As renewable energy foes and friends worked themselves into a tizzy over the last couple of weeks over just what happened in South Australia and why, the real action was quietly taking place on traders’ screens.

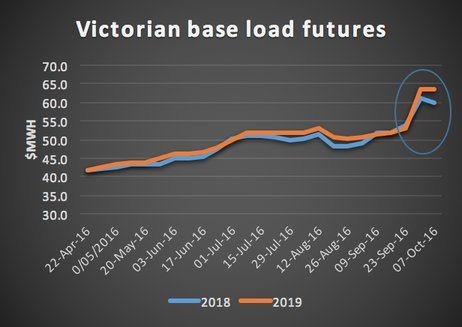

Over the past two weeks, futures prices in Victoria moved up 20% or $10/MWh. Yes that’s 20% in just two weeks. Prices in South Australia barely moved.

That move in the futures tells you that traders are starting to very seriously factor in the closure of Hazelwood. For the moment we think this is only the first wave of price movement. After all, it’s still speculative. Since April Victorian future prices are up 50% or over $20/MWh. That will add 10% to household bills and more to industry in percentage terms.

Household PV prices continue to fall. It’s just about economic to export back to grid.

Sydney, which still has a relatively low rooftop solar penetration (according to the APVI NSW has 15% households with PV compared to 30% in QLD), now has a median install price of just $1.23 w or $5000 for a 4KW system.

If you use your residential mortgage (NAB’s variable rate is 4.1%), and you get 14.5% capacity factor from your PV, 0.3% degradation and 25 year life (good luck with the inverter and the roof tiles) then you need just $65 MWh to break even.

That is very close to your friendly retailer’s feed in tariff (AGL offers $60 MWh, and actually Diamond Energy offers $80 MWh). Amazingly enough, it’s a way lower price than a utility solar plant requires in Australia, partly because of the upfront nature of SRECs, partly because of Australia’s world leading installation efficiencies, and partly because inverter prices are coming down.

Storage costs is coming down and energy density going up. LG presented its exciting (15% more energy density) and powerful new range of batteries. Prices have dropped 15% on last year and are forecast to come down another 15% next year.

Inverters that deal with all the complexities of hybrid systems are still in their infancy compared to the generic market but Redback (just acquired by EnergyAustralia caught the eye for its software). Still the inverter technology that could lead to a step change in inverter costs, probably forcing micro inverters into a very minor role, is the Solaredge “ HD-Wave”.

This technology is claimed to be 99% efficient and use substantially less materials. It uses thinfilm as opposed to electrolytic capacitors. In ITK’s opinion better and lower cost inverters would be another big leg up for the PV market.

Electricity and gas weekly review

- Electricity volumes : South Australia volumes are down 20%. NSW volumes are flat for the year and Victoria down 1%. Further declines in Victoria are expected due to car industry impacts. Queensland volumes are up 4% for the year. Demand is seasonally weak in Spring

- Future prices:. Are discussed above with Victoria being the feature. However in our view the flow on impacts to other States are not yet fully understood. Hold on to your hats, there will be more price action in electricity. Underlying prices will in the (very) long run settle at the LRMC for renewable energy as configured to make it on demand. We don’t know where that price is yet. In the meantime the basic dynamic is that coal and gas fired generation units are very lumpy. Every time a big one is taken out of service it takes time for new renewables to catch up. It would be better to build the renewables first, but that requires courage on the part of renewables suppliers to take the market risk of having their plant come on stream just as the old thermal unit closes.

- Spot electricity prices:. South Australian market was in suspense so prices in that State have no meaning. Otherwise spot prices were largely higher than last year but not out of the ordinary. Victorian prices were lower.

- REC prices were unchanged

- Gas prices : are 50% higher than last year in the STTM at $5 and $6 GJ. This is the new norm. Those calling for more gas fired generation have left it a bit late. If you wanted to go that way gas supply should have been organized 5-8 years ago.

- Utility company share prices: were weak over the past fortnight with several yield focused stocks down more than 20% over the past 30 days

- Company news. Nothing of substance to report other than Redflow shipments starting. Two were on display at All Energy.

![]()

Sources: NEM Review, ASX, Mercari, AEM

Share Prices

Volumes

Lower volumes in South Australia have impacted the numbers in a minor way. Still consumption in NSW and Victoria is flat year on year, and the ending of the car industry will lead to some demand decline. More energy efficiency is great for global warming efforts, but more support for electric vehicles powered by renewable energy would be a win win.

Base Load Futures

Gas Prices

David Leitch is principal of ITK. He was formerly a Utility Analyst for leading investment banks over the past 30 years. The views expressed are his own. Please note our new section, Energy Markets, which will include analysis from Leitch on the energy markets and broader energy issues. And also note our live generation widget, and the APVI solar contribution.