A mix of solar, onshore wind and battery storage remains the lowest-cost pathway for Australia to reach net zero emissions, a new report has confirmed, while also delivering near-term electricity price reductions and shielding the energy market from global economic shocks.

CSIRO and the Australian Energy Market Operator (AEMO) have published the final GenCost 2025–26 report, the agencies’ eighth annual assessment of the costs of new-build electricity generation, storage and hydrogen technologies, designed as an “objective benchmark” to guide policy out to 2030 and 2050.

Like the December draft, the final report concludes the cheapest path to net zero by 2050 for the electricity sector will see solar PV and onshore wind deliver the majority of supply (93%), as the two technologies continue to deliver the lowest levelised cost of electricity from current day out to 2050.

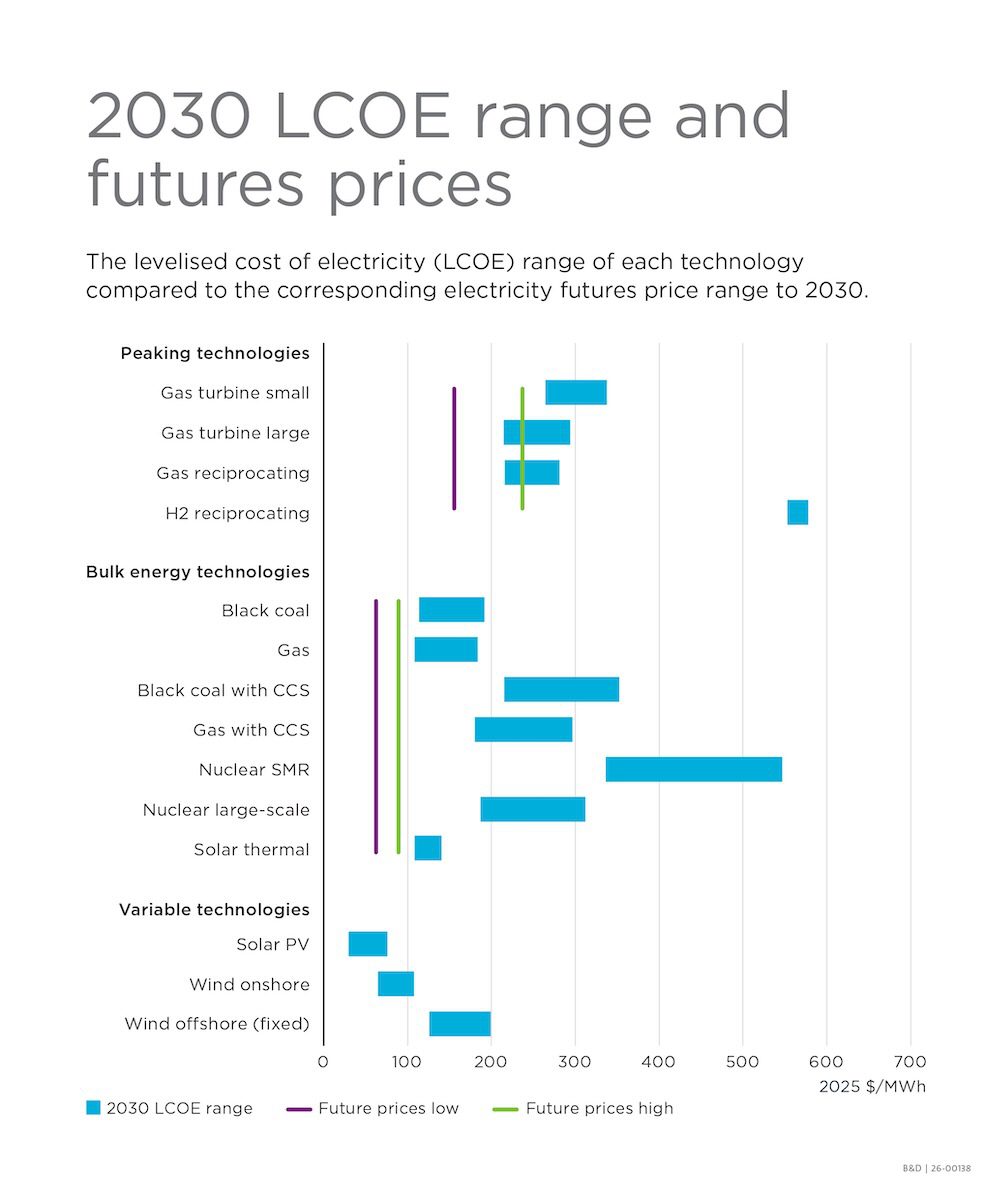

Such is Australia’s progress on solar and wind and ever cheaper battery storage that CSIRO says it expects average electricity generation costs to fall further, down to between $80-$90 per megawatt-hour (MWh) from the 2025 levels of $104/MWh, based on NEM electricity futures prices in the next three years.

“So there’s a good story in the next few years from where we came from,” says CSIRO chief energy economist and GenCost project leader Paul Graham.

“The worst year, recently, was 2022 at $189 a megawatt-hour. We’ve got that down to $104 [per MWh] by 2025 and if you look at spot prices now, it’s even lower than that, the market’s saying about $80 to $90 a MWh over the next three to four years. …So it’s good for consumers.”

Likewise, the influx of batteries – from the grid-scale to the storage systems being installed in hundreds of thousands of Australian homes – has helped to shield Australia from the impacts of the US-Israel invasion of Iran.

“What’s interesting about the Iran war is how little impact it’s had on the electricity sector, and that’s partly because we’re now less reliant on gas because of those batteries,” Graham told Renew Economy in an interview this week.

On the less positive side, he adds, the ongoing global conflict means ongoing pressure on global supply chains and inflation, which means nothing much will be getting any cheaper any time soon – except perhaps solar PV and batteries, driven by China’s seemingly unstoppable momentum.

One of the generation technologies still going up in 2026 is gas, which the GenCost report notes is being squeezed by both the war in the Middle East and by another input that is new to its modelling since the draft report was published – the global boom in data centres.

“New electricity generation capacity required to meet demand from data centres is growing strongly and is impacting gas turbine costs,” the report says.

“Gas turbine costs have already increased for the last four consecutive years. As a result of this ongoing demand from data centres, the projections assume that the cost of gas turbine technologies will continue to increase in the next two years.”

Graham says this adds a new twist to the debate around data centres and how they should be powered in Australia.

“I mean the waiting time [for new gas plant components] is in the order of three to four years. So… it’s arguable whether that would be the fastest way for a data centre to get up in Australia,” Graham says.

“In the US. it’s turned out to be a quicker way to get some of these big data centres up and running, but for me, it’s not clear that it’d be the fastest way to get something going in Australia.

“Because our our development pipeline is full of renewables and batteries – they’re the projects that are kind of ready to be signed off on. I think it’d probably take longer to get a gas turbine project running.”

Beyond 2030, what the SLCOE says

Graham says that following extensive consultation on the draft report in December, the team has decided to rely on market data to model costs for 2030, and only apply its new new system levelised cost of electricity (SLCOE) method to modelling for the 2050 costings.

Out to 2050, Graham says that in the absence of a hard target for what the electricity sector actually has to do, CSIRO goes through a process to figure out what is cost-effective to do relative to the abatement in the rest of the economy.

“We do that by testing a bunch of emission intensity targets in 2050, and we also test that against some of these different technology options for getting there, taking into account that other than solar and wind, most of the other technology options are pretty unproven,” he says.

And while CSIRO’s modelling confirms cheap solar, wind and batteries will “remain the backbone of a least-cost future electricity system,” getting to even a “moderate” net zero scenario will mean higher electricity prices across the board, due to the cost of building replacement infrastructure.

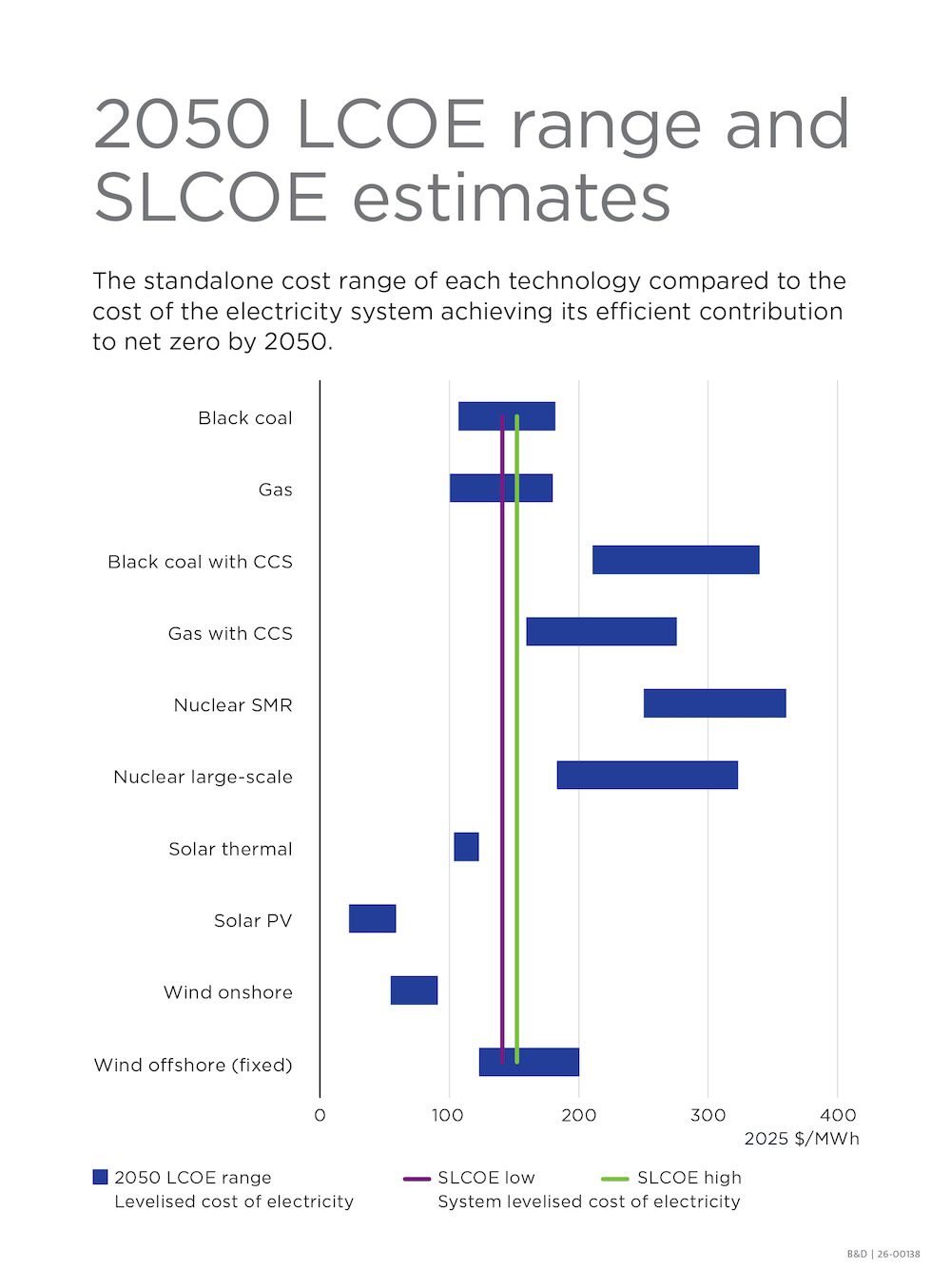

But that would be the case even without net zero policies and with any mix of technologies, including gas and coal – the latter of which CSIRO says will have new-build generation costs in the range of $107/MWh to $182/MWh by 2050.

According to GenCost, the SLCOE analysis indicates that there are “no new-build technology options, fossil or non-fossil with firming costs,” that will cost less than $100/MWh.

If the electricity sector makes an efficient contribution to achieving net zero by 2050, the report puts the cost of generation at $141/MWh to $152/MWh based on solar PV and wind generation inclusive of all firming and transmission costs. Excluding transmission costs, the net zero consistent generation cost is $120/MWh to $130/MWh or an average of $125/MWh.

“When we look at 2050, you can see there isn’t any options really below $100 [per MWh] because, even when you use solar and onshore wind, once you stack up the other costs to make that firm, you’re back up into this zone,” Graham tells Renew Economy.

“So we have to have a bit of an increase post-2030, and I guess that’s consistent with other modelling that’s been done, but the final number we think is, from a generation cost point of view, $125 a megawatt-hour for that to deliver a mostly solar, wind, batteries-based generation system.”

Graham says understanding how global events and technology markets influence electricity generation capital costs is a key part of GenCost’s role.

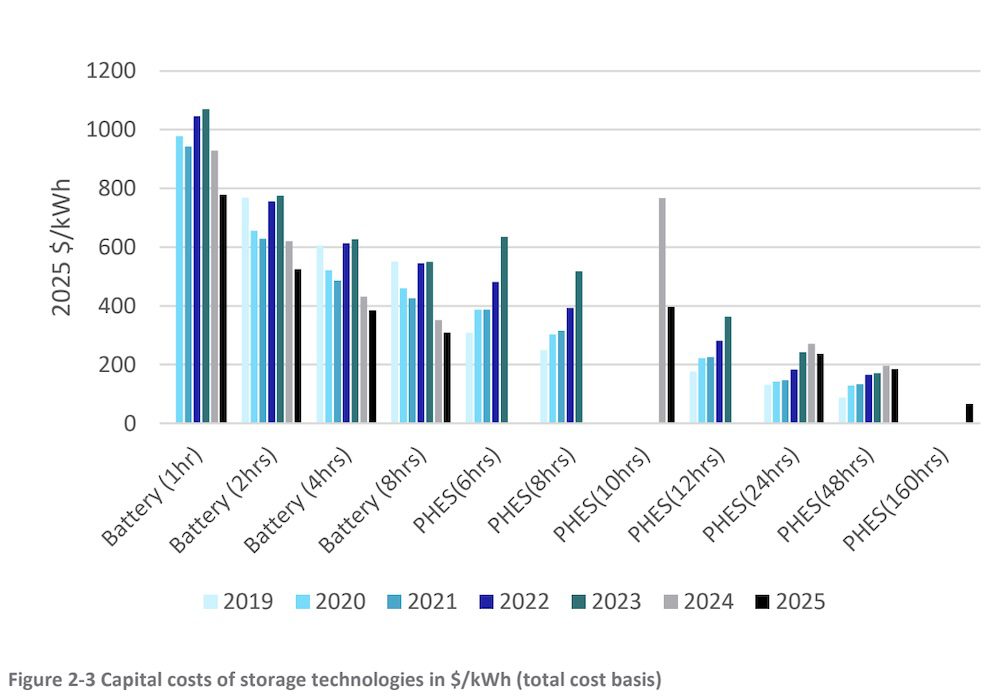

“As battery costs continue to fall and gas technology costs rise, batteries are increasingly becoming the preferred flexible generation technology in the near term,” he said.

“However, GenCost modelling finds gas technologies will still play a limited but important role in helping firm the electricity system, contributing around three to seven per cent of generation by 2050.”

Further reading: Starting from scratch on nuclear in Australia would take longer, cost more than first-time offshore wind