Australia, you will read almost anywhere, aims to be a global renewable energy superpower, even a renewable hydrogen superpower – in much the same way it does in fossil fuels, where it is one of the world’s three biggest exporters.

But despite Australia’s great natural advantage – huge resources of wind and solar and a massive, relatively unpopulated continent to host them, along with technical know-how – the hype, or hope, from business and politicians is yet to be matched by real and actual projects.

These tables below, presented by Gero Farruggio from Rystad Energy at this week’s Clean Energy Summit, illustrates the yawning gap between promises and delivery.

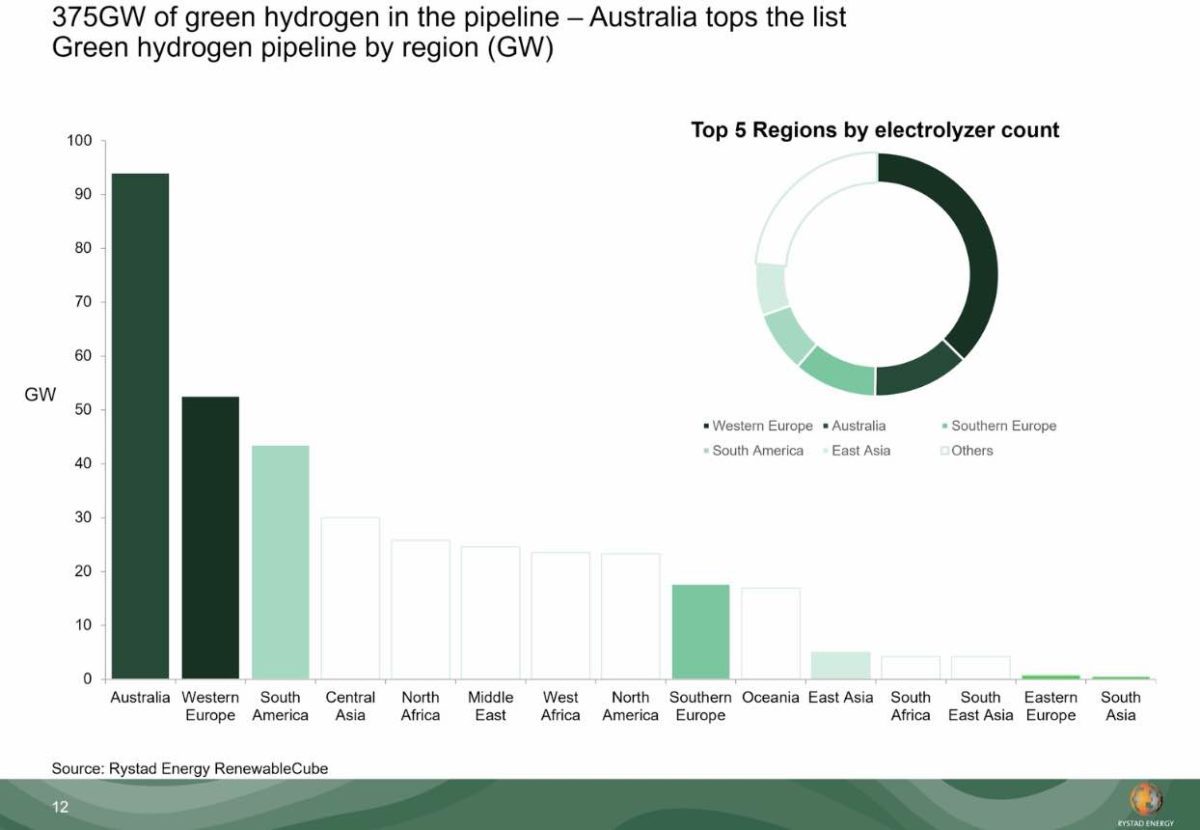

The first graph shows that Australia easily tops the global list when it comes to an announced “pipeline” of green hydrogen electrolyser projects, with some 95GW out of a global pipeline of 375GW.

The first graph shows that Australia easily tops the global list when it comes to an announced “pipeline” of green hydrogen electrolyser projects, with some 95GW out of a global pipeline of 375GW.

That figure is boosted by the multitude of huge project, such as the massive Asia Renewable Energy Hub, now backed by BP, the Western Green Energy Hub, and others.

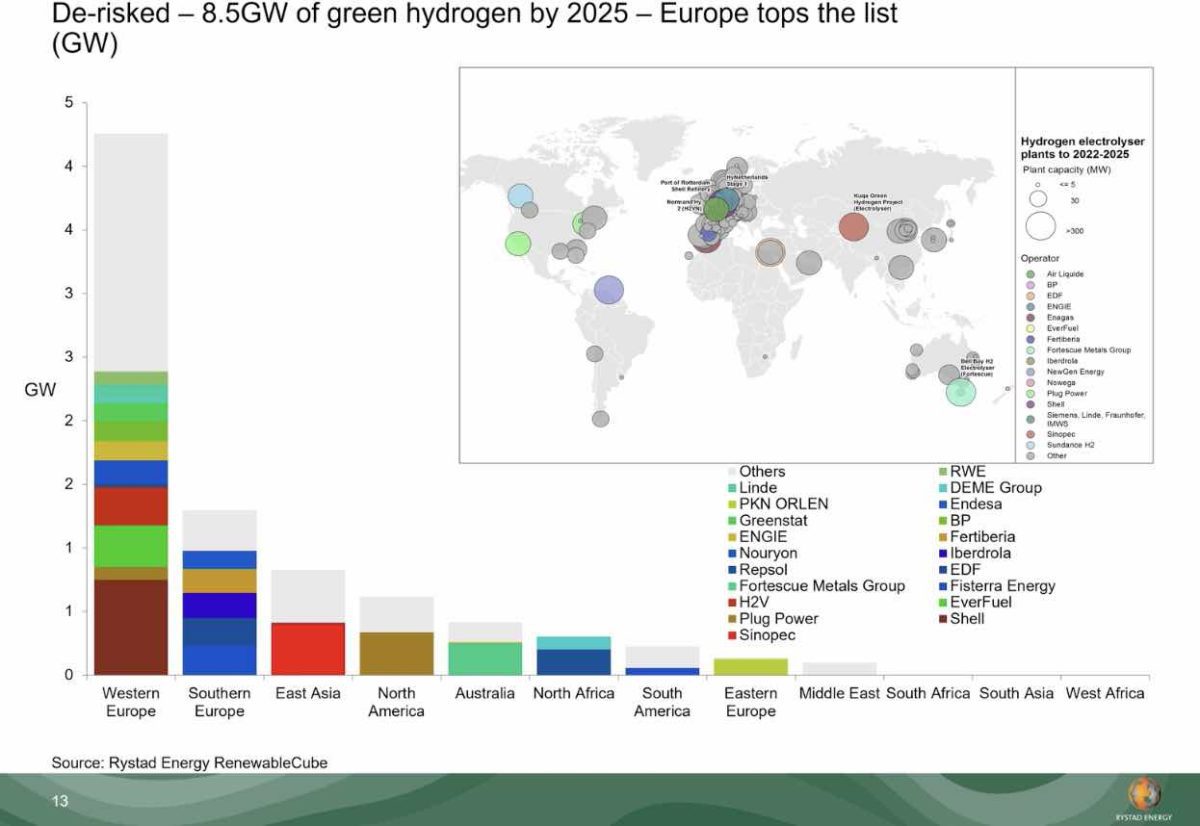

But when it comes to actual delivery, Australia is well back in the field, with less than 1GW out of a total of 8.5GW of what Rystad considers to be “de-risked” projects. i.e. those projects that are considered likely to go ahead by 2025

On this count, Australia ranks well below western Europe, and behind southern Europe, east Asia and north America.

This is despite the promises made by the likes of Andrew Forrest to deliver 15 million tonnes a year of green hydrogen production, and the WA government’s goal of having 100 million tonnes by 2030.

To be fair, Forrest has never said all of that green hydrogen will be produced in Australia, and the Bell Bay project pushed by his Fortescue Future Industries is included by Rystad as the most significant “likely” project in Australia to be underway by 2025.

And the company is building the country’s first electrolyser manufacturing facility in Queensland, which should start production late last year.

What’s going on?

“Australia is yet to see a single large scale project secure financial close,” says Anna Freeman, the head of hydrogen policy at the Clean Energy Council.

“I think we may just have cracked one megawatt. Those proponents at the fore of project development in Australia face significant challenges to make their projects economically viable.

“So how do we get a new green energy industry up and running from a standing start? What is the reality on the ground? And what can we learn from our past public policy successes and failures in order to seize one of the biggest market opportunities for the renewable energy sector of the next over the next 30 years?”

Rystad’s Farruggio says Europe is forging ahead because the demand is clearly there – accelerated by the pressures on gas supplies from the Russian invasion of Ukraine, and soaring fossil fuel prices across the board.

“The projects that we think will be energised by 2025 represent about 2% of that pipeline, or 8.5GW. That’s about 180 projects over 33 countries, and about 30 projects will probably be energized this year,” Farruggio said.

“And the average size of that electrolyzer will probably go from started the year about four megawatts to about 80 megawatts over that period. Asia will keep up with Europe for the next couple of years in terms of capacity installed. But then after that Europe really takes off.”

Farruggio says Australia is trailing the world because, unlike some other countries, it has no stated capacity target, and its funding for projects – despite its huge wind and solar resources – is ranked at number 10 among the nations competing for a lead role in this transition.

“Australia is at the bottom of that committed spend among the top 10 governments, and if you look at the capacity targets … the top five countries have committed about 55 gigawatts of electrolyzer capacity by 2030.

“Australia does not have a capacity target, maybe we should. So we can’t compete on policy at the moment.” And despite its great wind and solar resources, it may find it hard to compete on costs with the US and the Middle East.

Daniel Kim, the head of Ark Energy, which is looking to take its parent company’s Sun Metals zinc refinery in Queensland towards zero emissions, says cost curves associated with “all things hydrogen” at the moment are prohibitive.

“That’s that’s the fundamental problem. And it’s not just the electrolyzers, it’s the storage, it’s the compression, it’s the dispensers, it’s the tube trailers, the cost of the fuel cell electric vehicles.

“The real kind of lesson for us is that cost curves don’t come down as a function of time. They come down as a function of proponents, making FID (financial clos), ordering this kit and through that scale of mass production, then leads to technology advances, etc. That’s when that’s when the cars come down.

“Of course now we’ve also had the supply chain challenges have exacerbated projects that have been on the cusp of making FID which has also made it challenging.

“So in a sense, it’s there’s a little bit of a chicken in the egg here. I think what it what underpins for me is firstly that there is still a role for governments at all levels to help stimulate the production side. But I think equally it’s important to look for genuine use cases.”