- Volumes : were once again soft, back at 2014 levels across the NEM. For the CYTD volumes across the NEM are flat despite QLD’s 4% growth. If you think that energy conservation and energy efficiency is an important part of decarbonisation this is a great result. As we will continue to point out, the electricity industry, the environment, and consumers could all be big winners if Australia did a bit more to promote electric vehicles. We think the powerful lobby group of AGL, ORG and EnergyAustralia are missing a trick here.

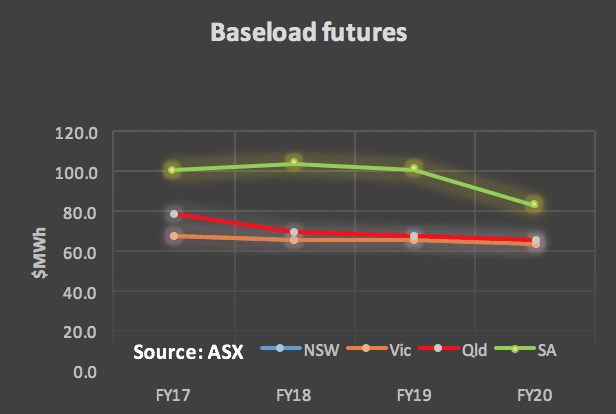

- Future prices: Well of course this is the big news with dramatic jumps in even the FY17 futures price. One of the points about the Hazelwood closure is that Engie has to cover Hazelwood’s contracts. That is they have to buy back or make other arrangements for the electricity Hazelwood had previously agreed to sell beyond the closure date. The June 2017 contract is arguably the most impacted. Engie couldn’t buy those contracts back prior to announcing closure because that would be insider trading. Still the point is that buying pressure is probably pushing prices beyond their natural level. We will have more to say about this, but the long and the short of it is, forecasting prices is a mug’s game. Pundits can’t even forecast demand let alone the far more volatile price.

Traders zoomed in on the June 17 contract, the first one due after the Hazelwood close. Normally trading at a discount to the March contract it’s now at a premium and has risen from $40 MWh to $70 a MWh in about six months.

- Spot electricity prices. Were soft this week although still well up on last year.

- REC were as usual unchanged

- Gas prices : remain well up on last year but not much changed on last week.

- Utility share prices: The best news, in our view, this week was the strong performance of Orecobre, a lithium producer, as the market reacted to the excellent price it received for lithium carbonate in its last quarterly. AGL share price also increased, although perhaps the good news of Hazelwood’s closure is still not fully factored in. Redflow was the worst peforming share in the week down 16% although still up 45% on last year.

- Industry news. Well of course its all about Engie and Hazelwood and deserves a forthcoming detailed note of its own.

Share Prices

Volumes

Base Load Futures

Gas Prices

David Leitch is principal of ITK. He was formerly a Utility Analyst for leading investment banks over the past 30 years. The views expressed are his own. Please note our new section, Energy Markets, which will include analysis from Leitch on the energy markets and broader energy issues. And also note our live generation widget, and the APVI solar contribution.