SunWiz and RenewEconomy’s latest update to the Large Scale Lookout service reveals a striking image of solar farm development across the country. Proposed Solar Farms cut a swathe across the country that resembles a ‘fertile crescent’ of solar development.

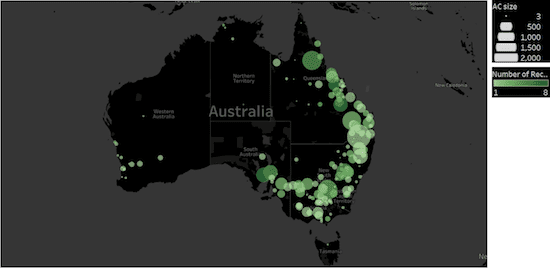

Most of the activity is located in Queensland, where one northern postcode has 6 publicly announced projects totalling 770MW.

In South Australia, there’s a large number of projects concentrated around the Port Augusta region, whereas those intended for NSW are distributed across much of the state.

The map above shows only the projects that are operating. This reveals the huge amount of activity that is planned for the next few years.

There are few solar farms currently operating in north Queensland, only two very small solar farms in South Australia, and there’s plenty of gaps to fill in within NSW before the fertile crescent is harvested.

All in all, SunWiz & RenewEconomy’s Large-Scale Lookout is tracking over 250 Solar Farms that now exceed 30GW of total capacity.

You can find out more by emailing [email protected].