“A mother was bathin’ her baby one night

The youngest of ten, a poor little mite

The mother was fat and the baby was fin

T’was nawt but a skellington wrapped up in skin

The mother turned round for the soap from the rack

She weren’t gone a minute, but when she got back

Her baby had gone, and in anguish she cried

“Oh, where is my baby?”, and the angels replied

Your baby has gorn dahn the plug’ole

Your baby has gorn dahn the plug

The poor little thing was so skinny and thin

He shoulda been bathed in a jug”

Cream, 1964

Ever since the renewables element of the National Energy Guarantee was killed off the Energy Security Board has started to get on with some real work. Firstly it got behind AEMO’s ISP and is doing its best to hurry transmission investment along.

In our view, it will be a tough task.

Its latest initiative is to prepare advice for COAG by the end of 2020 on the post 2025 market design for the NEM. The ESB states that changes to design will need to satisfy the National Electricity Objective [NEO].

We note that the NEO doesn’t have an emissions objective. However, the explanatory document does contemplate that changes in the NEO might be required to accompany changes in market design.

Notwithstanding the long time frame, very significant work is going to happen this year. A partial extract from the ESB’s explanatory document notes a timeline as follows:

“June-August 2019 – Identify options for the provision of the full range of services required to deliver a secure, reliable and lower emissions electricity system

March-August 2019 – Assessment of different international options for electricity market design

September 2019 – Stakeholder consultation on the options for the provision of the full range of services required to deliver a secure, reliable and lower emissions electricity system at least-cost to customers

December 2019 – Identify two potential options for the provision of the full range of services required to deliver a secure, reliable and lower emissions electricity system at least cost to customers (in addition to the current market design).

December 2019 – Undertake broad stakeholder consultation on two potential options for post-2025 market design.

To assist the ESB will have an internal working group, an advisory paneland a technical working group.

There are several issues with the current market design

Just off the top of my head.

Merit order based dispatch becomes less and less useful in a world of very low marginal cost wind and solar. In the case where wind and solar generation exceeds demand it becomes a negative bidding contest. Perhaps there is nothing wrong with that but its worth thinking about. It also goes to new investment when marginal units of solar will be curtailed if the excess generation isn’t stored.There is increasing Govt involvement in generation and this wont always be driven by standard micro economic profit maximising behaviour including investment decisions;

Vertical integration is now a major feature of the market

Events over the last few years have lead many observers to conclude that Goverments will only allow markets to work properly when prices are low.

Although capacity markets round the world have largely not been seen as successful, there is equally a question over whether energy markets can produce firming capacity in a timely fashion.

It can be argued for instance that there would be no need for a reliability guarantee if the energy only market was achieving the reliability function appropriately.

Above all else there is clearly a need: a need that no amount of politics can ever eliminate, to incorporate emissions reduction into electricity policy. One strong argument is to build such policy into the NEO.

There are other important details such as whether marginal loss factors are appropriate in major transformation of markets.

The formal integration perhaps ofDER, particularly if Govt policies continue to foster its development complete with household storage.

None of this need necessarily mean throwing out the baby with the bathwater as the energy only market in the NEM has generally been held in good regard.

The market action

Electricity futures continue to crawl up in the out years. Policy makers should ask themselves why with so much new supply coming on are 2021 flat supply futures at >$80/MWh in most regions.

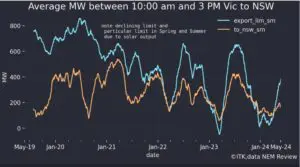

We think part of the blame has to come back to AEMO and the AEMC for the uncertainty around transmission investment, system strength and MLFs. The rule makers are not keeping up at the moment although they certainly are trying.

Figure 7: Commodity prices. Source: Factset

Volumes

Perhaps its imagination but is there a trend for these January volume spikes to be getting more pronounced?

Figure 8: electricity volumes. Source : NEM Review Figure 8: electricity volumes. Source : NEM Review

Base Load Futures, $MWh

Figure 9 Baseload futures Financial year average. Source: ASX Figure 9 Baseload futures Financial year average. Source: ASX

The futures curve, particularly in NSW out in 2020 and 2021 continues to drift up.

Figure 11 30 day moving average of Adelaide, Brisbane, Sydney STTM price. Source: AEMO Figure 11 30 day moving average of Adelaide, Brisbane, Sydney STTM price. Source: AEMO

ORE’s lithium business remains on the nose with investors, Windlab seems to be making a recovery from its Kennedy delay problems.

The market is giving AGL a thumbs up with the share price up 11% since the start of the year, but the yield related investments APA and AST have done very well from the fall in bond rates. Those falls make yield more attractive in a relative sense.