The renewable cavalry is coming but there may be casualties first

This note updates an earlier attempt looking at the net changes in supply and demand across the National Electricity Market (NEM) in view of further analysis we have been doing.

Specifically we update our new supply estimates to allow for recently confirmed projects, and the impact of the increasing oligopoly in thermal supply.

12 months ago our expectation, and we think that of the overwhelming majority of the electricity industry, was that Portland Smelter would most likely close and Hazelwood power station, having survived the carbon tax, would most likely stay open for a few more years.

In fact the reverse happened producing a net swing of 10-11% in supply required from other suppliers relative to the earlier expectations. We can add a couple of TWh to net demand from hotter January February weather.

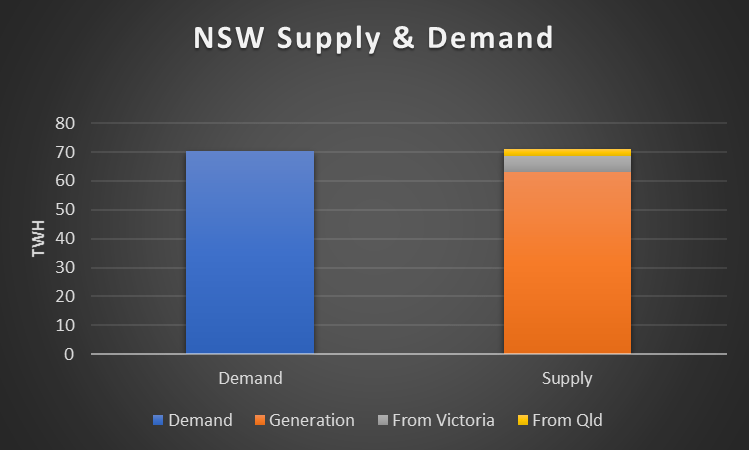

We could make Figure 1 more dramatic by eliminating QLD’s 55 TWh of demand and supply on the basis that QLD is not far off being an electricity island at the moment.

NSW $300 Cap contracts – a good indicator

The March 2018 $300 cap contract is arguably a key indicator of expectations. Buying these caps ensures that the buyer won’t have to pay more than $300 per MW for every MW of cap cover. We look at the March 2018 and March 2019 NSW contracts.

Prices have recently eased of a touch. This may indicate that the underlying market is finding a level. Still we aren’t sure how much trading there actually is. For large electricity consumers (industrials and similar) caps can provide some financial insurance against events such as we saw this Summer.

New supply would have been here a lot earlier …

Nearly every Australian will pay some part of the cost of the Abbott Government’s decision to effectively stop investment in generation. The attempt to abolish the RET and the destruction of confidence that caused has been by far the most destructive thing done in Australian electricity market for many, many years.

The negative impacts of that policy will go far beyond the actual $ impact, severe though that is. It is entirely arguable those policies are the driving force in the current break down of the cooperative Federalism that has underpinned the NEM.

The only significant new supply to come onstream this calendar year is that driven by the ACT Govt’s reverse auction scheme (Hornsdale and Ararat). The same style of scheme that the current Federal Govt has been criticizing.

New supply to total over 4Gw but only 600 MW utility scale in 2017

If we turn to new supply we estimate that over the course of calendar 2017 and 2018 there will be about 4.1GW, or more than 3X what is lost through the closure of Hazelwood.

However in terms of energy we still see a small net deficit.

We think this a reasonable view but in terms of caveats and footnotes.

- We don’t really know what the capacity factor of the utility PV will be as little of it is actually operating right now (just the Moree plant)

- Because grid delivered electricity prices are increasing 20-30% and the public is going to get scared about blackout risk we see that there is a possibility for a reacceleration of distributed PV over the 600 MW a year we have allowed for. We think maybe as much as another 150 MW a year is plausible

- There are a number of projects that have been announced but haven’t yet achieved FID (final investment decision) that could add another 500 MW or more into the total.

- Intermittency impact.

- The value of the dispatchable energy that Hazelwood produces is higher than the value of intermittent renewable energy that will replace it. To put it another way the new supply because of its intermittency will still result in higher average costs to consumers because some “insurance generation is required”.

- Its important to stress that we think this is just a temporary outcome. In the fullness of time as the portfolio benefits of diversifying the wind and PV portfolio occur and as the capacity factors increase then the cost of an individual project’s lack of dispatchability will reduce. Numerous studies have shown that 100% renewable penetration can be accomplished at prices of $100 MWh or maybe lower.

- In States such as NSW and Victoria and QLD there is a much higher ability to deal with increased renewable generation than there is in South Australia. To start with there is the 3.5 GW of Snowy hydro capacity, 0.5 GW of Southern Hydro and whatever part of Tas Hydro’s 1.9 GW that can be exported to Vic. On top of that several of the coal stations have quite flexible ramping capabilities.

- The new wind and PV farms offer lots of regional employment. To your author it just seems crazy not to fully support them.

- Wind and PV projects are fast build (1-2 years) and so far nearly all seem to come in on time and budget. With wind the capacity factor is sometimes questionable but more experience seems to be reducing that risk.

The wind projects

Our updated wind list is shown below. We note that Hornsdale 1 is now operating (and has achieved a pleasing 43% capacity factor for the calendar year to date). About half of Hornsdale 2 appears to be also commissioned.

Stockyard hill = Waiting for Godot

We draw attention to Origin Energy’s Victorian Stockyard Hill project which is over 500 MW. This project has been dragged out for years and years and years. But like “waiting for Godot” nothing has so far happened. If Origin had been a bit faster with this project it might have made a significant difference all by itself to the outlook for Victorian electricity supply.

Only Ararat and Mt Emerald representing 415 MW between them are scheduled to be completed in calendar 2017. The rest mostly over calendar 2018.

PV projects

The list of new utility PV farms we have:

We expect most of the 250 MW of “likely” projects to proceed. However despite the fast build they are increasingly unlikely to get done before 2019. None of these PV projects appear likely to be commissioned in 2017. A big thumbs up to the Ararat wind farm which has all turbines up and looks like it will get its 240 MW done within about 12 months from start of construction.

Looking by year

We show estimates of the year of commissioning. However the point is that much of the capacity to come on line in FY18 will be in H2 of that financial year and will struggle to contribute much in the critical March quarter.

We note that the Ararat wind farm will be constructed in about 12 months an excellent result, and that all turbines at that project have been installed. The PV estimates are rubbery as few public details are available.

Impact on REC target – maybe another 3 GW needed.

So far as we know only the 310 MW of Hornsdale and 80 MW of Ararat will have voluntary surrender of certificates and thus not count toward the LRET target. We also assume that all the rooftop PV will be SREC although there is a clear current financial incentive to use it for LRECs rather than SRECs.

The clean energy regulator estimated that as the end of 2015 about 6GW of new supply was needed for the 2020 target. The more solar in the total the more MW required. Without doing a more detailed analysis but simply subtracting 2.5 GW of non voluntary surrender utility renewables under construction still leaves a further 3 GW to get to the target. We stress that this is a very simple sum. The point is that right now our view is that there is still a significant shortfall.

NSW coal fired generators – not rushing to increase output

Victoria supplied about 5.7 TWh of electricity to NSW in calendar 2016

We doubt that Victoria will supply any electricity to NSW when Portland smelter is at full capacity and Hazelwood has closed.

We see few signs that the NSW coal generators are gearing up to significantly increase output and we note that the Smithfield Cogen facility (160 MW) is currently scheduled to close this year.

In theory Eraring, Mt Piper, Liddell and Vales Point can lift output. In practice we think most of the load will fall on Eraring and maybe Mt Piper and we aren’t convinced Eraring has the coal to substantially lift output. Nor was there any explicit indication from ORG’s recent results conference call that was any intention to substantially lift output. Market intelligence is that Eraring is in the market for 0.5 mt coal.

Mt Piper is dependent on extension to the Springvale coal mine which has received court approval in NSW. NSW coal difficulties have come because

- The China market for Australian thermal coal has improved as a result of China restricting its own coal supply.

- More importantly NSW coal generators had planned to use the proposed Cobbora coal mine for their future supply. When this was cancelled by the NSW Govt. in 2015 the generators’ owners were paid compensation. ORG was paid $300 m. To partly offset the loss of Coborra (ORG entitlement 5 mtpa until 2032) ORG signed a 24 mt coal deal with Centennial over 8 years. That’s around 3mtpa but clearly with Eraring consuming 5 mtpa at just 51% capacity utilization it needs significantly more than just that Centennial contract.

Snowy

Snowy had a dramatic lift in output in 2016 but has slipped back to historic average in 2017 (CYTD avg is 4.2 TWh). Water levels are good with Eucumbene at 47% and Jindabyne 78%. Snowy’s ability to generate can be restricted by its agriculture irrigation obligations. Long story short it should be a big help in the coming Summer.

David Leitch is principal of ITK. He was formerly a Utility Analyst for leading investment banks over the past 30 years. The views expressed are his own. Please note our new section, Energy Markets, which will include analysis from Leitch on the energy markets and broader energy issues. And also note our live generation widget, and the APVI solar contribution.