ITK has nothing against the many wonderful plans for offshore wind and green hydrogen in Australia. They potentially offer lots of jobs, investment, exports and and consume many articles on company press releases and web sites.

However, what they won’t do is get us to Labor’s now promised 80% renewable electricity share by 2030. ITK is unsure exactly what the status of the 80% is, but we presume it comes from the ISP “step change”.

Lets have an executive (team) in charge of implementing the ISP

If Chris Bowen wants to talk about the 80% by 2030 target then we need a bureaucrat to be put in charge of it. ITK can even save Bowen the need to engage any head hunters.

Alex Wonhas and Brad Hopkins are the names he needs. Those two, given a bit of authority, could get the ISP executed, plus do all the work of the ESB in a fraction of the time and far more effectively. They would work with the individual states but particularly Queensland, to get the state what it needs to make the ISP happen.

As good as it was to see the equivalent of COAG agree to put an emissions goal into the NEO it made my day seeing how strongly it was endorsed by Mick De Brenni.

However in Queensland, unlike in New South Wales, there is no bipartisan support for current targets and frankly there is not yet explicit policy of any kind. And yet I have no doubt that the federal government and the Queensland government have thought about it a lot.

Let there be wind farms

Back to nuts and bolts.

In theory, by the time we get to 2030 most of the job is done and it will be done by onshore wind and rooftop solar and household – or at least distributed – storage.

Those are the dashboards that should be on every policy maker’s desk every week. What new wind farms were confirmed? How much new rooftop solar was installed? How many household batteries were sold? Are they on target? If not what can we do to make it happen? Would community batteries speed up the household battery uptake? How about communicating meters? Why are we so behind? etc.

It’s not big announcements about offshore projects that won’t be built for a decade. We need to get as much as 3GW of onshore wind done every year.

That growth in renewables from 2022 to 2030 is driven very largely by growth in wind and rooftop solar. Yet outside of NSW and the federal SRES scheme there is no clear policy that investors can rely on.

Perhaps that is a bit harsh, in that the federal government’s transmission funding could increase confidence in Marinus Link going ahead, and it’s likely that – rightly or wrongly – commercial pressure will see HumeLink Sydney reinforcement and VNI West progressed.

Within NSW, the state government will make the transmission from New England and Orana happen and the key role of Queensland should see its connections to the rest of NEM as high as they need to be.

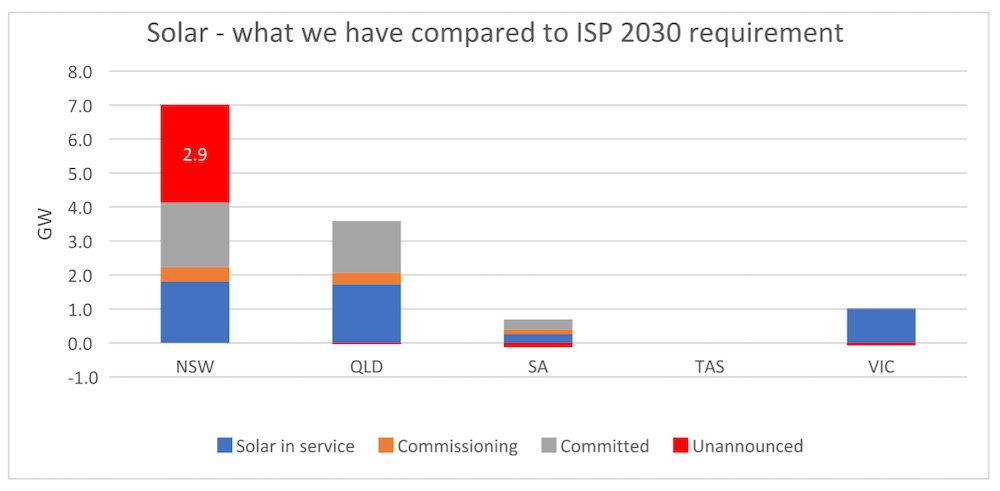

Just as a reminder, the ISP doesn’t have any hydrogen by 2030 and nor does it have any offshore wind. And in fact, outside of NSW, the ISP doesn’t project that building any more utility solar farms is a good use of investment dollars prior to the next decade.

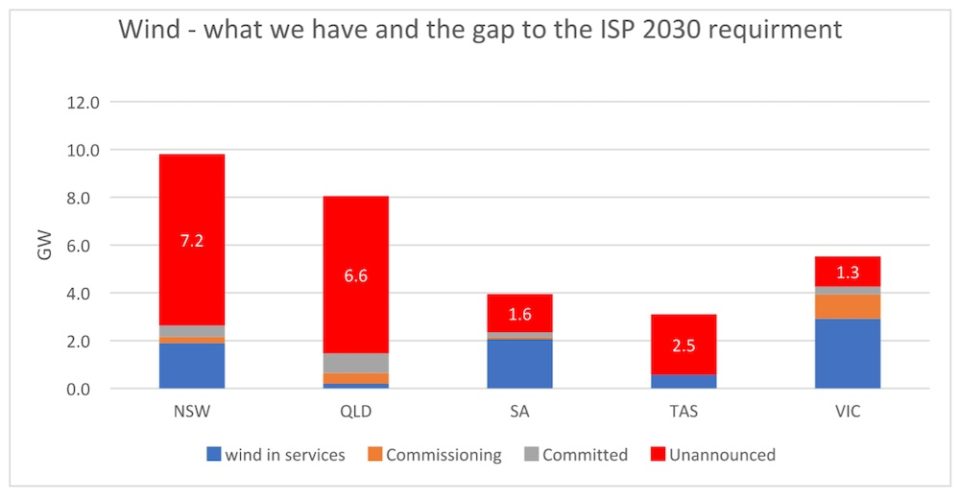

The following two graphs use data from the latest AEMO generation information spreadsheet and “step change” ISP to show the gap between the wind and solar that are both in service and announced compared to what the ISP models to be fully commissioned in the year ended June 30, 2030.

In the case of wind, it can be seen that the ISP calls for more in every state. In most states the requirement is larger than what is already installed and/or being built.

The table also shows that the committed pipeline is pretty darn average, with the arguable exception of Queensland. And because NSW has a clear plan and a timetable and process to achieve the plan, they get a pass.

I’d note that the ALP in NSW is fully behind the current government plan, so investors have the confidence that in the event of a change of government next year execution of the NSW plan will proceed unabated.

The data table underlying the graph is:

If you assume that it takes two years to get a wind farm operating from the time final investment decisions [FID] is reached, and that is frankly a little optimistic these days, then all of that 19GW has to be announced over the next six years or a bit over 3GW per year, every year. And, actually, it’s not like 2030 is the end of things.

Queensland has the most to do, but equally doesn’t need the transmission. Tasmania has a lot to do for a state of its size, but nothing can really happen there until Marinus Link is built.

You don’t have to be much of a desktop warrior to appreciate that getting the supply chain organised is a big deal. It’s not like Australia is the only country doing this.

Why not let Europe have its offshore wind turbines and we can get on with the humble job of building onshore wind using, say, 5MW turbines. We only need about 4000 of them and there probably are enough boats around to ship them.

Actually, the turbine blades arguably could be built in Australia, but I’m not going there.

Looking at solar, essentially not much is needed on the implicit assumption that there is enough policy around to keep behind the meter growth going at a decent pace.