Times are indeed changing as in Bob Dylan’s famous song, The times, they are a changing. Despite the overall bear market in 2015, high tech virtual companies grew at rates much faster than the more traditional companies of yesteryears as illustrated by the top 10 most valuable companies in the US (accompanying chart). Two things stand out immediately:

- First, 5 of the top 10 most valuable US companies, defined by their market capitalization at the time, are virtual, high-tech companies. Alphabet, the new parent of Google and Facebook, arguably do not produce widgets or products but are engaged in providing information, in the case of the former, or a platform for people to exchange information, in the case of the latter. Facebook was not even listed in 2010. Apple and Microsoft, one can argue, produce products, but most of their market value may be attributed to intellectual property and/or their dominant brands. Amazon does not produce anything; it is mostly selling products of others. Its market value is mostly explained by its dominant position as a low-margin middleman.

-

Second, all 5 virtual companies exhibit significant growth since 2000 – certainly by comparison to the other 5. ExxonMobil, once the most-valuable US company, is now in the 4th position. Once mighty GE is 6th—it is the only company still on the 30 companies listed in the Dow Jones Industrial index since it started. Exxon has barely grown in market value in 5 years, understandable given the decline in oil prices.

In reporting the findings, The Wall Street Journal noted,

In reporting the findings, The Wall Street Journal noted,

“US technology shares scaled fresh heights …, fueled by upbeat earnings that renewed investors‘ faith that the giants are solidifying their dominant positions at the center of the Internet economy despite a raft of upstarts.”

The WSJ article said,

“Investors added about $90 billion to the combined market value of Amazon,… Alphabet & Microsoft”

“Gains in the five top tech firms (at the time of the article) account for 15% of the rise in the broad S&P 500 index this (Oct 2015) month.”

The emergence and rapid growth of the new tech titans suggests another structural change taking place not just in the US but across the globe, namely the rise of much heralded information economy popularized by the likes of Alvin Toffler‘s The Third Wave published in 1980.

Long before the rapid penetration of the Internet and wireless communication revolution, Toffler predicted that humanity is entering a third phase of development with implications far more profound than the prior two: the dawn of domestication and agriculture followed by the industrial revolution. Recent developments, including the rise of the hi-tech titans, prove that Toffler‘s vision was spot on.

Manufacturing giants, multinational conglomerates, major energy companies, global banks and investment companies are still big, profitable and important. But those that gather, manage, control and manipulate information are apparently even more so. And this is beginning to dawn on the traditional firms that what increasingly matters is not the nuts and bolts or the gadgets but who is managing the information that runs the devices, the gadgets and the machines. Commodities and energy still matter, but perhaps not as much as they did, especially if future demand is less robust than previously assumed.

Take, for example, car manufacturing. Traditional car giants like Daimler Benz, GM and Toyota have belatedly discovered that manufacturing cars, as important as it is, will not be the most profitable part of the business. As future ―cars‖ become software-defined and increasingly software driven, companies that deliver data, manage information, and control devices stand to gain dominance and advantage. Manufacturing the bodies and assembling the pieces will become low-margin chores. Consider the following:

- Uber‘s latest valuation at $64.6 billion exceeds that of GM (graph below);

- Airbnb, which does not own a single room, is worth more than Marriott, which owns or manages more than 300,000; and

- The reservation system of major airlines, such as American Airlines, is worth more than the airline itself.Hi-tech unicorns, as they are sometime referred to, are enjoying gravity defying valuations partly because lots of venture capital money is chasing few potentially big hits, but also because there is genuine belief in the value of services they offer, if not today, perhaps in the future assuming they grow to a position of dominance in their market niche.

In an Op-Ed in the 29 Dec 2015 issue of The Wall Street Journal titled Shrinking tech means room at the top, Andy Kessler writes,”On Dec. 29, 1959, the physicist Richard

In an Op-Ed in the 29 Dec 2015 issue of The Wall Street Journal titled Shrinking tech means room at the top, Andy Kessler writes,”On Dec. 29, 1959, the physicist Richard

Feynman delivered a famous speech at the California Institute of Technology titled ―There is Plenty of Room at the Bottom.” He predicted almost limitless possibilities if we could “manipulate and control things on a small scale.” He nailed the next five decades of ever- shrinking realms that ultimately produced trillion-dollar markets in microelectronics, nanotechnology and bioengineering through DNA-level manipulation”Kessler asks,

“Now what? We‘re 16 years into the 21st century without any clear map of the world ahead”

This editor‘s take on Feynman‘s prediction of what happened to the plenty of room at the bottom is that at last count, 144 startups, most of whom did not exist 5 years ago, are now worth at least a billion, at least on paper (chart on page 15). That

This editor‘s take on Feynman‘s prediction of what happened to the plenty of room at the bottom is that at last count, 144 startups, most of whom did not exist 5 years ago, are now worth at least a billion, at least on paper (chart on page 15). That

suggests plenty of room at the bottom.

As for Kessler‘s ―Now what?‖ the answer is that Feynman, like Toffler and countless others attempting to predict the future or the next wave, was simply ahead of his time.

What are the implications of the information technology revolution for the energy sector? The most important may be that advanced economies of the world will increasingly grow not so much by the growth of their traditional manufacturing and energy-intensive sector but rather by the innovations of their information sector. Obvious, you might say?

This may also suggest that, while manufacturing will remain critical, the

service sector, especially the information sector, will become the engine of growth and prosperity for the future.

The information sector uses lots of energy, electricity in particular, but produces disproportional wealth per unit of energy compared to traditional energy-intensive industries of the past.

These trends, more than many realize, explain why advanced economies of the future will be able to sustain reasonable economic growth and prosperity while using ever smaller amounts of energy in aggregate.

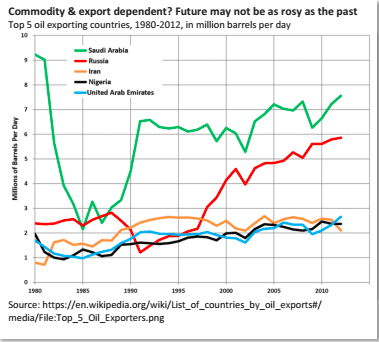

Countries like Saudi Arabia, who are totally dependent on exporting oil, according to this line of reasoning, are in for rough times. Others like Australia, who have historically generated tremendous wealth by simply digging stuff out of the ground and loading it into ships destined for China, will also have to make adjustments. Ditto for province of Alberta in Canada, and countless others.

Add increased pressures to cut carbon from fossil fuels, and eventually fossil fuels themselves, and one can clearly see the writing on the wall.

Perry Sioshansi is president of Menlo Energy Economics, a consultancy based in San Francisco, CA and editor/publisher of EEnergy Informer, a monthly newsletter with international circulation. He can be reached at [email protected]