It’s been said before, but it bears repeating, particularly given what former coal chief Ian Dunlop describes as the extraordinary stupidity of Australia’s energy debate:

The global energy industry is experiencing two major tipping points that will mean that coal will never be great again, no matter how much the likes of US President Donald Trump and Australian prime minister Malcolm Turnbull may wish it to be so. The age of wind and solar has arrived.

This was the key message from Michael Liebreich, the founder of Bloomberg New Energy Finance, in the company’s annual get-together in London last week.

The two key tipping points – the cross-over between the costs of wind and solar with new coal and gas, and the crossover between new wind and solar and existing coal and gas plants – have been noted before.

But, in the current debate in Australia, where the government is pushing for existing coal plants to be extended, despite the horrendous costs and poor reliability, and new coal plants to be built, even where they are not needed, they bear repeating.

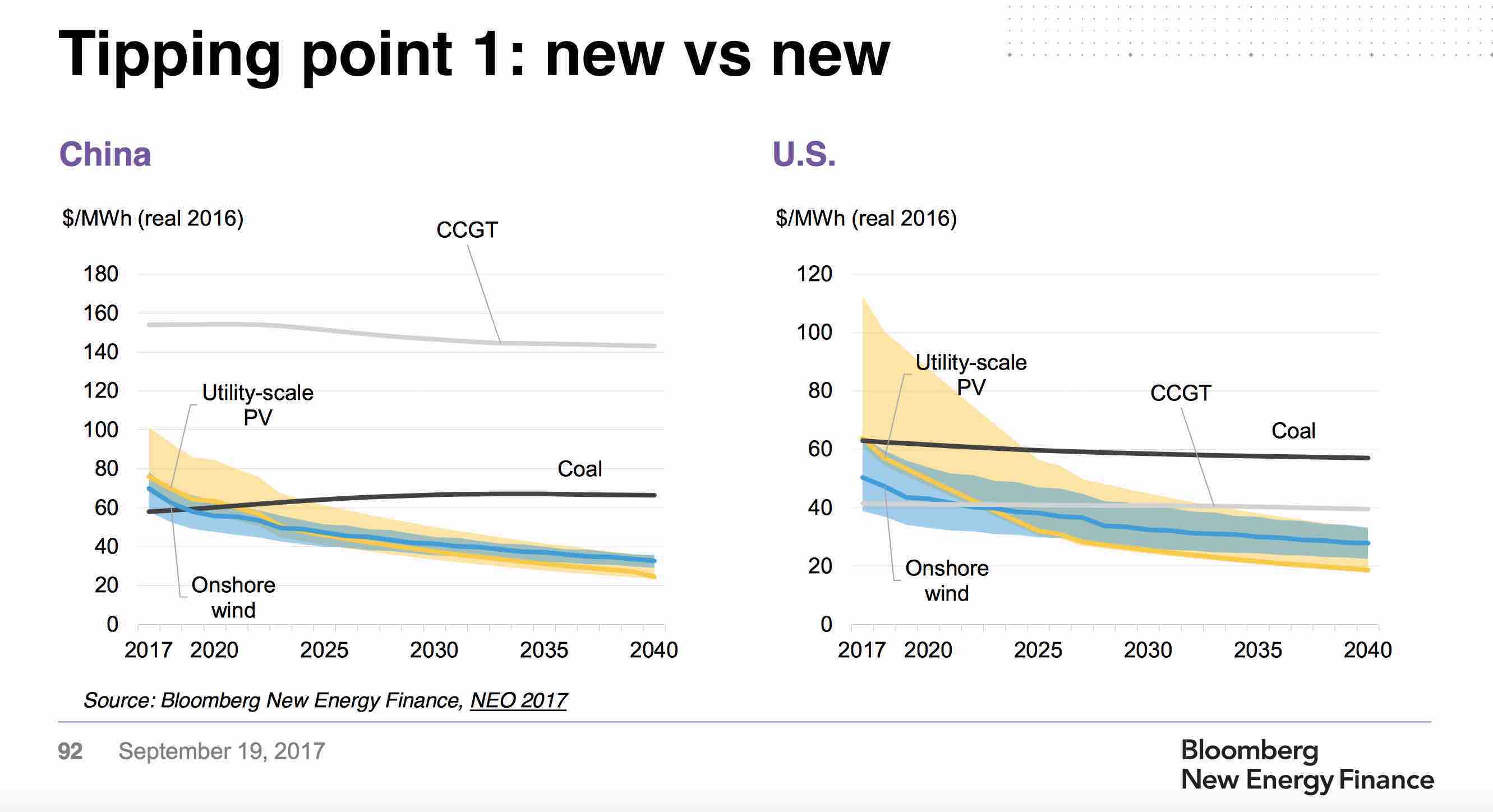

Liebreich says the first tipping point is the one we are living now, and it’s where new wind and solar becomes cheaper than new anything else.

“That means that anything you have to retire is likely to replaced by wind and solar,” he says (if economics rather than ideology were a factor). “That tipping point is either here or close everywhere in the world.”

The second tipping point is really interesting,” he says.

“It’s when wind and solar are cheaper than existing fossil fuel plant. Suddenly your addressable market is not just incremental demand and replacements, it is everything.”

And he adds: “No one is going to make coal great again in the US. It can’t beat cheap gas, it can’t beat cheap renewables, it can’t beat cheap energy efficiency.” Even in China, new wind and solar will beat existing coal.

So, here are the graphs that he used to illustrate this. The first (below) shows utility-scale PV and onshore wind very nearly beating new coal in China, and already doing so in the US, where the main competition comes from relatively cheap local gas.

This tipping point is also occurring in other major energy investing countries like Japan and India. In Japan, utility-scale PV is expected to be cheaper than coal within a few years; in India it will be the same.

The implications for Australia are obvious. New thermal coal projects will be built on the assumption that the coal market will continue to grow exponentially. But this assumes coal keeps its cost advantage – and according to Liebreich, it won’t.

And we are starting to see evidence of that in Australia in the cost of keeping old clunkers like Liddell open for an extra few years.

It is notable that while BNEF is often seen as the most optimistic for renewable energy forecasts, the global energy consultant DNV delivered an even more stunning scenario in its report earlier this month. (See our story: This is just the start of the solar age: Seven graphs show why.)

But what of all that disappearing baseload? Won’t the lights go out? Won’t each new megawatt of wind and solar capacity have to be backed up by an equivalent amount of storage?

Only if we fail to re-imagine the energy system, and we insist on loading up costs by trying to make wind and solar act and appear like “baseload”. There is no need to.

As any market operator will tell you, the age of large centralised baseload capacity is rapidly moving past its use-by date, to be replaced by fast, flexible and “dispatchable” capacity to fill in the gaps of variable renewables and to respond to swings in demand, and the demand peaks.

Chief among these solutions will be demand response and batteries – supplemented by other storage technologies such as pumped hydro and solar thermal.

Small-scale batteries, Liebreich suggests, will jump to more than 200GW, and utility-scale batteries will be nearly as big.

But both will be trumped by demand response – which, contrary to the nonsense you will read in Murdoch media today from future-denier Judith Sloan, does not mean enforced switching off of appliances.

And one final note: Liebreich also took issue with noted climate contrarian Bjorn Lomborg, and his attempts to downplay the prospect that wind and solar will play any meaningful role in the world’s electricity sector.

This battle has been ongoing for years. RenewEconomy got a lot of flack, and demand for retractions, from Lomborg’s representatives when we challenged his assumption in the lead-up to and at the Paris climate talks in 2015.

But his nonsense continues to gain traction, despite new reports shedding some light on how he comes to his “numbers” – he uses the IEA description of final energy demand which, outrageously and misleadingly, includes all the energy wasted by fossil fuel plants in the process of burning fuel and boiling water.

“Using primary energy as a measure is a really stupid thing,” Liebreich says. “Sixty-eight per cent of it is waste, and it comes from oil, gas and nuclear. You only choose primary energy if you want to make wind and solar look smaller than they really are.”