Energy Efficiency Market Report – 31st March 2017

Victorian Energy Efficiency Certificates (VEECs)

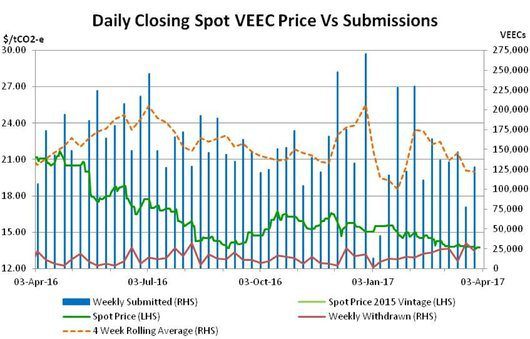

Having lost ground early in the month, March proved a generally stable affair in the VEEC market with forward activity the mainstay and talk of cheaper forms of commercial lighting making up much of the discourse. Whilst VEEC submission numbers have fallen, the VEEC surplus continues to grow.

The spot VEEC market opened the month by softening into the high $13s early on, yet from there stability took hold. Across its remainder, the market was range bound, trading between $13.65 and $14.00 and ultimately ending the month at $13.75, a drop of 3.5% on February’s close.

It was the forward market that captured most people’s attention during March, with large trade volumes particularly for settlements across the second half of the year taking place in the high $13s, often at very similar levels to the spot price.

VEEC supply has moderated across early 2017 but not to the extent that many had expected it to, and not to the extent that it has ceased to remain above the rate of creation that would begin to shrink the large VEEC surplus.

As at the end of January, there were just under 4m VEECs either registered or pending registration above the 2016 target of 5.4m. Ignoring that surplus, the 2017 target of 5.9m requires a run rate of 114k per week. Each weekly VEEC submission figure above that therefore grows the surplus further, each below it would shrink the surplus. Across March, despite the presence of a public holiday week, VEEC submissions still averaged 126k, hence the VEEC surplus has continued to grow.

At the heart of the surge in recent forward market activity appears to be the arrival of significantly cheaper forms of high bay lighting, which some suspect may just be viable for a giveaway model at current pricing. As these new lights are approved and installed there are those who believe that it will yield another increase in VEEC supply in the coming months.

Against this are those that think even if these new lights do prove successful, the natural decline in activity from all other sources owing to the removal of low hanging fruit and the persistently lower VEEC prices will compensate for any increase, with the net outcome being lower overall weekly submission figures.

The numbers are always closely watched, but with 3 weeks in April impacted by public holidays the coming month will prove an interesting one in terms of the VEEC submission rate and its impact on the surplus. It will also yield the 2016 final surrender figure.

New South Wales Energy Savings Certificates (ESCs)

It was a positive month in the ESC market with the price recovering off its recent lows and healthy trade volumes taking place, particularly in the back end of the month.

In the early part of March the spot ESC market continued its downward run which saw it reach a low of $14.80, a level not seen since February 2015. From there the market began a recovery which brought the spot back into the low $16s by mid month and up to $17.35 by its conclusion.

The forward market was particularly busy in the second half of March as the improving prices helping to encourage sellers back into the market. The recovery across March seems in part to be a reflection of perceptions that perhaps the market overshot its mark during the fairly severe downward run across February.

The recovery in March happened despite ESC registration figures remaining high across the period with the 4 week rolling average sitting at 143k, though this was no doubt boosted by several baseline methodology creations that relate to activity across the previous year.

The cut-off for 2016 compliance is looming at the end of April at which point we will know how many ESCs will be surrendered against the 2016 target (expected to be around 3.8m). It appears that the ESC surplus carried forward from the 2015 vintage into 2016 (circa 3.3m) is likely to have grown across the last year, though the final figure will only be know by 30th June when the cut-off for registration of 2016 ESCs occurs.

Whilst the surplus appears to still be growing, the delay between sales, installation and registration means that the current registration figures do not necessarily provide a timely indication of conditions on the ground at present. There are those who argue that the fall in price across the early part of 2017 will lead to a reduction in supply sometime around the middle of the year, an outcome that will be closely watched for.

Late in the month the 2016-17 ESS Rule changes were gazetted. As always the update included a range of very technical changes to multiple creation methodologies. At first glance the only changes with the potential to have some impact on supply are the changes to the Home Energy Efficiency Retrofit program aimed at encouraging activity in the residential and small businesses sectors, though once again the changes do not appear set to make either dramatically more financially attractive given the prevailing ESC price. The other change was the reduction in the air conditioning multiplier for commercial lighting which will be reduced from 1.3 to 1.07 and will essentially see fewer ESCs created for installations in premises that have air conditioning use onsite.

Marco Stella is Senior Broker, Environmental Markets at TFS Green Australia. The TFS Green Australia team provides project and transactional environmental market brokerage and data services, across all domestic and international renewable energy, energy efficiency and carbon markets.