Battery storage is the possibly the fastest growing but least understood element of Australia’s green energy transition.

Until 2017, the country didn’t have a big battery on the grid and even the market operator could not imagine a role anytime soon for a battery bigger than 1 megawatt (hour). That all changed with the promise of Elon Musk to build the Tesla big battery in less than 100 days. The grid has and will never be the same since then.

If the market operator didn’t have a good sense of what was possible, perhaps – just perhaps – it could be forgiven when the then Coalition government mocked the Tesla and other big batteries as simple toys in the market, about as useful as the Big Banana, the then prime minister Scott Morrison suggested.

But battery storage is way more useful than a Big Banana. What differentiates it from existing fossil fuel generators, and even pumped hydro, is its speed and versatility.

It can do more than one thing at once, and its Swiss-Army knife capabilities make big batteries and its inverter technologies perhaps the most essential tools of a grid heading towards 100 per cent renewables.

One of the problems of the Australian battery storage market has been the lack of market signals that can actually pay the batteries to deliver the services they offer. They are, however, rapidly evolving, with the recent introduction of the first very fast frequency services market.

The most successful battery storage developer in Australia is French-based Neoen, which built the original Tesla Big Battery (officially known as the Hornsdale Power Reserve) and has since completed another two big batteries, and has another four under construction.

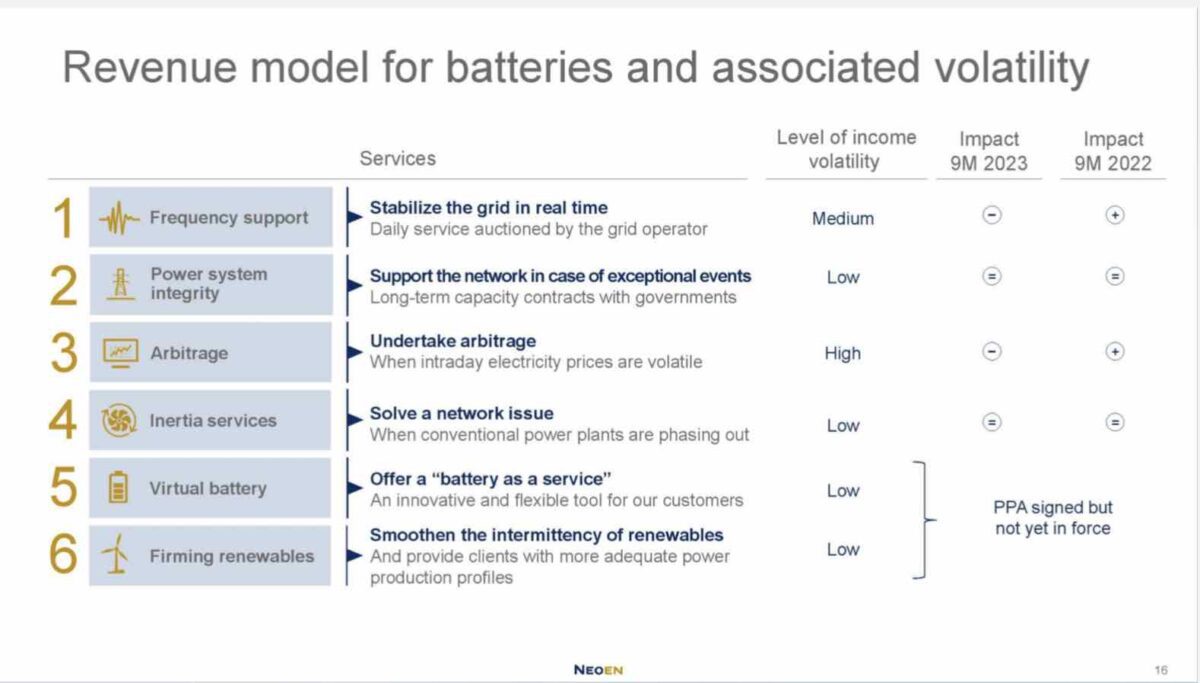

In a presentation to analysts last week for the group’s nine-month revenue report, CEO Xavier Barbaro gave some insight into where battery storage revenues are sourced, and where they are headed.

Barbaro noted that Neoen had unlocked three main sources of income in its initial battery projects – Hornsdale in South Australia, and the Victoria Big Battery and Bulgana batteries in Victoria.

The first of these was the frequency support market – read here how the battery quickly smashed the then gas cartel’s control over that market – where the batteries can intervene to arrest any frequency diversions on the grid.

The second was power system integrity, with long term contracts to provide capacity that will support the grid in times of major disturbances or outages.

These are long term, fixed contracts that allow transmission lines, for instance, to be used at greater capacity. The new Waratah Super Battery in NSW, described as a giant “shock absorber”, is another case in point.

The third revenue source is arbitrage, but as Barbaro noted, this is market based and very much dependent on volatility in the market. When volatility is high, as it was in 2022, the returns are strong. Neoen’s revenues in the latest quarter were nearly half of those previously because of the reduced volatility.

Barbaro says three new revenue sources have been added in recent years that underline the versatility of the technology and the options it can deliver to customers.

One of these is the provision of inertia services, now being delivered by Hornsdale for the National Electricity Market. Most other batteries fitted with so-called grid forming inverters will be able to do the same

The second new stream is offering “battery as a service”, or what Neoen calls a “virtual battery”. Neoen has signed its first such deal, a seven year agreement for AGL to use 70 MW of the capacity of the new – but delayed – 100 MW/ 200 MWh Capital big battery in Canberra.

Other big batteries have similar arrangements, including the new Bouldercome and Riverina batteries (with energy utilities EnergyAustralia and Shell).

The third revenue stream is for “firmed renewables”, illustrated by the landmark “baseload renewable” contract with BHP’s giant Olympic Dam mine, and which will be underpinned from 2025 by the 200 MW/400 MWh Blyth battery under construction in South Australia.

Barbaro says the company has its eyes on more “capacity contracts”, such as the highly lucrative one that it sealed in June for the new Collie Battery, which is also under construction in Western Australia, and is its first four-hour storage facility.

That battery has a specific contract to time shift the output of solar from the middle of the day to the evening peak, squashing the solar duck and simultaneously addressing the grid’s two most pressing issues – low demand in the middle of the day, and high demand in the evening.

The contract is highly lucrative. The details of the two-year deal have not been revealed, but it prompted Neoen to upgrade its forecast 2025 earnings by $A150 million. Other batteries being built by state owned utility Synergy and Alinta Energy have similar contracts.

Barbaro says the key to the growth of the battery storage market will be the mix of revenue streams that offer predictability and market opportunities.

See also RenewEconomy’s Big Battery Storage Map of Australia