The international news of the week was the reaffirmation of the Paris Accord by 19 out of the G20 countries, including Australia, and the explicit isolation of Trump as called out by Angela Merkel.

The significance of this for Australia is that a mechanism will have to be found to demonstrate how we are going to achieve the Paris Commitment. Obviously, with carbon emissions going up we are not on track at the moment.

This issue takes on special significance as we head into a COAG meeting on Friday.

That meeting will be the first formal opportunity for COAG to discuss the Finkel Report and eyes will clearly be on progress towards the “Energy Security Committee” and what, if anything, the Federal Government takes to COAG in regards to Low Emissions Target.

Locally, of course there was enormous attention on the 100MW South Australian battery. This space is not the time to comment on that battery at length (it is done here) but we would say:

- Using batteries for time shifting of electricity consumption, ie using PV and wind to charge batteries to consume power on demand, is likely to be far more cost effective, when all costs are considered, if the batteries are installed at the fringes of the grid, and behind the meter.

- Utility scale batteries are finding that their best economic application right now is for frequency and voltage control. That’s how they are being deployed in the UK and in South Korea.

- Despite the wonderful advantages that lithium batteries have for fast installation, small amount of space, excellent fast power characteristics it’s likely that the best overall solution in large grids, ie South Australian size and up, will also include other forms of storage such as pumped hydro or possibly biomass or CST. On paper if you want four-six hours of time shifting of energy for say 200MW (ie 800 -1000 MWh) then pumped hydro is way cheaper than lithium batteries. Lithium battery price may come down enough or the pumped hydro price may go up enough to change this but that’s the way the spreadsheets look right now.

- So to our way of thinking the complete system has (i) household and commercial batteries behind the meter (ii) utility batteries to cover grid stability and short duration power issues (ie wind stops blowing briefly, clouds cover a pv site) and (iii) lower cost, large scale energy storage. For that reason one of the most significant announcements we look for this year is a commitment by Energy Australia to invest in the proposed salt water pumped hydro station in South Australia.

Turning to the weekly action

- Volumes: Were down this week other than in Tasmania. Overall across the NEM for the calendar year to date consumption is flat despite the very hot weather at the start of the year. That’s despite 2% growth in NSW.

- Future prices fell in Qld and NSW but rose in Victoria. The two speed nature of electricity prices is becoming more evident by the day. Qld is forcing prices down, this flows to NSW but doesn’t flow to Victoria. Victoria is stuck with relatively expensive open cycle gas setting the price for the next 12 months. I call this the “Portland Price”.

- Spot electricity prices were 20-25% lower than last year in QLD and NSW although still around the $75-$85 MWh mark. The spot price in Victoria was $133 MWh – actually 1% higher than in South Australia.

- REC No change.

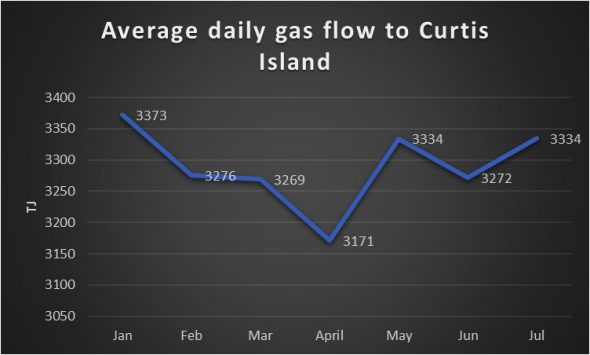

- Gas prices Gas prices are now obviously lower than last year and in QLD were just $7.1 GJ although still above $9 GJ in the Southern States. As far as we can see this is not due to any reduction of gas flowing to Curtis Island, although supply was down a touch in June. Gas generation is higher than a year ago so it looks like Turnbull’s regulatory push is working even before being formally introduced.

Utility share prices

- AGL shares have been a little soft recently following there very strong run over the past couple of years. Tiny Genex shares have done well following what is effectively QLD govt support for transmission. The Kidston pumped hydro project is in the middle of nowhere but with the help of QLD Govt and ARENA they may yet make a go of it

Share Prices

Volumes

Base load futures, $MWh

Gas prices

David Leitch is principal of ITK. He was formerly a Utility Analyst for leading investment banks over the past 30 years. The views expressed are his own. Please note our new section, Energy Markets, which will include analysis from Leitch on the energy markets and broader energy issues. And also note our live generation widget, and the APVI solar contribution.