From humble beginnings, batteries for energy storage are now deservedly having their time in the spotlight.

There have been other emerging technologies that have been through their own processes of development and then commercialisation, to become widely-accessible sources of energy generation and security.

From promising but expensive prototypes, they transitioned to become mass-produced and readily deployable systems.

Now it’s time for large-scale energy storing batteries. They provide energy systems with valuable energy security and reliability to be the superpower in the world’s transition to 100 per cent renewable energy.

Batteries: the system enablers

Batteries are a systemic enabler of a major shift to bring industries to net zero carbon emissions by coupling industry to transform renewable energy from an alternative source to a reliable base.

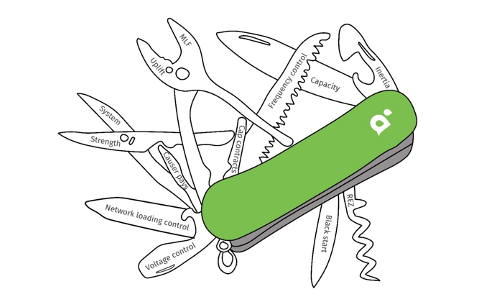

They have been described as the Swiss Army Knife of electricity grid infrastructure (Figure 1); in that they can perform a whole range of different functions.

They can ramp up with exceptional speed to provide precisely the power needed by the grid under a range of scenarios, such as for frequency response, or to support an interconnector.

Placed at strategic locations around the grid, for example, incorporated into planning for new renewable energy zones or at strategic points within networks, batteries can:

- Maximise the generation potential of a region’s utilisation of transmission assets

- Avoid costly network investments that would otherwise be required

Some of these services have been demonstrated by examples such as the Hornsdale Power Reserve and Victorian Big Battery, among others, for the crucial role it plays in both energy system security and energy affordability.

It is playing a major role in stabilising system frequency upon large contingency events and ensuring considerable savings in ancillary services costs (Figure 2).

Most battery storage systems deployed in the National Electricity Market have, to date, leaned on funding support agreements to supplement revenues obtained in the energy and frequency control ancillary services (FCAS) markets to build a viable business model.

Now, market actualisation that enables commercial projects without reliance on external funding is essential to see them realise the levels of deployment forecast for them – a similar process to what we saw with wind and solar.

Technical and market insights for best possible business case

With the stack of revenue opportunities potentially available to a large-scale battery storage project, the big question facing developers is how to make sense of the options and trade-offs involved; how to design a project that delivers the best possible mix of services to the grid and business case for the project.

The stack of services available to a project must be defined. Technical performance data needs to be integrated. Operating strategies and their impacts on different services must be considered and forecast market revenues modelled.

Opening up additional revenue streams will require more sophisticated business cases for battery projects that incorporate complex technical and market interrelations.

If batteries are to prove their worth as the Swiss Army Knife of grid infrastructure, greater innovation, nuance and optimisation needs to occur.

Four areas to focus to ensure batteries prove their worth

The true value-stacking potential for large-scale batteries will be realised through continued development in the following areas:

- Capability: System operators, networks, technology providers and project developers alike have a major stake in proving up the capability of batteries with advanced grid forming inverters to provide the range of services touted for them. Successful demonstration projects will build experience and confidence that the technology can be reliably deployed to meet the energy system’s most challenging problems.

- Reform: Further regulatory reform is needed to equip the energy market rules of the 21st century with enabled technology for the future energy transition to be most efficiently deployed. Significant reforms have been adopted and are in progress, but more is needed to realise the full value that batteries and other future energy technologies have to offer.

- Collaboration: The optimal integration of batteries requires deep understanding and collaboration between stakeholders. Developers, for example, need detailed insight into the emerging challenges facing network service providers, and to understand the opportunities for targeted support services.

- Tools: Sophisticated tools for analysis of aspects including revenue opportunities, sizing optimisation and technical performance will be needed to achieve optimum outcomes for any given opportunity.

There is no one-size-fits-all approach when it comes to designing and de-risking battery projects. Each project, and site, must be analysed and assessed to determine the best project design and mix of services to achieve positive technical and commercial results.

The next decade will be a fascinating time for large-scale batteries and battery storage with the rapid growth of innovative technology set to change the decarbonisation landscape.

Battery evolution as the energy system changes

As Australia pushes forward with decarbonising its energy system, it will be managed quite differently to how it is today, and batteries are ideal providers of many of the services that will be needed.

Traditionally, key energy system security services such as inertia, system strength, and system restart services have been provided by synchronous generators, either by default as an inherent characteristic of their operation, or under contract for system restart services.

However, as coal and gas generators retire, or, have much of their generation subsumed by renewables, the baton for these services must pass to alternative technologies. Batteries with advanced grid forming inverters will have a crucial role to play.

The demand for increasing volumes of firm, dispatchable, energy capacity will come from all corners of the country as thermal generation facilities are progressively retired, and customers demand ongoing energy affordability and reliability.

The Australian Energy Market Operator (AEMO) has modelled the requirement for energy storage to be 45 GW and 620 GWh by 2050, with battery storage one of the key technologies.

By that stage, the energy system will be relying heavily on medium-duration storage of 4 to 8+ hours duration for daily energy shifting to meet supply and demand.

Before these demands are upon us, strategic investments in transmission infrastructure and renewable energy zones (REZs) are required to efficiently connect renewable generation to the network.

These will unlock the wind and solar generation needed to progress to net zero carbon emissions, with large-scale batteries integrated to play crucial roles.

They enable greater build-out of renewables in each REZ, maximise utilisation of transmission investments, and reduce marginal loss factors to improve revenue margins.

Regulatory reform – keeping up with change

This rapid growth creates new challenges for the energy market rules to adapt to the evolving technology mix. Finding the right policy settings to ensure the grid remains secure and reliable while efficiently integrating new technology to keep pace with the transformation will be crucial.

The transition is underway.

Energy market 5-Minute Settlements came into effect in October 2021, making a splash through better incentives for fast responding, flexible generation and storage.

Changes to how energy storage can be registered in conjunction with other generation such as wind and solar are also a positive development towards a more efficient registration process and flexible operation.

Another key, but complex reform, is in how system strength is defined, procured and managed. A recent system strength rule change determination by the Australian Energy Market Commission (AEMC) is a positive step.

It recognises the potential that grid forming batteries have in providing this service and establishes a framework that allows renewable energy developers and networks to deploy them in efficient ways that will minimise total costs to end consumers.

A change in progress is the proposed fast frequency response market which will look to equip the energy system with the response capability needed to manage major system security events that occur from time to time.

Planned incentives for primary frequency control should also be a step forward in recognising the value that batteries and other generators currently provide without charge.

Further clarity would also be beneficial in other areas, including in how storage projects should best be allocated network use of system charges such that demand on the network, and value provided, are appropriately considered, and that projects can be developed with confidence as to any costs that may be incurred.

Progressing these and other reforms will be crucial to driving the decarbonisation transition of the national energy market as efficiently as possible.

Steve Wilson is technical director, Power Generation, at Aurecon