The standard of living is the biggest problem facing any government looking for re election. In the US, even the prospect of Trump chaos wasn’t enough to scare off voters, even if it should have been.

In Australia, Anthony Albanese has wasted something he waited his career for. Albanese, like so many, underestimates Dutton and arguably lacks the courage of his convictions. His reported veto of the EPA bill is concerning.

Still, that is none of concern except insofar as it concerns decarbonisation. And my interest is in seeing that the Capacity Investment Scheme is fulfilled, and in my opinion that will be a lot easier if energy minister Chris Bowen remains in charge. This is a job that has to be seen through to the end. It is worth the sacrifice required.

Bowen hasn’t wasted his time. I’ve pointed to the list of achievements previously but for me the success of the 6 GW CIS Tender 1 is an absolute key and would be fundamentally reinforced if Tender 4 can be successfully completed prior to the next election.

However, the latter is a bit doubtful, and the new schedule suggests it won’t be decided until late next year. Between them another 10 GW of wind and solar could be more or less locked in and that would take us to say over 60% renewables within the next 3-4 years. From there to 80% is an easy step.

Even before the new CIS tenders, wind supply is set to grow 44% and utility solar 36%. Between them it’s about 8 GW of new VRE supply under construction and commissioning. Battery supply is growing very dramatically.

The market in a couple of years may be quite different to this year. All this supply is of course totally needed so that coal can be moved out. Equally we still need lots more transmission and more of everything.

Even before those tenders though as the following tables show there is more going on than is realised.

I am indebted to RenewMap as the source of the data used in the following tables.

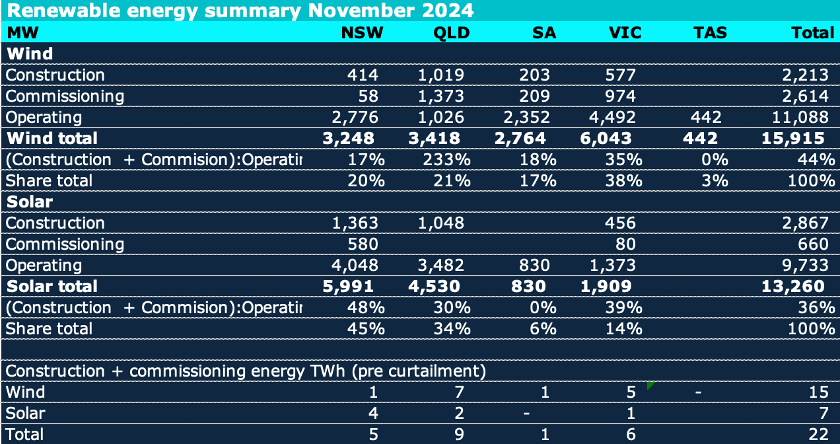

Locked in wind, solar and battery supply

The following figure summarises VRE operating, commissioning and construction.

Figure 1: VRE in the NEM. Source: RenewMap

Thanks largely to Mick Di Brenni in Queensland and the persistence of Westwind in Victoria, wind supply in the NEM will grow 44% for sure. QLD supply will grow 233%.

Of the new wind supply 2.6 GW or more than half is in the commissioning stage with max output from each of Macintyre and and Golden Plains having gone over 50 MW briefly, The 200 MW Ryan Corner could be regarded as fully commissioned and Goyder 1A not far off.

Utility solar supply is set to grow a signifiant 36% largely due to NSW. NSW has need of new supply and even utility solar can mostly get a positive spot price but its still a bit surprising.

Between the wind and solar its something like 22 TWh of new supply or more than 10% of the current NEM wide total.

Regarding the 3.5 GW of utility solar under construction and commission a rough estimate of average daily output if zero curtailment is about 18 GWh. Or, put another way, peak average daily output is about 2.5 GW never mind the extra rooftop solar every year.

So either there will need to be a lot more curtailment or something like 2.5 GW of batteries is required to store it all.

More likely is that some solar will go into storage, some will be curtailed and some will be needed as coal generation units retire. Still this spring’s problems will likely be worse next year and significantly worse the following year. It’s the retirement in short order of Yallourn, Eraring and likely Gladstone that we are working towards.

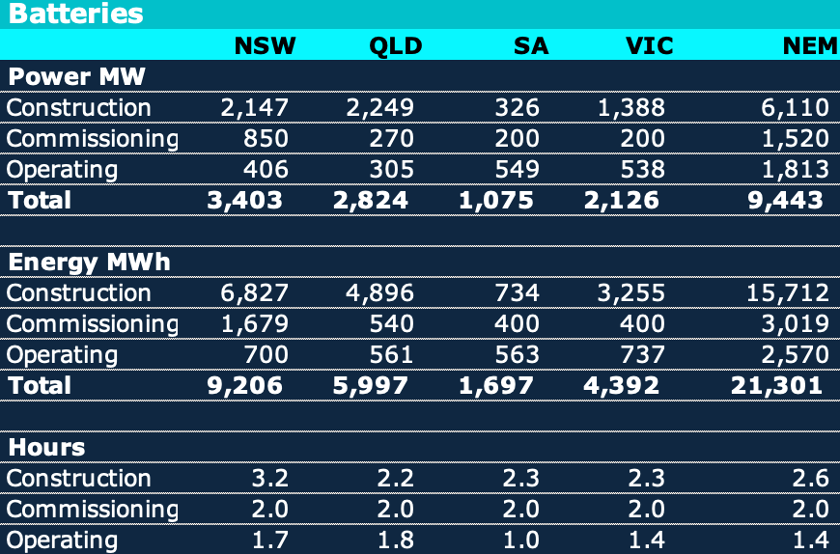

Turning to storage, the fantastic growth is living proof that price signals work. The prospect of being paid to charge at lunchtime, a seemingly endless growth of new lunchtime supply from rooftop solar has lead to developer after developer taking the investment plunge.

Figure 2: Batteries in the NEM. Source: RenewMap

And it’s not just an exciting 7.6 GW of power (rivalling the growth in even Texas) but the even more exciting 18.7 GWh of energy. So that 18.7 GWh actually marries up closely with the new utility solar but its rooftop that will still lead to an imbalance. More household storage would fix that and is the missing Federal policy initiative.