The small-scale solar PV market recovered late in 2016 to post a 1.3% increase on 2015 installed capacity. Solar PV systems equivalent to 723MW were submitted for creation during 2016, compared to 714 MW in 2015.

Capacity installed for residential sized systems (less than 10kW) decreased by four per cent whilst commercial sized systems (10kW to 100kW) increased by 19%.

Commercial sized systems accounted for 26% of installed capacity for 2016 up from 21% in 2015. Interestingly commercial sized systems accounted for 32% of STCs that were submitted for creation in the Month of December (GEM December 2016 Solar Snapshot).

This is symptomatic of a long term trend in the Australian rooftop solar market.

Several years ago Australia’s solar market was quite unique in the world in terms of being dominated by lots of very small household systems below 2 kilowatts in capacity. Meanwhile the market in commercial rooftop systems was almost non-existent.

The market has now changed dramatically.

Large reductions in module prices and changes in government subsidies, as well as the fact that household customers are harder to come by, has encouraged solar retailers to shift towards larger residential systems closer to 5kW in capacity.

In addition, the dramatic reduction in solar system costs and the increasing maturity and sophistication of solar companies has driven growth in sales to larger commercial customers such as major retail chains.

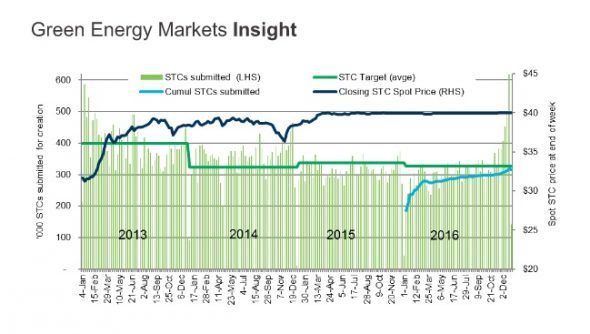

At the beginning of the year Green Energy Markets had projected that 16.25 million STCs would be created over 2016. In the end this forecast was slightly exceeded by 1.4%, with a total of 16.47 million STCs submitted for creation during 2016.

This fell just 3.2% (0.55 million STCs) short of the Clean Energy Regulator’s target for the Small Scale Renewable Energy Scheme of 17.02 million.

Getting so close to the target is a result of the surge in STC creation over the last two months of 2016 (refer to chart below). Half way through the year (30 June) solar installations had been tracking 12 per cent behind target.

The late surge in STC creation can be mainly attributed to:

- More aggressive marketing by solar businesses off the back of the reduction in the level of deeming for solar PV from 15 years to 14 years (“get in before government rebate reduces”). Whilst the impact of the reduction is not that significant on its own (say $270 for a 5 kW system that would cost in excess of $5000), it is used by solar businesses to create some urgency to get customers to sign up.

- Increasing media focus on higher power prices particularly following SA blackout and high priced events as well as the closure of Hazelwood. The focus on higher prices not only improves the economics of PV but also serves to create additional urgency.

- Increase in the number of commercial sized systems

Feedback from a number of industry players indicate that order books are full going into the new year. Whilst we still expect to see some seasonal slowdown over the first quarter, it is not likely to be as severe as experienced in the first quarter of 2016.

Ric Brazzale is director of Green Energy Markets.