Victorian Energy Efficiency Certificates (VEECs)

The period of steady declines in the VEEC price appears to have passed – at least for now – with November appearing to confirm the pricing range established in October. VEEC submissions did vary across the month, starting low before picking up later in the month, though the average remains well above that which is required.

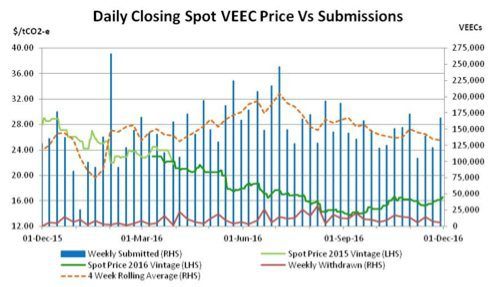

Having found its feet and recovered sharply in October, the spot VEEC market kicked off November by losing ground, opening at $16.15 and progressing to a low of $15.25 across the middle of the month. Yet following several trading days at this level the selling interest once again thinned out, opening the way for the market to once again recover, with healthy trade volumes ultimately helping the spot back up to $16.60 by month’s end.

It was a big month in the forward VEEC market, though perhaps tellingly, far less volume was done with the spot price in the low $15s compared to when things improved later on. Indeed for a period after the spots stabilised a ‘normal’ contango shape returned to the forward curve in which the value of forward settlements escalated above the spot. This persisted until the spot market reached the low $16s, after which the forwards once again returned to a state of backwardation for settlements beyond March 2017. This is the clearest indication that the recovery in prices was led primarily by those trying to buy spot and shorter term forwards, in many cases to meet the large volume of pre-existing forward deals which are to settle before the end of the year.

VEEC submission numbers began the month slowly, with the public holiday associated with the Melbourne Cup reducing the first week to just over 100k, though a stronger remainder of the month resulted in a weekly average of 133k uploaded across November.

At the macro level, the VEEC surplus continues to grow, with the success of commercial lighting the main driver of supply. By the end of the month there were already 1.2m registered VEECs in excess of the 2016 target (of 5.4m). With more than 1.4m pending registration and another 8 weeks before the cut-off date for submission for 2016 eligibility, it appears the VEEC surplus remains highly likely to exceed 3.5m, with a best estimate at present somewhere between 3.6-3.8m.

Given such a situation, there are those who question why prices have not continued to fall. The most convincing response at present appears to be that with the VEEC price in the low $15s or below, the commercial lighting giveaways that are the overwhelming contributor to supply become decidedly less appealing for installers and thus a trading range (of sorts) has emerged.

Looking forward, it appears this range will be tested by VEEC submission rates in the New Year and the trade off between the introduction of newer, more efficient lighting products and new methodologies (such as non building based lighting) on the one hand and the saturation of the sites with the highest extended operating hour rating on the other. The rolling off a higher priced forward deals struck early this year will also impact on profit margins for creators which will be another interesting factor to observe.

New South Wales Energy Savings Certificates (ESCs)

Strong ESC registration numbers reinforcing the presence of a large surplus undermined confidence in the ESC market in November, leading to a sharp and persistent decline across the month which at one stage saw the market reach a 19 month low.

The presence of a large ESC surplus (3.3m or circa 85% of the 2016 target) rolled over from 2015 has been an argument used across much of 2016 by those of the view that prices should be lower. When the first 6 months of 2016 are analysed, average weekly registration figures (76k) were marginally above the weekly rate required by the 2016 target (73k).

However, as can be seen in the chart below, between July and September ESC registrations fell sharply, with the average figure down to 28k across the three moth period. This drop – caused by the delay in audit times owing to the additional compliance measures introduced by the scheme’s regulator – hamstrung creators and brought a prompt end to the decline in prices that had characterised the end of the financial year. Yet, while it was in October that ESC registration began to climb again, it proved the sustained high levels of weekly registrations in November ( which averaged 132k) that caused buyers to run for the hills. Such is the nature of ESC registrations which, unlike in the VEEC market, happen in fits and starts as creators emerge from an audit, are then able to register large chunks of certificates over short time frames in line with their audit limits, before then going back into audit for a month or two without creating any.

The spot ESC market opened November lower at $22.85 and moved relentlessly downward across the month with buyers spooked by supply concerns and sellers opting to follow the market down rather than disengage. As is sometimes the case in markets, a trend develops a momentum of its own and can result in overshooting, which appears to have occurred in the ESC market in November. With the spot having reached a low of $18.10 in the second half of the month, buyers re-emerged and the selling interest became harder to come by, allowing the spot market to end the month back at $19.00.

The big questions ahead for the ESC market revolve around the release of the update to the Scheme Rule (due any day now) and the outlook for supply moving forward. With the major increase in the ESC target taking place in 2016 (2.8m in 2015 to circa 3.8m in 2016) and only minor annual increases to follow, participants will be looking for signs of whether ESC registrations will be maintained at the levels seen across 2016, or instead whether 2017 will be the year that the sizable ESC surplus begins to be eroded.

Marco Stella is Senior Broker, Environmental Markets at TFS Green Australia. The TFS Green Australia team provides project and transactional environmental market brokerage and data services, across all domestic and international renewable energy, energy efficiency and carbon markets.