- Volumes in the week ended December 2 were essentially flat across the NEM and we can fairly confidently say, 11/12 of the way through the year, that volumes will be up about 1% for the year in total driven essentially by QLD, with NSW flat for the year and Victoria down.

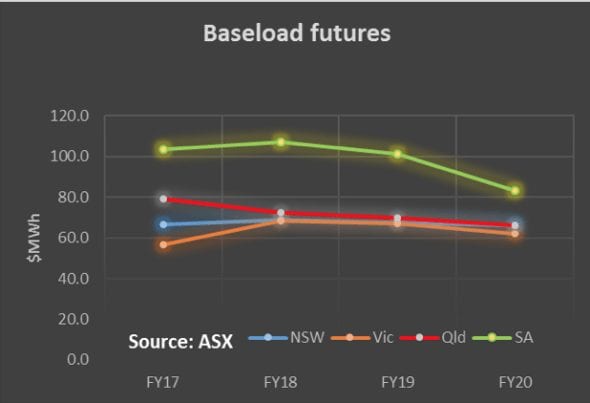

- Future prices:. Continued the seemingly inexorable march upwards. It’s worth looking at figures 6-9 below. They show, particularly in NSW, a continued climb even in the past four weeks. Prices in the States responsible for most consumption are up $20 MWh, over the course of this year all of which will be passed through to consumers. In percentage terms this will matter more to big business than to residential Prices out in the very thinly traded 2019 – 2020 years have dipped a bit. In our view policy uncertainty is once again causing “paralysis by analysis”. We know there is a policy review next year.

- Spot electricity prices Looking at NSW and QLD spot prices were 70% higher than last year during the week. For the calendar year to date, prices in NSW and South Australia are up over 50% and in QLD about 29%. Since demand over the NEM has barely changed most of this price increase represents a reduction in supply. However the supply reduction has only been small in the current year, Northern Power Station, a bit less gas supply. So therefore there is also the possibility of some changes in bidding behavior from an increasingly vertically integrated supply sector. AGL’s ownership of Macgen has no doubt contributed to this, and we would also point our fingers at the Qld Govt which takes full advantage of its ownership of much of the State’s generation system and exploits if fully, normally at the expense of Qld consumers.

- REC. prices unchanged.

- Gas prices : Gas prices on the spot market are essentially double what they were last year at around $7.50 GWh. The idea that more gas fired generation is going to solve energy security needs in the medium term seems fairly untenable to us. We were a fan of Pelican Point being operated in South Australia while better medium term solutions are found, but (i) there isn’t that much domestic gas available to replace coal (ii) Gas generation is not that good at covering for wind variability because gas is inefficient at less than design heat rate and doesn’t ramp quickly enough. It does ok covering the more predictable PV duck curve.

- Utility share prices: .Virtually all utility related share prices with the exception of Ausnet and Redflow outperformed the market during the past week. Barring some disaster the best performing utility shares for the year are likely to be AGL, IFN and ORE (disclosure the Author’s super fund owns ORE). Increasing confidence in the oil price has seen ORG shares up 15% in the past month. Of course CKI’s bid for DUE came too late for this week’s data.

- Industry news..

The main industry news is likely to be the bid by CKI for DUE. Although the immediate focus of the mainstream media is on the FIRB implications since CKI was disallowed as a bidder for Ausgrid on FIRB grounds, our first though is that it will raise interesting questions for the ACCC. CKI is already the majority of owner of two of Victoria’s electricity distribution businesses and 100% of South Australia’s electricity business. CKI also own Envestra which has all the South Australian gas distribution business, and one of Victoria’s gas distribution businesses. Coupled with DUE is will have 60% of Victorian electricity and gas distribution and the lion’s share of remote (ie not grid connected) energy supply.

Share Prices

Volumes

Base Load Futures

Gas Prices

David Leitch is principal of ITK. He was formerly a Utility Analyst for leading investment banks over the past 30 years. The views expressed are his own. Please note our new section, Energy Markets, which will include analysis from Leitch on the energy markets and broader energy issues. And also note our live generation widget, and the APVI solar contribution.