Wednesday’s newsletter provided a fascinating glimpse of the contrasting themes that are sweeping through the electricity industry: One one hand there was Citigroup and Jeremy Grantham warning of the risks to fossil fuel generators and incumbent businesses, and then there was AGL Energy, the Australian utility with the greatest track record in renewables, deciding to treble its exposure to coal-fired generation with the purchase of the Bayswater and Liddell generators in NSW.

What is going on? Is the proposed purchase of the MacGen business, as RenewEconomy suggested on Thursday, an opportunity simply too good to refuse for AGL? And what does it mean for renewables and competition in the country? Does mean an early sacrifice of both, or is AGL positioning itself to be the last utility standing by taking control of the cheapest suppliers?

Analysts are also wrestling with this issue.

David Leitch, from UBS, noted that AGL Energy had now committed $4.5 billion in the last three years in thermal generation (coal and gas), an industry Leitch says “is in trend decline due to the requirement to decarbonise the global economy.”

AGL had once claimed that the best way to prepare for a clean energy economy was to have the lowest possible emissions profile. UBS notes that AGL Energy has now invested so much in coal and gas that “if the Australian economy moves quickly towards a decarbonised economy it could pose significant threats to AGL”

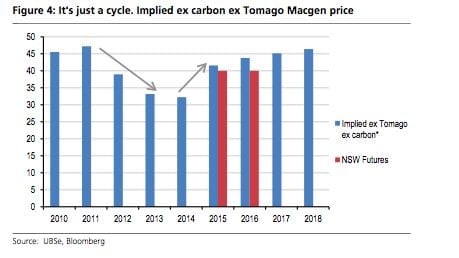

While AGL has highlighted MacGen low coal price of $34/tonne as a major attraction, UBS points out that this in itself has not prevented a significant slide in MacGen’s earnings in recent years. Its average price (net of carbon) has fallen to $35/MWh from $44/MWh in 2010.

It assumes that AGL must be calculating an improvement of $300 million in synergies to meet its assumption that the purchase will be “value accretive”. i.e. it will lift earnings rather than reduce them. To achieve this, it suggests, AGL Energy would need to achieve a $10/MWh increase in average prices.

Here is how UBS imagines the cycle to turn on wholesale prices. (table to right). If it turns out to be the case, it will make a nonsense of Prime Minister Tony Abbott’s claim that removing the carbon price will deliver reductions in the cost of energy. Not that anyone beyond the NSW Ltd press believed that anyway.

Here is how UBS imagines the cycle to turn on wholesale prices. (table to right). If it turns out to be the case, it will make a nonsense of Prime Minister Tony Abbott’s claim that removing the carbon price will deliver reductions in the cost of energy. Not that anyone beyond the NSW Ltd press believed that anyway.

UBS says that given the historical volatility of MacGen, an Ebitda of $350 million is a reasonable forecast, but so is a forecast of $250 million, or even worse, “ if for whatever reason demand is soft and renewables continue.”

The scenarios for that to happen include the around 5% of Victorian demand that is tied up with the likely to be closed Point Henry aluminium smelter. Demand will also be affected by th closure of the car manufacturing and car parts manufacturing industries.

“Near term, the new Federal Government’s policy of delivering lower electricity prices at the expense of environmental policies is an opportunity for coal generators,” UBS writes. “We doubt if it will be a long-lived opportunity and expect “decarbonisation” to become an ever more entrenched concept worldwide.”

In a separate report, Deutsche Bank noted that the purchase marked a “major strategic shift for AGL Energy,“ because it would move from selling more electricity than it generates (short generation) to generating more than it sells (long generation).

“With wholesale electricity prices currently depressed due to subdued demand and recent increases in preferentially-dispatched wind farm capacity, we recognize the argument that now is not the time to go long generation,” the Deutsche analysts note.

But, they also say that Macgen’s low position on the cost curve means that it will be less impacted than other generators, and AGL Energy could use its long position to source cheap supplies and help it win over more retail customers, furthering its strong position in the retail market.