Sometimes assumptions in official documents are questionable and so too are the conclusions. In this latest document from the Energy Security Board – the “final decision” paper on the National Energy Guarantee -there is a big emphasis on price outcomes.

We hate to say it but there seems to be an agenda at work. In most important documents there are rarely obvious errors.

This latest ESB document (see it in full here) includes some strange results. We note the ESB has neither officially released the document, even though it’s in all the press, and perhaps more importantly it hasn’t released the ACIL Allen modelling report cited within.

The document states that

There is a less than 1% of total Australia wide emission reductions as a result of the NEG, or indeed even if there isn’t a NEG. The extra emission reduction as a result of the NEG compared to a no NEG policy are 4 mt. Giddy up.

If there is no NEG the analysis claims there will be no new large scale generation between 2022 and 2030. Just rooftop PV. Hands up if you believe that, because I have a Harbour Bridge you might like to buy. We would argue that a “strawman” has been set up to justify the conclusions, but we do respect that ACIL Tasman is a noted modelling firm and widely respecting. We just don’t agree with the conclusions. We think they are at odds with history and economics.

If there is a NEG, NEM wide pool prices will be between $40/MWh and $50/MWh from 2022 to 2029. That’s despite the closure of Liddell. More importantly it’s despite the fact that gas prices are way higher than last time electricity prices were at those levels and right now export coal prices are also much higher. On our numbers, Vales Point and even Eraring will struggle mightily at those prices. Gas generation won’t be running much either. AGL investors will be running for the hills. The document also contains at least one error or a contradiction between the text and the underlying charts.

Sloppy errors result in deeply misleading statement on emissions reductions

“The Guarantee is expected to deliver the emissions reduction target for the NEM, with an additional 38 MtCO2-e abatement over 2020-21 to 2029-30 relative to a scenario without the Guarantee.” Page 23 of the document.

38 mt is about 7 per cent of Australia’s approximately 550 mt emissions, so that would indeed be fantastic.

Unfortunately, the ACIL Allen Chart 9 which accompanies it shows only about a 4 mt reduction i.e. less than 1%. And that’s relative to ACIL Allen’s straw man status quo which we will get to in a minute. The absolute reduction in emissions from FY20 is about 5 mt, still less than 1% of total emissions.

Of course writing 38 mt could be just a sloppy piece of writing, but it has the impact of leaving readers with a very misleading view of the facts. How can COAG rely on this kind of stuff?

The document is big on the stated price reduction results, but very short on providing data or facts to justify them. Both the price reductions and price in the no-NEG scenario are not justified in the document in any practical way. Price is the outcome of supply and demand.

The ESB shows a change in supply graph in the no-NEG “strawman” case. The graph only shows power, that is gigawatts, and not energy. According to this graph there will be no new capacity other than rooftop solar if the Guarantee is not approved.

How credible is that? There has never been a five year period in the history of the NEM with no new capacity. That’s even before we think about potential closures of other stations, State renewable targets or just entrepreneurs taking a punt.

Figure 2 No NEG, No Job for generators. Source: ESB p15, ITK comments

The no new generation forecast comes despite the fact that without the guarantee prices would be rising throughout the same five years, to levels above current wind and solar PPA prices.

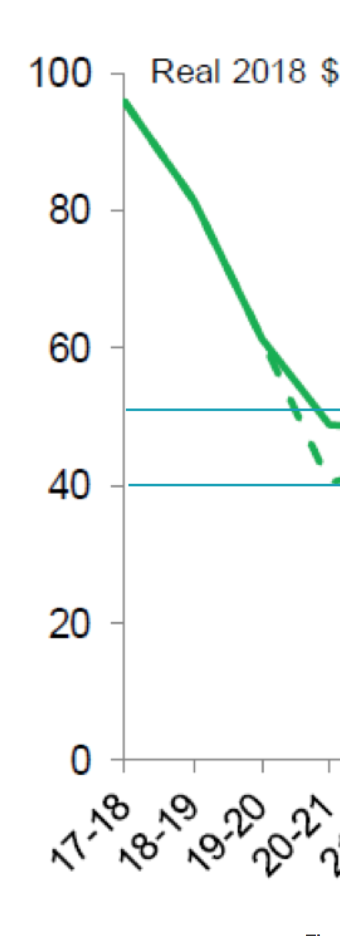

The price forecast charts are wonderful.

Let’s look at the no NEG case first. The following figure is amended by me from ESB’s Fig 3. I’ve blocked out the history, added in some grid lines and added the arithmetic baseload futures average of NSW, QLD and Vic for FY21 and FY22.

Figure 3: Adapted from ESB Chart 3

Figure 3: Adapted from ESB Chart 3

Retailers have to pay above baseload for power. Even so the figure clearly shows that in FY22 Futures are sitting at $10/MWh above forecast and are also above the FY21 forecast.

The futures could be wrong and the modelling correct. Or both could be wrong. I’ve added in red line showing the PPA price for new wind and PV in Fy18, never mind FY23.

Now let’s look at the price forecast with the guarantee. Apparently the price is lower mainly because there is more contracting.

This basically predicts prices between $40/MWh and $50/MWh with the guarantee between 2022 and 2028. The ESB hasn’t let us know what the new supply forecasts are with the NEG.

Let’s look at Vales Point though and bear in mind AEMO says there is an expensive refurbishment due in FY22. The electricity price is forecast to be say $46/MWh average.

Let’s say the coal price that year is $80/t, half the export spot price. Vales Point would then be making on my numbers about $11 m of ebitda.

Goodluck Brian Flannery selling that power station for $700 million, Jeff Dimery at Alinta will be beating the door down I’m sure. I’d question whether you’d do the refurb at all. It would probably just get put off.

The Victorian and NSW State forecasts will also be unpleasant reading for AGL and Energy Australia. We only show Victoria. Seven years of $40/MWh prices will do wonders for Yallourn and LYA profits.

Would you be spending money on reliability capex at those prices. Costs at Victorian brown coal generation have increased quite significantly over the years.

Even leaving aside the strong increase in state royalties that was the final nail in Hazelwood’s coffin you have to remember the coalmines get further away from the power station every year and overburden increases.

Not to mention labour costs. Heres a chart from AGL’s 2016 investor presentation on LYA overburden.

Despite the politics, despite the pain are low prices even a good thing?

Now we’re standing on shaky ground, but we reckon much of the coal generation is going to close by 2035 and that lots of new generation needs to be built ahead of time to manage that.

Low prices of the sort that the ESB is putting forward won’t assist that. Nor will they do anything to encourage energy efficiency or disincentivise consumption.

However, industry will love the ACIL forecasts. Great for data centres and anything energy intensive. The price forecasts are lower than say the actual prices in China in Calendar 2017.

15 responses to “ESB paper: Strange, sloppy results suggest agenda at work”

Brad

Looks like the text box in Figure 3 (the amended chart) needs “No fill” on the text box formatting.

Ben

Just thought I would point out the discrepancy you’ve noted with regards to the 38 MtCO2-e is a misunderstanding between cumulative emissions and annual emissions. As an example, if your annual emissions are 1 MtCO2 for 20 years, your cumulative emissions are 20 MtCO2.

The ACIL modelling and Chart 9 shows the annual emissions, in which the NEG will only save 4 MtCO2-e p.a. by 2030. If you add the cumulative emission difference between NEG and no NEG each year from 2021-2030 you’ll reach the 38 MtCO2-e total figure.

It is important to note that cumulative emissions savings are more important when meeting a carbon budget, which is expressed in absolute tonnage terms, not annual terms.

Peter G

Well pointed out, but the report remains confusing with the graphical representation not aligned with the text. The graph scale is to 150Mt so the text reference to 38 MtCO2-e implies a much larger portion than is actually the case.

Peter G

This type of misrepresentation would be marked down in an undergraduate essay. A kind interpretation might be that the document is intended to be confusing.

David leitch

Thanks Ben

Well worth pointing out. And shows the risk in me using strong language. It will come back to bite me. And I hereby apologise to the ESB. What the text says is correct. That said…

Total emissions in Australia over those 10 years will be something like 5500 MtCO2-e so the 38 MtCO2-e cumulative saving is 0.7% compared to the no NEG case. Assuming the modelling is correct for both cases.

David leitch

Also if I use the modelling target of cumulative NEM wide emissions of 1320 MtCO2- for the FY21-FY30 the reduction compared to the non NEG case is a more meaningful but still small 2.8%.

I note there is an assumption in the graph that the passing of the guarantee will result in emissions falling sharply in the FY20 to FY22 period compared to the No NEG case. I would like to have the logic of that explained to me as the graph shows the investment will be made five years or so ahead of when it is needed by the budget (green line).

The graph and others imply that there will be investment immediately the NEG is approved that would not take place with the NEG, the emissions credits will be banked. That extra investment will be made even though the black electricity price it receives will be lower than if the NEG isn’t approved. If a separate emissions compliance market emerges I guess that could be the case but its not clear to me why investors will rush to do it ahead of their obligation.

Obviously if they don’t make that early investment the cumulative savings are less. I guess I’ll just have to wait for the modelling document to see if further light is shed on the point.

Peter Lyons

David, in your item 1 you mean 4 Mt as in megatonnes, not 4 millitonnes I presume?! 😉

David leitch

million tonnes

Peter G

Thanks David. Such low modeling of future price demands supporting data and assumptions to be credible.

Scott Morrison must have repeated his “NEG MEANS LOWER PRICES” slogan a dozen times this morning…

It brought the Baird to mind

… It is a tale

Told by an idiot, full of sound and fury,

Signifying nothing.

Alastair Leith

Saw a column graph present to ~2030 on the front page of The OZ in the supermarket showing the NEG having a 20% influence over decline of household energy prices. The extra show in Oz Red tone just so you can’t miss it.

I haven’t bought The Oz for well over a decade but I do occasionally notice the cover and I don’t think putting graphs of anything on page one is common practice, so I can only assume the Federal Government MPs media advisors are pushing all out on this fiction that the NEG means cheaper power in order to pressure the states into locking in a protection racket for coal.

I don’t know how they determine what a median or average household energy price is. Does it include houses with PV systems on the roof in the data set?

juxx0r

1mt = 1kg, lucky the ESB got it right with 4Mt because sloppy errors result in deeply misleading statements apparently.

David leitch

Thanks. I’m embarrassed

juxx0r

And it might not come through from me, but you always do really really good work. Thanks for always shining a light on things the way you do.

Alastair Leith

So wherever is happening here is good (see image of years 2017-18 to 2020-21) , why don’t the Liberal Party and their paid in full mining industry reps in the National Party promote extending the RET which non-coincidentally flatlines with no extension of targets in 2020-21, just as the price decline abruptly halts and prices start to increase again.

Open publishing of open models using open source software is the only credible way that these important discussion around policy can be conducted with anything like the scientific rigour that they a) deserve and b) any of the modellers doing this work behind closed doors would probably claim about their work.

How many times have we seen a policy for carbon price mooted by the Government or opposition to have umpteen models of the exact same policy and settings to provide us with umpteen plus one different reports telling us it will mean the end of industry ABC if it is adopted or something equally grandiose? All without a shread of evidence being tabled in public by way of transparent modelling that can be scrutinised by their competitors, independent observers or any individual of the public motivated enough to do so.

Many of the consultancies often involved in this modelling take a lot of money from governments and from industry sources — so can hardly claim spotless independence.

I understand some academics and others may be working towards open source software for energy grids and markets software which can only be a good thing… it can’t come soon enough. The current state of play where a government funded board, the ESB, pays what is likely to be a small fortune for modelling that they don’t release to the public but which the Government of the day then goes out to launch on media campaign on the back of (first time I’ve seen a column graph with red ink on the cover of the Oz in a long time) is nothing short of a policy development disgrace.

In the meantime for modelling generation from renewables and conventional assets on grids made up of interconnections Sustainable Energy Now has released open source SIREN software. Modellers in SEN use a set of excel spreadsheets to run the output of SIREN through merit order dispatch to tweak amounts of capacity deployed so as to optimise generation assets to balance demand and supply and determine system costs, or Levelised Cost of Energy.

Hopefully any OOS we do end up with is user friendly enough (no coding required) so that it will enable NGOs and other less well funded organisations access to these powerful tools to scrutinise the work of others

{kind=link}