What’s interesting this week

This week we focus on two things, one of minor interest in the bigger scheme (but for analysts like myself, it’s fun), and the other a look at the growth area of measuring and estimating the financial impacts of climate change.

- Sunset Power

Adam Walters published a good note about Sunset Power and Vales Point this week in Reneweconomy. Because the accounts essentially provide a view of a single privately owned power station, they are a good indicator of industry profitability dynamics.

So we thought it worth fleshing out the P&L (profit and loss). The year-on-year comparisons are difficult because Sunset acquired Vales Point in mid December, 2015.

To get around this we annualized the reported FY15 numbers. We also show what the pool revenue was, the metered electricity volumes and the coal consumed. All of this latter data comes from NEMReview.

This in turn coupled with the reported financials lets us compare the average pool price received with the price earned in the accounts. Hedging contracts account for the difference.

Finally, we provide a notional estimate of say FY20 profit assuming that by then all the current hedge contracts are replaced by “baseload” futures contracts and that any unhedged volume is sold at a pool price = futures price. We also adjust up the coal price to around today’s export parity price.

We’ve highlighted a couple of numbers that are key. The increase in ebitda over the proforma numbers is not that startling but that’s because the hedge contracts are holding back profits. Looking forward, though, the story is good for Sunset.

Finally we were interested to see that the accounts didn’t show a “remediation” or closure liability. Enthusiastic readers may recall that AGL disclosed this year in its sustainability report a rather astonishing $900 million remediation estimate for Bayswater and Liddell, almost double its estimate for Loy Yang A ,despite the fact that neither Bayswater or Liddell have a captive coal mine.

Our understanding is that the estimate for Vales Point would be an order of magnitude lower, but it’s a moot point because under the sales process Sunset has an obligation to decommission Vales Point at the end of its life, but then the “asset” goes back to the NSW Government who have the remediation responsibility.

After remediation the NSW Government will then have a lot of very attractive and well located land to sell. So it’s hard to say whether this is a net cost or benefit to the NSW Government. But it does fully explain why Sunset’s valuation doesn’t need to account for remediation.

- US GAO report on economic impacts of climate change

Quantifying the costs of climate change is a rapidly growing field, but a breakthrough is needed.

The IMF, for instance, is including climate change in its economic outlook now. Increasingly, company boards are being asked to formalise their response, if any, to carbon risk.

We now know that climate change is occurring quite quickly and can quantify the rate, but my view is that we can have very little confidence in estimates of its economic impacts. The Social Cost of Carbon has a margin of error wider than the Pacific Ocean.

Increasingly this is where the work needs to be done. This week, the US Government Accountability Office released a report which reviewed 31 existing studies that look at specific climate studies, sector specific impacts and economy-wide models.

26 experts were interviewed. The GAO study highlighted the difficulties. Problems include (i) climate modelling uncertainty, (ii) limited information, (iii) challenges of modelling over long time frames.

One study estimated US$4-US$6 bn of USA coastal property damage between 2020 and 2039. How much if any confidence can we have in that number?

Clearly if there is enough warming then damages will be catastrophic, but for warming in the range of 2-3 degrees C what will the impact be? Remember the global average land sea surface temperature in the 20th century is 13.86 c.

The 20 year average (which obviously trails the data by a long time) is 0.64 deg above the 20th century average. An excel fitted polynomial trend is already about 0.75…..

Turning to the weekly action (to October 22)

- Volumes: were down the past week to the lowest level in the past three years. Nationally there is no volume growth for the CYTD over last year.

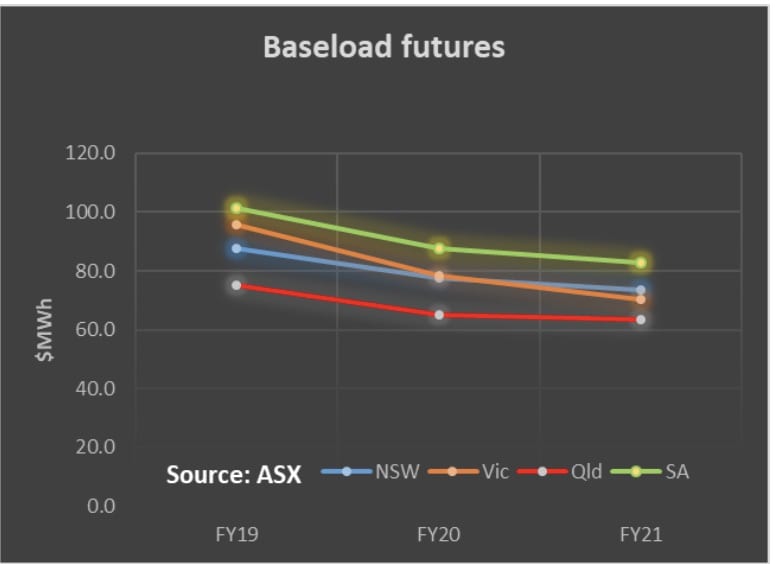

- Future prices Near term prices increased. We show the FY21 estimates in our table now around $73 MWh in NSW and Victoria.

- Spot electricity prices fell this week compared to last week, but in most States, most notably and unsurprisingly Victoria, were substantially higher than last year.

- REC. prices were unchanged.

- Gas prices fell substantially in QLD. We think this likely relates to an LNG train being down for maintenance and the gas supply made available to the QLD spot market. The true test of gas prices will come in Summer.

Utility share prices. AGL share prices rose about 5% during the week. This indicates to us that investors see the Govt’s plan as positive for AGL. Redflow shares continue to be soft. Genex shares have also been strong.

The company has been very prompt in advising the market of its good progress on its PV plan. Should the pumped hydro plan prove a bit slower one wonders if updates will continue to be as frequent.

Share Prices

Volumes

Gas Prices

David Leitch is principal of ITK. He was formerly a Utility Analyst for leading investment banks over the past 30 years. The views expressed are his own. Please note our new section, Energy Markets, which will include analysis from Leitch on the energy markets and broader energy issues. And also note our live generation widget, and the APVI solar contribution.