Firm plans have been developed for enough New South Wales transmission for 14GW of new wind and solar, but most of that transmission won’t be complete before 2028.

If all 14GW is built, and adding in rooftop growth and pessimistically assuming no demand growth, then all the coal generation in NSW will be squeezed out/replaced by 2030, or 2032 at the latest.

The transmission will cost around $10 billion once downstream links to load are also built. That will essentially double the value of transmission installed in total in NSW. The process will introduce more competition into transmission ownership and operation within NSW.

Although clearly slow, the process seems thorough and should/could give more confidence to wind and solar developers.

The planning process for approving wind farms has been streamlined but developers still have to go through eight steps, even in a best case scenario, and can expect to spend two years or more on biodiversity and similar studies.

Around 6GW of wind have progressed to the latter parts of the EIS approval process but some of those projects will still face significant community resistance (e.g. the big hat Barnabies and Barnaby wannabes who oppose Winterbourne).

The market will be tight between now and 2028 although increased transmission from Victoria and Queensland will help.

NSW energy minister Penny Sharpe seems to be trying to throw the social license message off course and needs to get on message and lead the social license proposition from the top.

I doubt that Origin has any intention of selling Eraring back to the state and the sooner we move on from that scare campaign the sooner progress will be made.

In the meantime, the behind-the-meter industry is standing by in case either the state or federal government work out that they have an unexploited reliability asset ready to deploy in the form of household batteries.

Context

Recently EnergyCo released its “NSW Network Infrastructure Strategy” [NIS]. This document outlines EnergyCo’s lastest and most comprehensive views on what transmission needs to built within NSW, the timing and the cost.

The latest episode of the Energy Insiders podcast discusses the strategy with James Hay, CEO of EnergyCo and Andrew Kingsmill, executive director (technical).

The NSW electricity decarbonisation program is not actually called that, but it amounts to replacing all the privately owned coal stations with privately owned variable renewable energy and supporting firming power.

The carbon reduction was not mentioned once in the NIS report and nor does it appear to be an explicit constraint in the modelling process. No matter, the economics of wind and solar are sufficiently strong despite capital cost increases as to make them the natural choice.

The coal stations will end up being replaced because they won’t be able to compete with lower variable cost wind and solar once it’s built, and because they are, in any event, old, at risk of breaking down, or don’t have reliable access to coal; or have full ash dams and other issues.

The prerequisites for the transition include that enough new wind, solar and firming is built, have satisified AEMO’s generator performance standards [GPS] or derogated NSW equivalents, and have transmission they can connect to.

It turns out that building wind farms has become a highly skilled, value added business.

Wind farm sites with potential for connection are hot property in every state; those that have done most of the four to seven years of wind speed measurement, connection planning, environmental planning and social license approvals required, even more so.

Yet, in the end, the thousands and perhaps tens of thousands of construction jobs, and the regional management of the resulting generation and infrastructure is, in my opinion, the biggest decentralisation opportunity that NSW (and Queensland) have had in many years.

Little towns like Uralla are booming as a result of one solar farm (450 construction jobs). When the next drought hits the diversified income will be invaluable.

Yet none of it can happen without transmission.

A summary of the NIS is that $10 billion will be spent by FY29 to enable 14GW of new generation to be connected:

The plan also allows for significant further expansion beyond 2029 as that becomes necessary.

The $10 billion spend is almost identical to the average real size of the existing Transgrid regulated asset base [RAB].

And so it’s reasonable to assume that the cost to consumers, spread over the entire NSW consumption, not just the REZ production, will be about the same as what Transgrid currently charges. And that is $14/MWh in real terms.

In short, this program will double NSW transmission costs, but on the other hand consumers will avoid paying coal costs and existing coal plant maintenance costs.

The overall impact on electricity prices of the NIS has yet to be officially commented on. The basic point is that the coal stations had to be replaced.

Benefits and problems

The claimed main benefit of the NIS is the certainty it provides to developers that they will be able to connect.

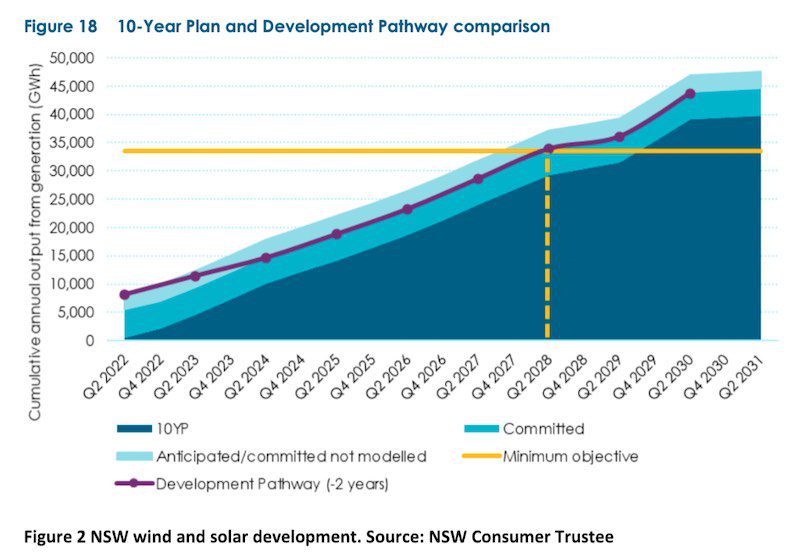

The biggest problem, in my mind, is how long it’s going to take. The NSW road map was announced in 2020, transmission to make it a reality will be on board in 2028.

The development plan that EnergyCo’s sister organisation, the NSW Consumer Trustee, has published (but which hasn’t been updated for a while) calls for 35TWh of developed wind and solar by Q2 2028.

Looking at the above graph one imagines renewable energy coming on line every year at a steady pace. Indeed LTESA (insurance) contracts will be issued at a rate of about 2GW per year to aspiring developers.

But even assuming they had built the plant, there will be little or nothing to connect to prior to 2027. So there will be a fairly big connection process going on from 2027 to 2029. In numbers, about 9GW will want to be connected over a couple of years.

Skills are a challenge. Essentially all the transmission is expected to be operational in 2027-2029. In other words, it’s all going to be built at pretty much the same time as the wind and solar is being built. And that’s just in NSW. Queensland will be going through a similar build, maybe a year or two behind.

Clearly there is room in NSW for some expanded training similar to the recently announced Queensland “Supergrid” training centre to be established in Gladstone, to upskill 500 workers per year.

Lots of higher level skills will also be needed. These are not the responsibility of EnergyCo or the NSW Trustee but rather the state government.

Instead of creating panic in NSW voters’ minds by talking about Eraring, Sharpe could do something practical and useful and completely in keeping with NSW ALP values by getting a similar or better training facility up and running.

That said, the workforce can be relied upon to meet the demand. Jobs of today didn’t always exist a decade ago.

Almost enough under the roadmap to fully replace NSW coal

This analysis ignores the firming capability of coal generation. Firming is important, however this analysis is focused on bulk energy.

Of course, these numbers don’t account for changes in either net imports or changes in demand. Right now, importing more energy from Victoria would help Victorian producers and NSW consumers. But once Yallourn closes there will be some tightness in Victoria for a couple of years.

Building social license – beyond the buzz

It’s one thing to talk about social license and another thing to earn it. This is another reason why minister Sharpe’s panic talk about Eraring is absolutely making things more difficult for everyone in the NSW energy system.

Social license – at a minimum, acceptance, and at best, trust – has to be built at every level. Social license has to be achieved for a wind or solar farm, for the REZ it operates in, for the new transmission and, at the most top level, the overall confidence of voters and consumers in the “efficacy” of the electricity system.

Of course this requires credible, consistent and unified messaging, led by the minister and extending down to the most junior apparatchik.

It was interesting, therefore, to hear of how planning and social license are being progressed through the NSW road map.

According to James Hay and in line with my above comments, the primary focus is about building a long-term big picture message. Communities in a REZ will be able to appreciate the totality of what is being proposed.

Beyond that, EnergyCo has funded a dedicated team within the Department of Planning. The idea of this team is to be specialists in wind and solar projects. Basically I can see how this will improve the process due to the familiarity of the specialists. As a result planning fees for applicants have been reduced.

Further, and perhaps more minor, there is more or less a standardised approach to what’s in it for councils and the council can expect a relative standard contribution from a project within a REZ. That, too, should reduce the overall time taken.

This is probably as much as can be done without substantially changing the existing planning process.

An example of the planning process and a good description was provided by Neoen, in respect of the Thunderbolt Energy Hub. In the best case scenario – i.e. no Land and Environment Court cases – there are eight formal steps.

In the case of Thunderbolt, Neoen submitted the scoping report in November 2020 and received SEAR’s requirements in December 2020. Following this, specialist studies for EIS were undertaken which include two years of ecology studies.

Why mention all this? It’s mainly to note it takes time to develop wind farms.

The list of wind farms in NSW that have reached at least stage six of the above process but haven’t yet started construction is:

Of those, the Liverpool Range site has been approved since 2018 for 1000MW. But Tilt, which acquired it in 2019, is now proposing 1300MW. Certainly none of these projects are speed demons in terms of getting started.

Even once notice to proceed is issued its likely that three years of construction will be required. Developers could, and arguably should, speed this up given their confidence by, for instance, doing early road works. Typically 20-50 km of roads have to be built.

My point is that it will take a while for any of this wind to actually help NSW consumers; at least three years for these projects and ignoring a couple under construction, principally Rye Park. On the above list only Uungula has any chance of getting Notice to Proceed this calendar year.

Connection, batch processes

I have, however, heard a number of concerns expressed in advance of the “batch” process experience, more properly called the REZ connection process. Andrew Kingsmill made two, to me, important points about this in the Energy Insiders podcast.

Firstly, that generators within a REZ will have clear REZ determined generator performance standards to meet and secondly, and perhaps more importantly, that NSW can “derogate” – that is, to an extent, step outside the NEM rules and make its own connection rules.

EnergyCo is in the process of formulating such a rule. I guess ultimately AEMO will still have a say and EnergyCo will still need to demonstrate that its rules result in an improvement, compared to the current process, and also have to mesh with other streamlining proposals. Nevertheless, this explanation was a cause for optimism.

Risk and mitigation – behind-the-meter storage

It remains a mystery as to why federal and state policy turns such a blind eye to behind-the-meter storage.

There are “nation building” pumped hydro projects such as Snowy 2.0, Borumba or any of the pumped hydro projects that have been mooted in South Australia for a decade and in NSW for five years.

These can all get support without trying too hard. If the state government money is not enough, don’t worry the federal government will back it up with the Capacity Investment Scheme.

To a far, far lesser extent the same thing goes for utility batteries. These have access to system services revenue and again can be eligible for either state or federal capacity support.

But even with that support it takes a couple of years for each of these batteries to do their connection agreement, organise the finances, run with the lead times and get built.

I, of course, think utility batteries are terrific and the longer-term solution to the majority of the NEM’s storage needs (other than seasonal and VRE droughts). Yet household batteries can be done faster and consumers will pay most of the cost.

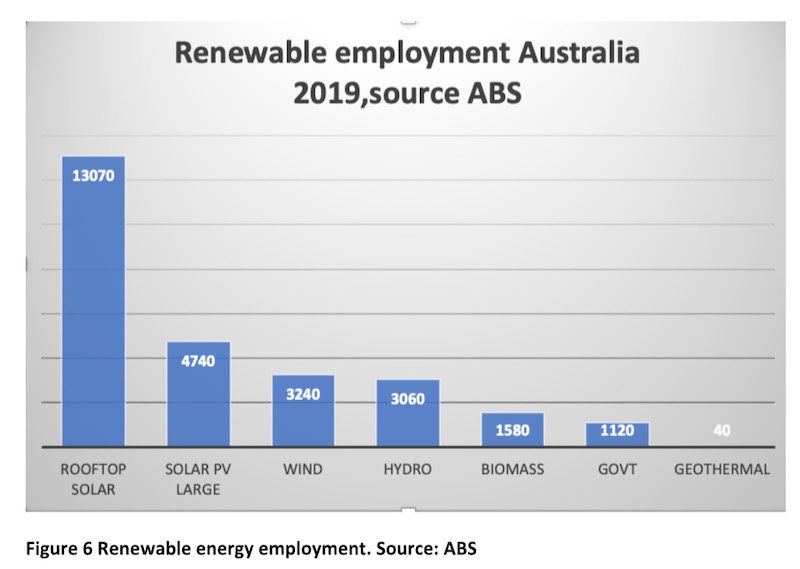

I don’t believe the renewable energy employment statistics have been updated since 2019, but at that time the rooftop industry was easily the largest employer and I suspect it remains so.

The rooftop industry is, by and large, fully trained, doesn’t suffer a skills shortage and can easily, easily sell more household batteries.

As I have previously written, the batteries and the associated inverter software are far more capable than they were five years ago.

There are plenty of competing brands and the sector continues to innovate. Tesla, the market leader by far is about to launch the Powerwall 3 which has 11.5 kw of maximum power, far more than most houses need at one time.

In NSW, 100,000 of those Powerwall 3s running at once could deliver more than 1GW of firming power into NSW and it could be done, arguably, within 12 months, or certainly two years – i.e. by the time Eraring closes.

If you are one of the increasing number of people, not currently including me, who think that vehicle-to-grid is a better idea than household or community batteries, then incentivise that sector.

But I don’t think the standards and technical side of vehicle-to-grid are settled yet and in any event the EV industry has already shown there won’t be sufficient supply to make a difference in NSW in the next couple of years.

I won’t say any more on the topic as it does seem to be controversial (subsidies for the wealthy, community batteries are cheaper, household batteries are too expensive, vehicle to the grid will render household storage obsolescent) – but I just continue to find the idea attractive and capable of providing a quick improvement to the NSW reliability outlook over the next three years.

My electricity bill with seven people in the house, a heat pump on the pool, ducted air con and an EV is just $20 a month. And yes, I am lucky, but the NSW government could help to make more people lucky if it wanted to and take some of the strain off peak prices thereby improving the lot of all consumers.