It has recently hit the news that New South Wales transmission company Transgrid is seeking to pass-onto consumers $1.1 billion of a $1.5 billion blow out in the construction costs of Project EnergyConnect.

It’s important to put this blow-out in context, because it is by no means a small blow-out. Originally when Transgrid persuaded the Australian Energy Regulator to approve this project as good for consumers, it was projected that its share of the project cost would be $1.82 billion.

So under Transgrid’s watch this project’s cost has blown out by 82%. It’s also not small relative to the size of Transgrid’s overall asset base, which was $7.65 billion in 2021-22.

One would expect that one of Transgrid’s core capabilities that consumers pay them for is the management of construction risks associated with building transmission lines. But according to Transgrid’s shareholders they shouldn’t have to bear even a third of this risk.

Yet this is just the tip of the iceberg for a far bigger issue: if the shareholders in network monopolies aren’t prepared to wear the core and highly obvious risks associated with their business, why did we privatise these things in the first place?

This extends well beyond Project EnergyConnect to issues related to whether electricity and gas network shareholders should be immune from any loss in revenue associated with declining consumer demand for network capacity due to electrification (for gas networks) or energy efficiency, solar and batteries (for electricity networks).

Our electricity networks and a large proportion of our gas networks were constructed by government entities who were able to finance construction at very low interest rates linked to government bond markets.

Governments in Australia as well as those of major stable economies around the world can raise finance at interest rates well below what competitive market-exposed private sector companies can do because of their ability to raise incomes by fiat via taxes, as well as their ability to set prices for certain goods if they wish.

So why on earth would we hand this role to the private sector and pay them a significant premium over and above what government can finance this infrastructure for?

This is an especially pertinent question in relation to network assets when you consider:

– The vast majority of the costs associated with energy networks relate to paying for their construction and therefore paying back financiers. The operating and maintenance costs are small.

– These provide an essential service that has historically been a monopoly, so until very recently we have had limited ability to rely on competition to discipline providers to keep their prices to consumers aligned with efficient costs.

Yet we privatised them, nonetheless. Or in the case of Queensland and NSW electricity networks, we regulate them as if they were a wholly private sector entity that was dependent on private sector financing options. This was a bit of a half-way house towards privatisation known as corporatisation, but with NSW then following through to sell a large ownership stake in these networks (like Transgrid) to others.

The argument for why we did this was built on experience over the 1980s when it became apparent that government-owned, vertically integrated electricity companies (spurred in part by politicians’ wishes) had been far too keen to spend money building new capacity without adequate regard to whether this capacity was needed or could be deferred.

In power generation, in particular, we had vastly more coal power generating capacity than needed. We were told that, by privatising these assets, the new private sector owners would be far more disciplined about spending money on new capacity, because if they built expensive capacity for which there wasn’t the demand, then they’d end up losing money and shareholders would quickly put that to a stop.

Should network shareholders be a protected species?

But when it came to energy networks we’ve failed to put the regulatory structures in place to ensure shareholders faced the same discipline that power generators face. That is: if you fail to properly read market demand and technological change and the market ends up with too much capacity, then you will pay the consequences for that error by losing money on that investment.

Instead, in energy network regulation under our national regulatory regime that began in 2008, we provided shareholders (which perversely included Queensland and NSW state government treasuries who got to write the regulatory rules) with a free, one-sided option.

If demand grows then you can keep that upside. But if demand goes down, or just doesn’t grow in line with the forecast you demanded the regulator accept for fear of supply outages? Well, you get to keep whatever you could fool the regulator into accepting.

What compounded this error is that while we’ve eliminated much of the risk facing these company’s shareholders, we’ve also assumed financing costs that assume that they do face meaningful risks.

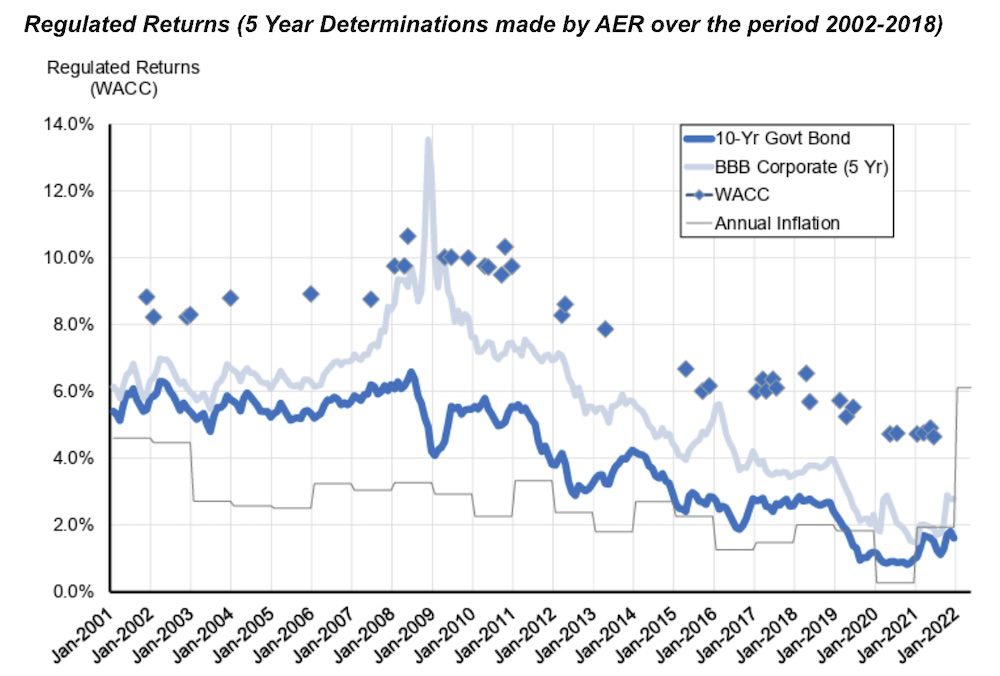

This is embodied within weighted average costs of capital (WACC) decisions that are far higher than government bonds, as illustrated by the WACC diamonds in the chart below which sit several percentage points higher than the dark blue 10 year government bond rate.

Yet not only that, network shareholders also get to recover extra costs associated with above-normal inflation while those that buy government bonds have to cop that loss on the chin.

Plus, there are a range of other opportunities for networks to earn extra returns over and above the regulated WACC that mean electricity network shareholders made profits 70% greater than the regulator allowance, while gas pipeline shareholders made profits 90% greater than the regulator allowance.

This one-sided option regulatory framework has created an incredibly perverse incentive for dishonest behaviour by energy networks. There is no penalty for lying to the regulator, only upside.

What makes this worse is that while we assumed the owners of these networks faced costs of capital in line with risk-facing private sector entities, many are still government entities.

That obviously includes the Queensland and NSW State Treasuries, but also the Singaporean Government (Singapore Power), the Chinese Government (State Grid Corporation of China), Qatari Government (the Qatar Investment Authority); and several Canadian Governments’ public sector pension funds.

This has opened up the opportunity for these government entities to make a tidy sum arbitraging the difference between the low cost they pay to raise capital versus what the regulator lets them charge Australian energy consumers.

These distorted incentives led to tens of billions of dollars being spent expanding network assets that means we now have electricity networks with vastly more capacity than residential consumers need across large parts of east coast of Australia (note to dynamic pricing enthusiasts: the Australian Energy Market Commission has stated these won’t apply in areas of the network that have spare capacity – which is most of it).

It also means that gas networks have encouraged and eagerly connected lots of additional customers to their networks with little concern to whether long-term use of these pipelines was consistent with governments’ climate change goals.

Is the customer always right, or should the customer be forced to compensate for the network planner’s errors?

Meanwhile, large rises in the prices of electricity and gas have led consumers (often encouraged by governments in order to lower carbon emissions) to look for technological substitutes to using these networks – more energy-efficient equipment (which includes electrifying gas appliances) as well as solar and batteries.

Unfortunately, our energy rule maker – The Australian Energy Market Commission or AEMC – thinks consumers should be permanently saddled with the costs of this network capacity which they don’t need to use, through forcing a fixed charge upon them which they are unable to avoid, irrespective of their demand for network capacity at peak times.

Quite incredibly, those keen on this idea try to paint households that choose to be energy efficient, or adopt solar and batteries, or who are just frugal in their use of energy, as being free-loading, cross-subsidised parasites on the energy system.

This is an extraordinary reversal of the adage that the customer is always right. Instead, we have a group of people that want us to believe that the production planner is always right.

Meanwhile customers that don’t conform to a planner’s forecast have done something wrong and should be made to pay more to compensate for the planner’s error. Not only that, apparently these people should be punished for the fact that landlords’ failure to provide well insulated and energy efficient homes has left renters especially vulnerable to network monopolies.

Side note: A household with a battery will place a low burden on the need for network capacity during the peak period even in winter

At this point, I should note there is a myth and a red herring promoted by both the AEMC and other supporters of hiking the fixed charge. This is that households with batteries and solar should have to pay the same as an energy guzzling household because the solar and battery owner will place a burden on peak grid capacity equivalent to what they would have done without solar and battery system.

The reasoning is that in winter there will be times when the solar panels will be unable to fill the battery and the battery won’t do anything to reduce the household’s load on the network at the peak demand period (usually between 4pm to 9pm).

This is a myth because the typical battery being installed in households is 20kWh or more and can easily cover most household’s peak-period load even if they’ve fully electrified. Sure, it may not be able to fully charge off solar, but under the existing tariff rules there is an incentive for the battery to be charged up from the grid at an off-peak period. So their need for grid capacity at the peak period will remain far lower than other households.

It is also a red herring because, if you just stick with the existing rules for cost-reflective pricing where people are required to pay high charges during the peak demand period (which could be via a demand charge or even a dynamic network charge), that solar and battery household will pay a high charge for the network anyway, if they turn out to use a lot of network capacity at the peak period.

There is no need to shift to a fixed charge in order to ensure fair cost recovery for solar and battery owners who might still push up network peak demand due to a failure to charge-up their battery.

Escaping the absurdity that networks are always right even when they’re wrong

The AEMC and also the Australian Energy Regulator (AER) have attempted to blinker our vision to one where consumers who have made network forecasters look stupid are somehow to blame for the plight of renters dealing with an uncomfortable home that is costly to keep warm. This is completely and utterly absurd.

It just doesn’t have to be this way, and it shouldn’t be this way.

There is an imminently sensible option available to our regulatory institutions (which oddly they have studiously avoided mentioning) to deal with declining demand for network assets. It would involve the regulatory rules being changed to embody a principle that most consumers take for granted – that customers should only pay a supplier for what they actually need and use.

Back in 2012 the Major Energy Users proposed a change to the regulatory rules. This would require the regulator to review the valuation of all network assets when assessing the asset base as part of a network revenue determination to ensure only necessary assets, appropriately sized for the service, are included in the asset base.

The asset base would only allow a return on assets to the extent they are used by consumers. In other words, if network assets were deemed to be excess to customers’ needs they would be excluded from earning revenue until such time as they were needed.

At the time, the AEMC rejected this rule change request claiming, “Little empirical evidence has been provided on the extent to which electricity network assets are under-utilised.”

Well several years down the track that empirical evidence is now in (although it was pretty obvious even back then). Below is a chart of distribution network utilisation by state based on maximum demand (not average) versus peak transformer capacity by state published by the Australian Energy Regulator.

Across all jurisdictions network utilisation is substantially worse than it was in 2006 when the AER began collecting these statistics (with the exception of the Northern Territory which has always been horrible). It’s now over a decade since the AEMC declared they needed to see more evidence and network utilisation hasn’t shown any sign of a dramatic turnaround of improvement.

Source: Australian Energy Regulator – Electricity and gas networks performance report 2025

The path forward

I would be a bit more sympathetic to networks than the Major Energy Users through modifying their proposal somewhat.

Sure, the owners of these networks can hardly claim they couldn’t have foreseen that climate change was serious problem that governments would seek to address by promoting electrification, energy efficiency and renewable energy. Nor could they have been blind to the threat that solar and batteries could achieve widespread adoption that would provide a competing substitute for networks.

But electricity networks are incredibly valuable in sharing energy resources and will need continued investment, so it would be better to minimise the pain to investors where reasonable. And it’s fair to say that our regulatory institutions haven’t done a good enough job in making it clear to owners of networks that financing premiums over the risk-free rate came with a sting in the tail – you have to accept some risks in return.

The first step to soften the pain would be a grandfathering clause – gas and distribution networks could get to keep the value of whatever assets they’ve built up to 2025 provided demand for those assets remains the same or higher than it was over the prior regulatory determination.

But if consumers’ need for network capacity declines from this historical benchmark, then the network’s asset value and revenue would be re-optimised in line with the decline in demand for capacity.

Transmission networks, however, need to be treated differently. This is because they are built not just to meet peaks in customer demands, but also to transfer power from areas rich in energy resources to where they can be consumed. This can mean those assets are sized to cater for peaks in supply driven by wind or solar availability that often don’t coincide with peaks in end-demand.

That brings us to the other way to help compensate networks, which is that power generators should take on some of the cost of paying for the network (as they do in many other countries), particularly the transmission network.

But this shouldn’t be applied just to households that export power from their solar and battery systems, it should apply to all generators. And the cost should be apportioned in line with the value of network assets those generators need to use to get their power to end customers.

It is ridiculous that in our wholesale electricity market a generator hundreds of kilometres from the consumers that it supplies is treated the same as a generator located a few metres away from end-consumers.

Likewise, if a generator provides power to nearby customers at a time when the local network capacity is close to its limits and saves those customers the cost of a network upgrade, then the generator should be paid for that service.

Importantly such reform should not absolve incumbent generators from bearing network costs (usually justified on the basis that the cost of the existing network is already sunk), otherwise it will favour fossil fuel generators, and act as yet another barrier to decarbonising our energy system and enhancing competition.

Such changes would result in a far fairer system for recovering network revenue that recognises network shareholders and generators are part of the overall equation, not just consumers.

Also, unlike what the Australian Energy Market Commission proposes (hiking fixed charges, while dropping energy charges for the vast majority of households), it would provide much better pricing signals for developing a power system that can decarbonise on a timely and cost-effective basis.