At a time when Berkshire Hathaway’s Nevada Power is setting new record low US$24/MWh solar tariffs in the US, India continues to see the benefits of record low renewable energy tariffs.

In the last two months India has seen 2.5 gigawatts (GW) of wind tenders completed at record low US$36-37/MWh tariffs (zero indexation for 25 years, like Nevada above).

On the back of this, the Indian Energy Minister R.K. Singh has lifted India’s renewable plan from 175 GW to a new mission of 227 GW by 2022.

It is no co-incidence the largest import coal plant in India, Adani’s relatively modern 4.6GW Mundra facility, is idle, unable to compete. Our conclusion is clear – stranded asset risks rise every time new record low renewables tariffs are announced.

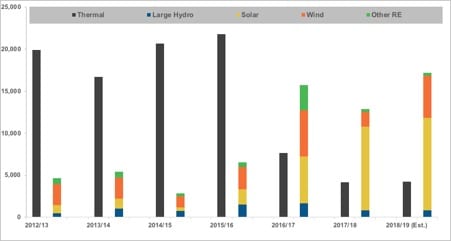

India’s Renewable Vs Thermal Power Capacity Additions (MW)

April 2018 saw a 2.0 GW wind tender by the Indian government’s Solar Energy Corporation of India (SECI) concluded at Rs2.51-2.53 per kilowatt hour (kWh).

Last week a 500 megawatt (MW) wind tender was completed in Gujarat, at price of Rs2.43-2.45/kWh (US$36/MWh), equal to the record low price for wind in India set in 2017.

And the month of May 2018 alone saw a record 10 GW of solar project tenders announced across India, with 1.75 GW of tenders completed at Rs2.71/kWh (US$40/MWh). All prices have zero inflation indexation.

Interesting to note that Adani Green Energy won 300MW of the 2.0 GW wind tender and 200MW of the Maharashtra solar tender, yet another US$500m investment by the Adani group into renewables.

Adani’s total renewable operational energy portfolio has reached 1,958 MW as of March 2018, with another 1.5 GW under development now across India.

One might be mistaken for all the talk of Adani’s Carmichael coal proposal in Queensland, the only tangible evidence of progress by Adani in Australia in the last eight years is the 65MW stage I solar project under construction at Rugby Run near Moranbah (ironically, a property originally acquired for the Carmichael rail line, but now not needed).

While solar tariffs in India have bounced 10-20% up from the Rs2.43/kWh record low set in early 2017, China’s decision to dramatically slow solar installs with immediate effect is likely to see Indian module import prices re-testing 2017 lows below US30c/W, particularly now the High Court has cancelled the proposed 70% module import tariff.

While interest rates in India have edged up since their mid-2017 lows, the scale of renewable deployments plus ongoing technology improvements should more than offset this.

Solar is now consistently cheaper than existing domestic thermal power in India

In April India’s National Electricity Plan 2018 was released, re-iterating the plan to lift renewable energy installs fivefold to 275 GW by 2027, including the previously articulated 175 GW interim target for 2022.

Even allowing for 5-6% annual growth in electricity production over the coming decade, this plan sees thermal power’s share of total capacity in India drop from 67% in 217 to 43% by 2027 – a faster rate of electricity sector transition than achieved by either China or the US over the last decade.

As the fastest growing large economy in the world, India’s global leadership on energy is critical for the world’s goal to limit carbon emissions and climate change.

Where India leads, IEEFA expects the ASEAN nations to follow, given the huge benefits from improved energy security, reduced imported fossil fuel reliance, reduced pollution pressures and consequent health costs not to underestimate the economic motive of electricity sector deflation.

This month Energy Minister R.K. Singh has referenced a possible increase in India’s renewable plan from 175 GW to a new mission of 227 GW by 2022.

Given this implies a fourfold increase in the rate of installation relative to the 15 GW p.a. achieved in the last two years, this looks a really tall ask.

However, the proverb “Aim At The Sky, At least You Will Reach Top Of The Tree!” comes to mind – even if India falls somewhat short of the truly staggering 227 GW mission, it will set the country on a trajectory to deliver on its NEP 2018, an achievement way above the expectations of more fossil fuel oriented modelling groups like the International Energy Agency.

While India’s domestic financial market capacity could not countenance such a massive US$75-80bn annual renewables infrastructure and associated grid expansion cost, the global utility and pension system clearly has the capacity to do so.

The recent multi-hundred million dollar Indian renewable energy investment proposals from SoftBank, Singapore Government Investment Corp, Sembcorp, Caisse de dépôt et placement du Québec the Canada Pension Plan Investment Board, ENEL and ENGIE have provided the perfect endorsement to Prime Minister Narendra Modi’s vision.

Failure to complete the much needed distribution company (Discom) reform remains another threat to investment in the Indian electricity sector.

Unfunded subsidies, unsustainably low agricultural tariffs and excessive financial leverage combine to see Discom losses still ran at US$5.5bn in 2016/17, albeit down by half from the record losses reported back in 2013/4.

However, the wholesale price deflation being delivered by ultra-competitive renewable auctions is continuing to reduce Discom losses, particularly as retail electricity tariffs are creeping up with overall inflation, and transmission and distribution loss rates are edging down. IEEFA expects a further halving in aggregate discom losses in the last financial year.

India is now the fastest growing major economy in the world, and its electricity market is the third largest behind China and America.

As such, the fact that renewable energy is now clearly the lowest cost source of electricity in India and able to be deployed at such scale and speed is illustrative of the magnitude of technology and finance driven change pending for global electricity markets, and in turn for the internationally traded thermal coal market, Australia’s third largest source export earnings.

That India is joining China and Europe as the world leaders on climate change is a telling indication of a changing world order, particularly as America turns isolationist.

Not: Tim Buckley will be speaking at the Large Scale Solar and Storage conference co-hosted by RenewEconomy and Informa in Sydney later this month. To find out more and book tickets, please click here.