This note shows that the state renewable energy targets, particularly in New South Wales, will be difficult to achieve because transmission development is too slow and wind development is too difficult.

It’s within Penny Sharpe and/or Chris Bowen’s remit to do something about this.

There are three suggestions.

First: Speed up the transmission development. It’s still too slow in NSW and is already two years behind the initial Roadmap timetable. That’s a job for the NSW minister.

Second: Speed up wind and solar permitting. One way to do this, as the EU has just adopted, is to have a REZ-wide planning approval system. You should not need a year of bird studies for every single wind farm or having to deal with Barnaby Joyce-style objections every time.

Third: Provide a 33% subsidy for household batteries installed prior to 2030 with a limit of 1.8 million installations. Achieving that would add about 9GW of firming capacity with zero transmission required and greatly reduce the need for utility-scale storage. It’s what the Australian Energy Market Operator’s Integrated System Plan (ISP) models.

At the same time, my opinion is that the new NSW energy minister is sending the wrong message. Her message is keep coal going. There may be many other messages, but that is the main one and it just sends the wrong signal.

The state target information source

In looking at the state targets I have primarily drawn on: Jacobs: Victorian energy market modelling, NSW: 2022 Firming Infrastructure Objectives report Dec 2022 and Queensland: Supergrid blueprint.

One of the many issues is in working out what we have at the moment compared to the target. It’s kind of easy using AEMO data to see what is operating today, but then we have to identify what is committed and/or under construction but not operating and, finally, what remains to be committed if the targets are met.

Equally, the processes of meeting targets varies from state to state.

For NSW, the amount of new variable renewable energy (VRE) to be procured is determined by the consumer trustee and tenders will be awarded to procure what’s required.

In Queensland, state government-owned entities will accept capital from the state government to procure and perhaps operate sufficient generation to meet the target.

In Victoria, there are various policy instruments including the offshore wind support scheme. Where, as in NSW, there is a defined amount of power for which LTESA’s will be offered quarterly, the calculations are easier.

Everywhere else we are trying to hold down a number of wriggling, moving targets, that are often camouflaged – and then add them up.

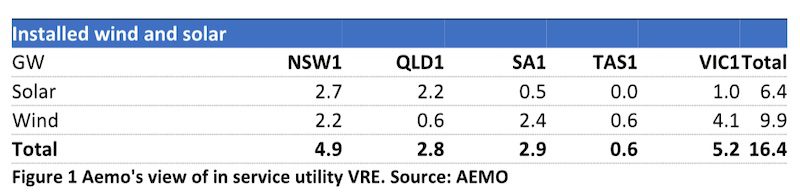

So according to AEMO this is what we have today:

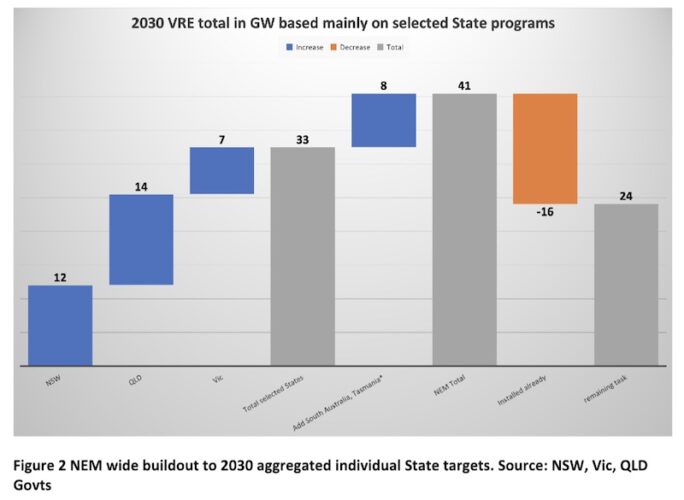

And according to me, if the state government targets are met, and this is already looking less likely, we still need to build about 24GW over the next eight years:

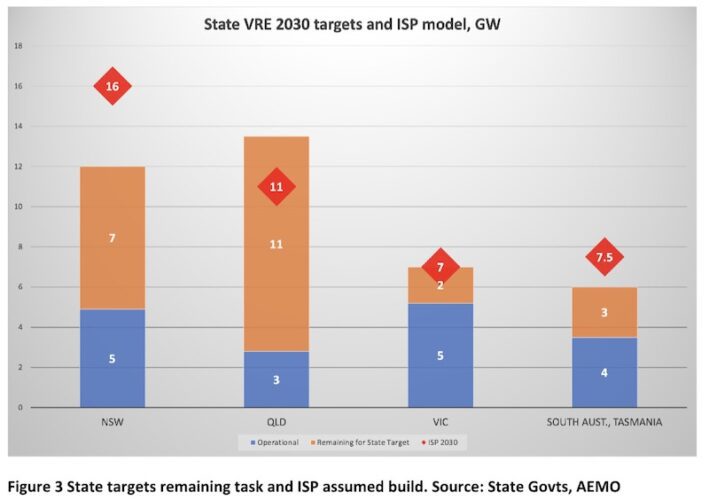

On a state by state basis:

And of the remaining task some projects are already underway.

Wind generation development: the problems

Despite the rise in costs and despite competition from China, USA and Europe there is a strong price signal to build new wind in the NEM, particularly in NSW, see discussion below, and in Queensland.

It’s true that in Queensland there are significant wind projects that have been announced and or under construction. Stanwell has announced PPA volumes of over 2.2 GW in the past 12 months for instance, although CS Energy has done almost nothing of consequence save maybe 100MW/2 hour battery and a solar farm.

However, in NSW progress is excruciatingly, agonisingly slow – even though the need is great.

Wind still faces three major problems, and they are:

- Lack of access to transmission;

- Length of time required to permit, including social license;

- Managing the required AEMO studies including fitting into the untried REZ batching process.

It takes nearly as long, maybe even as long, to get a wind farm approved as it does to get a transmission link approved. This is well recognised as a problem in Europe where the EEC has put in place special planning rules for wind and solar:

“Permitting procedures will be easier and faster under the new law. Renewable energy will be recognised as an overriding public interest, while preserving a high level of environmental protection. In areas with high renewables potential and low environmental risks, member states will put in place dedicated acceleration areas for renewables, with particularly short and simple permitting processes. The provisional agreement also enhances cross-border cooperation on renewables.” (Source here.)

I note: So far the only use of a REZ is to put transmission in place and maybe batch connection negotiation with AEMO. But surely if a REZ is going to be developed it could have one planning permit that covers the wind and solar to be put in place in that zone.

This is something that minister Sharpe could turn her mind to. It would be an advantage to residents in the REZ to see the entire planning picture. They could see the problems but also the advantages in terms of employment and growth in the REZ, gross product per resident.

Many businesses would prosper, 100s of kilometres of new road will get built, internet links will improve. This leads to better health facilities, etc. Renewable energy is the single best decentralisation opportunity NSW has had in many, many years. Don’t waste it and don’t drop the f**** ball.

NSW is a well off the required pace

What jumps out is that the NSW state government target of 12GW, which seemed wonderful when first announced by Matt Kean, is not enough based on the ISP step change. The NSW government target is for 12GW constructed by 2029. The ISP models 16GW by 2030 and 22GW by 2035.

Obviously, and I do think it is obvious, and notwithstanding the huge contribution that behind the meter will make, lots of transmission within NSW and better links with other states are required.

The transmission issue is not really about RIT-T. I completely agree with critics of RIT-T modelling. Ted Woolley is only one respected figure to make what I see as completely valid points about absurd assumptions in the modelling.

However, the fact that the RIT-T process requires dumb, dumb modelling to get over the line doesn’t mean the transmission isn’t a good idea. Or at least not to me.

In my view, the fact that more transmission is needed comes from taking a look at the bigger picture.

Examples include the inability of surplus Victorian power to get into NSW, causing significant price differentials, or equally the likelihood that when Victorian brown coal shuts down more power will need to get into Victoria. Last time Victoria nearly had a blackout, there was 1GW on the NSW side that couldn’t get there.

There is far more to be said about the ongoing Interstates and my views remain unchanged from those presented a year ago – RIT modelling is a furphy – but my current concern is with the IntraNSW side of things.

At the moment, Sharpe, the NSW energy minister, who to be fair hasn’t yet had her feet under the desk for even a couple of months, let alone the two years training I would require of anyone on my team, seems to have only one message: “I will keep the lights on likely by stopping Eraring from closing.”

In my opinion this is entirely the wrong message to be sending stakeholders other than those who don’t know any better.

My translated subtext of Sharpe’s message is: “I don’t know what to do, I don’t have any answers, my team is worried and anti privatisation, so I’ll just stay on that level and kick the can down the road.”

Yet in my opinion the problem is not that Eraring is closing, but rather that NSW is not delivering.

Let’s start with NSW problems

There are a few issues for NSW:

1. The intrastate transmission build out is going too slowly.

2. There is not enough wind or other competition at peak time in the evenings and this has been worsened by Queensland shortages at evening peak, such that NSW generators are incentivised to shift power north.

3. NSW prices are being pushed up by the lack of access to midday surplus in Victoria.

4. NSW doesn’t have much actual policy beyond the road map.

5. Developers of NSW wind projects still don’t have a clear line of sight to the success of their projects.

NSW transmission build is slow

The thing that really struck me in reviewing the NSW road map is how slow the required transmission build-out is progressing.

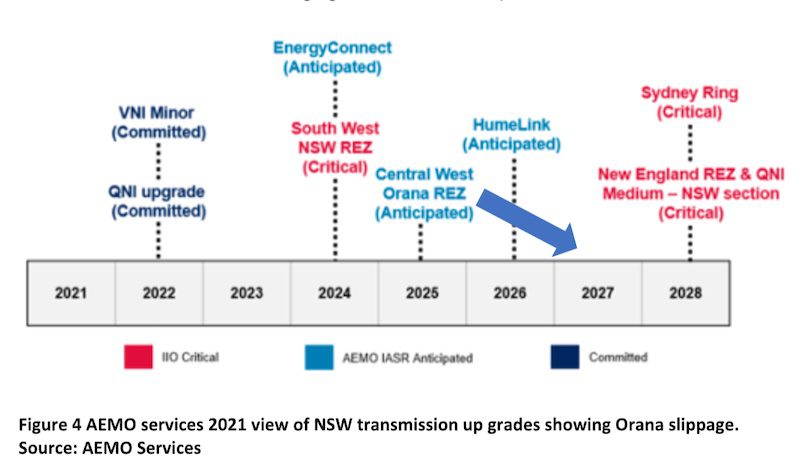

For instance, consider the following figure Aemo Services provided in 2021:

The very first part of that transmission augmentation that the NSW government has responsibility for is the Central West Orana link.

In 2021, when AEMO Services likely had no real clue, as it was just established, that link was expected in 2025. Guess when its now expected? Actually, don’t guess – it’s already slipped two years to 2027.

So even though about 1GW of LTESA tenders are being awarded right now and there will be another 1GW awarded every six months for the next few years, none of it will be able to connect to any of the REZ infrastructure before 2027. And that’s despite the NSW roadmap announcement having been made in November 2020.

In short, for an announcement made in 2020, the first delivered bit of transmission will be in 2027. And that’s if it’s on time.

I haven’t seen an update on New England REZ/NSW section of QNI medium or the Sydney Ring infrastructure, but I’m worried. I understand that an updated Infrastructure objectives report is due to be published imminently and that this will alleviate my worries. Yet I’m still worried.

I think my point is that Sharpe should be worried as well. There are several policy actions that the NSW government could take to improve NSW electricity supply, but getting the required transmission built faster has to rate right up there. How that’s done I don’t know, but that’s what governments do.

One suggestion is to open up all the required transmission to any transmission company, including large international ones, as Stephanie Bashir presented at the Smart Energy Conference.

This will not reduce the need for various studies but a larger company may be prepared to take more risk around a favourable study outcome and start building early.

Going faster will likely cost more and require more risk to be taken. Surely, after having discussed transmission and how hard it is to build almost continuously since 2017, stakeholders have got some clues about how to speed the process up. Surely?

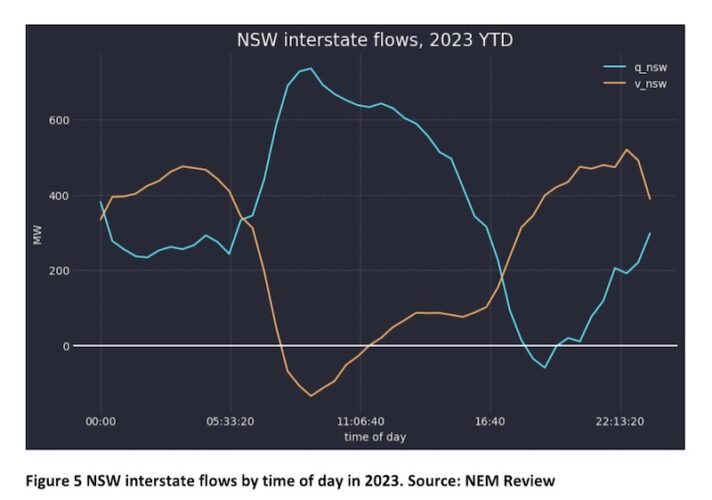

Queensland needs NSW power at evening peak, and NSW exports to Victoria in middle of day

Most of the time Queensland is a net exporter to NSW, but because of all the Queensland coal outages when the sun goes down and Queensland demand goes up at dinner time it’s basically short on power.

So NSW exports to Queensland at dinner time for an hour or two. This pushes up NSW prices. Eventually, this will be remedied by Queensland.

Maybe Callide C will be fixed up before the large amount of Queensland wind under construction starts operating or maybe not but, either way, Queensland’s need to import from NSW will go away, reducing NSW peak prices.

It’s equally perverse that NSW is exporting to Victoria in the middle of the day when prices in Victoria are low. That reflects constraints on the VIC-NSW interconnect.

Household battery rollout is capable of immediate acceleration

Above, I have pointed to the problems in getting wind connected. It’s probably less permitting time for solar but it still takes time.

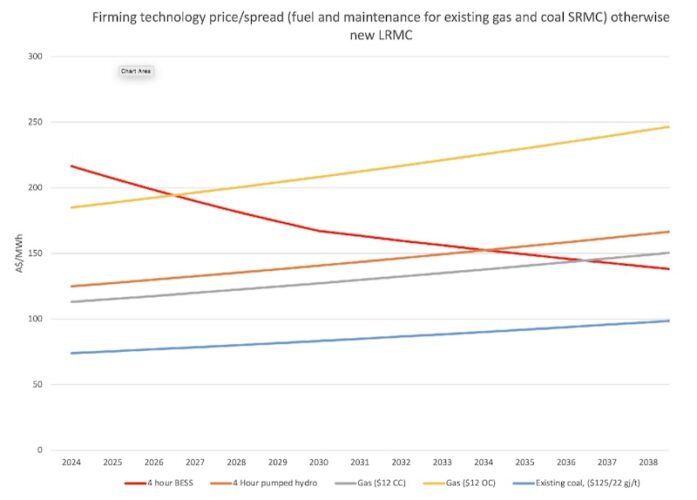

For firming power and bearing the capacity investment scheme in mind, it’s likely that batteries and pumped hydro are the go-to technologies. Yet pumped hydro has zero chance of helping NSW in the next three to four years.

It’s blindingly clear that pumped hydro, whatever its value, takes a long time to develop. It makes wind and transmission look like child’s play.

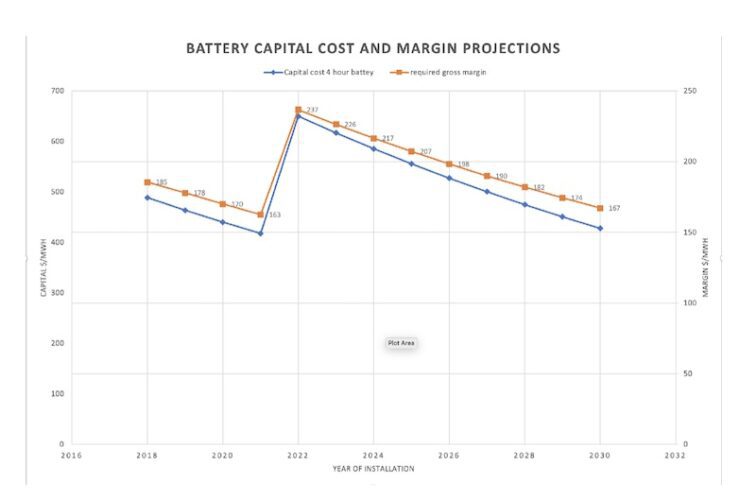

So that leaves batteries. Utility batteries have many advantages. Brad Hopkins made an excellent point on the recent Energy Insiders podcast that utility batteries tend to outperform their investment case.

They need to, because right now based on a $A650/kWh installed cost they need a margin (sell price – buy price) of around $200/MWh every day to justify the cost.

My conclusion from my estimates is that batteries need lots of frequency control revenue to justify investment because they are not competitive with existing gas on daily load shifting.

However, once the battery is built it is immediately competitive because it can generate a positive spread with a price differential between buy and sell as little as $10/MWh. The battery operator may not wish to incur the non cash depreciation cost of the extra cycle for such a low spread but it can be done.

Alternatively batteries can be justified by capacity provision agreements with state governments, particularly in NSW.

Federally, the ill-defined Capacity Investment Scheme may well support some big pumped hydro projects but…

How about some support for household batteries

Years ago the Grattan Institute wrote what I personally regard as one of the dumbest reports I have seen saying that the feed-in tariffs for the household solar sector were a major mistake that “should never be repeated.”

Yeah? Look at the household solar sector today, the world’s best, maybe outside of China, and it all got its start from those feed-in tariffs. Australia would be in a far worse position without the humble hard working rooftop industry. Champions of small business they are.

Many, many politicians attended the Smart Energy Conference. This is a tribute not just to John Grimes and his team and their unstinting hard work to have Smart Energy make a difference, but also to the growing importance of the renewable energy and green lobby. Renewable energy is a vote winner.

Yet I wonder if one of those politicians – Adam Bandt, Chris Bowen, Penny Sharpe – took even one minute to actually walk around the exhibition and talk to some of the vendors, look at the products, understand their position. (Editor’s note: Bowen did do a quick walk around, I followed him!).

From what I saw, and to be fair I didn’t see much and probably missed what they really did, it was race in, deliver some rah rah wave-the-flag message, and race out.

Yet for my money the household battery sector rollout can be accelerated very easily. The industry has spent the past five years improving the product, training the installers, building the software, organising the supply chain.

The only – I repeat, the only – obstacle is price. Household batteries are too expensive, they aren’t that much too expensive but they are still either marginal or on the wrong side of being a good deal.

Household batteries need an incentive. Compared to utility batteries household batteries are of typically long duration. My Powerwall is 13kWh and even drawing 2-3kW at evening peak in Winter that’s at least four hours. Many use cases would be less profligate with their consumption.

If I take the 2022 ISP’s assumptions for household storage it amounts to a massive 9GW by 2030. Think about that relative to Snowy 2. This, of course, completely ignores vehicle-to-the-grid because that is still an emerging technology.

Household batteries are not emerging, they are a mature, ready-to-be-deployed, at-scale technology. Yes, there are equity issues but I ignore them because household storage can reduce average power bills and that will assist everyone, including the poor. Just as rooftop solar has done.

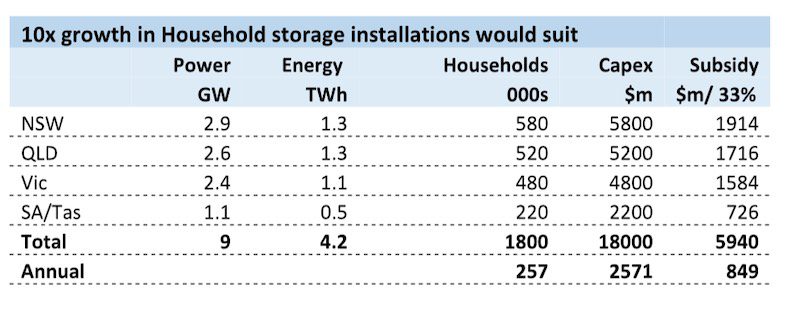

Using the industry-leading Powerwalls as the benchmark, and assuming that faster deployment can drive the average fully installed cost down to $10,000, I calculate that NEM-wide a 33% subsidy would cost less than $1 billion a year:

In NSW, the subsidy would be less than $200 million a year to get 2.9GW of firming power installed by 2030. Try building that much pumped hydro and see how you go.

The household batteries don’t need any transmission support, will – despite what distribution companies say – greatly reduce the need for capex in the distribution network, and will save, on these numbers, 1.8 million households a lot of money on the electricity bills.

Household batteries, of course, work in apartments in a way that rooftop solar doesn’t. I won’t over sell it, but in my view it can be done and it can be done now. It could make a difference before Eraring closes.

REZ are far from the only game in town

VRE doesn’t have to be built out in the way suggested by the state targets, particularly projects like Golden Plains in Victoria, or Goyder in South Australia get developed because the developers convince the financiers it’s a good idea.

But to the extent that the state government programs result in price signals or investment signals beyond what the markets offer on their own then quite clearly properties in Queensland and NSW are valuable. There is a land grab on in Queensland and NSW. And I’d suggest it’s wind that’s the valuable resource.

Equally, putting my non-existent developer hat on, I will maximise my development site net present value to the extent that there is transmission available to build it sooner rather than later.

State government VRE targets

NSW target is 12GW generation from a renewable energy source constructed by the end of 2029 as stated in Infastructure Investment Objective draft report page 17. So that is 12GW constructed over the next seven years. Additionally, there is 2GW of eight-hour or more duration to be constructed by end 2029. Let’s give NSW a year’s grace and say 2030.

Here at ITK we are keen to see some progress under the NSW infrastructure road map. The plan calls for 35TWh of wind and solar to be tendered by 2030. No doubt the build will be a bit behind that.

The first of the wind and solar tenders was held in the December quarter and a short list prepared. But the actual results let alone the construction times, and the actual operation dates, remain as much of a mystery as when the program was first announced. As a reminder the tender quantities and quarter of tender are shown below.

Some people like to think in GWh terms, but the headlines and the capex estimates are mostly based on the MW. For NSW wind, a capacity factor pre-MLF (marginal loss factor) of maybe 35% might be achievable, although I do not think the Orana zone has a particularly noteworthy wind resource and for solar maybe 25%. So 2.5TWh of wind requires at least 820MW of wind or 1150MW of solar.

So basically, the NSW road map calls for tenders roughly equivalent to 1GW of capacity every six months out to 2028. Some tenders a bit larger and some a bit smaller.

It’s essentially the job of the NSW government to make sure the transmission infrastructure is available and that the connection process goes as smoothly as possible.

The connection process is supposed to be speeded up by REZ batching. As explained to me, the batching process means that wind and solar farms connecting through a REZ go through a GPS negotiation with the REZ, then a batch of them are sent through to AEMO to be modelled simultaneously.

The thought seems to be that this will result in a more streamlined process. It seems to me it has a good chance of success because the model of the REZ can be planned out in advance to an extent.

However, the solar will require more firming than wind. Often wind requires more transmission than solar because solar can sometimes be located close to existing transmission but wind has to be located where the resource is.

In the Orana zone, the transmission is available by assumption so there is no advantage to one over the other.