25-50GW of generation may be active at any time). To successfully operate the market, the Australian Electricity Market Operator (and its participants) need detailed understanding at 5-minute intervals of the volume and performance of PV.

Warwick Johnston is director of consultancy group Sunwiz, which tracks PV performance, how much PV is connected to the grid, and the relationship between deployment and government incentives. And Warwick will be watching the impact this month’s solar eclipse has on solar panels across the nation (and the eclipse’s effect on the solar panel we’ll be taking to the path of totality). How eclipsed will you be? Find out here.