“So I told my dad “I drove your car to the party and was drinking, but my friend who wasn’t drinking drove your car home.”

My dad said, “Son, I’m a used car salesman, Don’t bullshit a bullshitter.”

Bring on the elections

Your analyst is in favour of parties that have stronger policies on climate change and decarbonsiation. It’s as simple as that. We think the Queensland State Election shows that on balance elections can be helped by policies that favour decarbonization.

Lily D’Ambrosio, Energy Minister in the Victorian Government doesn’t have nearly as impressive academic qualifications as Angus Taylor, Energy Minister in the Federal Govt and yet under her stewardship Victoria has a sensible electricity policy, one which has been carefully developed over a a number of years, takes on board feedback from stakeholders, will increase supply, lowers risk, increases predictability and decarbonizes the Victorian electricity sector at pace.

You only have to listen to D’Ambrosio, as I did at All Energy and at the earlier CEC event, to realise that good policy stems from good leadership. And good leadership is about bringing the best out of a team and getting everyone to buy in to a shared objective. It also requires courage to stay the course and a modicum of talent.

By contrast the Federal Govt. nailed its electricity and decarbonsiation colours to the mast with the appointments of junior burgers Angus Taylor and Melissa Price. It’s totally clear and hardly worth discussing that at best, at best I say, the Feds will pay lip service to climate change and have zero interest in any action.

Large parts of the coal industry are controlled by overseas investors, but this matters less than the export dollars, the royalties and a view that the “base” doesn’t care about science. The Coalition may not lose the Federal Election on this issue alone but on this issue they surely make themselves look stupid to anyone with an education.

ESB gets behind the ISP – Riverlink will likely go ahead

We were critical of the modelling that underlay the NEG and therefore we were critical of the ESB which commissioned the modelling. That’s history. The ESB has quickly moved on from the NEG to looking at how policy needs to be modified to accelerated stage one and potentially stage 2 of the ISP.

As a reminder Stage 1 of the ISP has 3 steps:

- Increase transfer capacity between New South Wales, Queensland, and Victoria by 170-460 MW.

- Reduce congestion for existing and committed renewable energy developments in western and north-western Victoria.

- Remedy system strength in South Australia.

Capital cost about $550 million or say annual finance cost of $40 million, which is a trivial 0.1% of NEM wide annual revenue of say $39 billion.

Stage 2 of the plan is:

- Establish new transfer capacity between New South Wales and South Australia of 750 MW (RiverLink).

- Increase transfer capacity between Victoria and South Australia by 100 MW.

- Increase transfer capacity between Queensland and New South Wales by a further 378 MW (QNI).

- Efficiently connect renewable energy sources through maximising the use of the existing network and route selection of the above developments.

- Coordinate DER in South Australia.

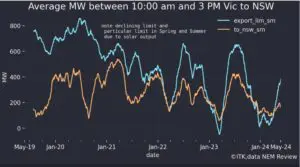

The Riverlink interconnector is very important in this group. We think Riverlink is virtually certain to go ahead. This means it’s hard to justify building a pumped hydro or gas plant in South Australia.

We expect all those proposals to stay on hold for the time being. Bottom line nothing is going to change in South Australia until Riverlink opens. The exception to this could be household batteries. If there are enough they could smooth out some peak pricing and reduce the opportunity for gas.

Equally, the interconnector will likely open up massive opportunities for new wind and solar plants along its route. You only have to look at the map of stage 1 and 2 to see the opportunity.

At All Energy, ESB chair Kerry Schott expressed a view that there may need to be some revision of the controversial RIT-T test. The ESB has issued a consultation paper that will consider options as to how to implement the ISP. Without going into the detail we expect that:

- There will be an increased focus on the timeliness of delivering the Stage 1 proposals. These are uncontroversial and just require lots of “i” dotting and “t” crossing and can be expedited.

- The ESB will lean toward the more “aggressive” side of the 5 options identified by an AEMC paper to make the ISP more actionable. Those options are:

- Option 1 – TNSP decides on transmission investments but is required to consider ISP-identified investment needs in transmission annual planning reports and regulatory proposals

- Option 2 – TNSP decides on transmission investments but is required to conduct RIT-Ts on ISP-identified investment needs and options

- Option 3 – In addition to the ISP identifying investment needs and options, AEMO determines the “best” option for transmission investment but the TNSP is still able to determine how to most efficiently meet that option e.g. to take into account local conditions

- Option 4 – AEMO determines the “best” option for transmission investment and directs a TNSP to proceed with the “best” option, although the TNSP can still choose the functional specification of that option

- Option 5 – AEMO determines what transmission investment is necessary, including the functional specification, and directs a TNSP to implement that investment.

The market action

This is the first “Know Your Nem” for some weeks. What we see is:

Consumption in front of the meter is flat but spot prices are up. This is I think due to some Victorian generators not running all units all the time. Futures prices have largely stayed flat with some minor moves round the edges. However, for the most part cap prices are above last year.

Gas prices, as expected, have moved above last year and this to is contributing to high spot prices. Share prices are torn between the opportunities offered by the lower dollar, through to the negatives from higher USA bond rates (but rates in Australia are flat).

Oil prices have jumped and in A$ terms are up 20% year on year. This pushes up gas export prices and domestic gas prices. Coal remains very elevated albeit unchanged from a year ago. What this means is that as domestic coal contracts in NSW roll off the costs for thermal generators are going to increase, perhaps quite a lot.

The recent problems with the ageing Chain Valley coal mine in the Newcastle show that costs in coal minining are high and so high prices are required. Maybe prices don’t have to increase to spot levels, adjusted for quality, but they need to be a lot higher than Vales Point B is paying.

The oil and coal prices are in line with expectations, what’s really catching the eye recently is the jump in the USA 10 year treasury note to 3.23% a full 50 bps above Australia. Only Greece has a higher rate of countries regularly covered by Factset.

Share Prices

Volumes

REC Prices

David Leitch is principal of ITK. He was formerly a Utility Analyst for leading investment banks over the past 30 years. The views expressed are his own. Please note our new section, Energy Markets, which will include analysis from Leitch on the energy markets and broader energy issues. And also note our live generation widget, and the APVI solar contribution.