As far back as 1981 a proposal for an international agency dedicated towards renewable energy was made at a UN conference in Nairobi. It took until 2009 for the founding conference to be held and in 2011 the International Renewable Energy Agency was born.

IRENA now has 147 members and serves “as a platform for international co-operation, a centre for excellence, and a repository of policy, technology, resource and financial knowledge on renewable energy. Australia is a member as is most of Europe, the USA and much of Asia. Canada is not a member.

IRENA’s HQ is in Masdar City, in the UAE. It has about 90 people and a 2016 budget of US$30.4 m plus it expects/hopes to “mobilise” additional voluntary resources for US$15 m. Australia pays US$0.5 m.

It’s virtually impossible for someone who has worked as a stockbroking analyst for more than 30 years to not go poking into the budget and equally impossible to totally suspend cynicism about the value for money and overheads of any global organisation.

IRENA does provide its budget and work program in some detail on a two year basis and we have converted to annual numbers in the table. The work under the voluntary resources project depends on the resources being available. Tasmania arguably could have taken some of the “Islands: lighthouses for renewable energy” information on board and avoided some of its recent issues.

What we get is some useful information.

IRENA’s web site provides some useful summaries of the state of the renewable energy in an effective online, graphical database that can be accessed here.

The data can be seen and analysed on screen and download either to excel, as a .pdf or as an image. In short its an excellent example of a user friendly, data rich, graphical website.

So it’s nice to see we are getting something for the money. In fact as the budget above shows IRENA does a lot more than simply provide installed capacity statistics.

A couple of images from the site are shown:

Ignoring hydro, but leaving in pumped storage, the world has about 0.9 TW (900,000 MW) of renewable energy capacity and this has basically doubled since 2010. Wind remains the dominant technology although “solid biomass” has a larger than expected share.

A new global record of 110GW of annual installations was reached in 2015. New wind installations continued to exceed new solar though many expect that may reverse as the solar technology has more development potential and in addition is disruptive by virtue of its distributed nature.

Geography

If we look at wind by country, the dominance of China is clear, followed by the USA. It’s a cause of some amusement to the author that there must be overt 50,000 wind turbines in the USA and maybe over 0.5 mn “fracked” shale wells.

If either technology had any significant health or environmental impacts we’d have expected it to show up by now.

China also leads the world in installed solar PV and the lead in both segments can be expected to continue grow over the next few years.

The broader context

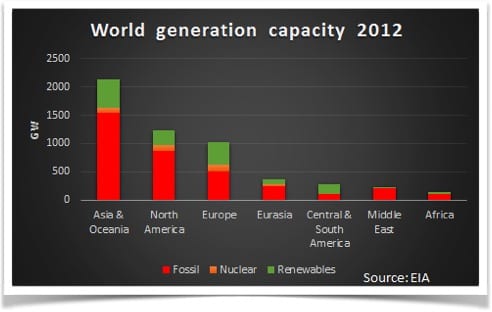

At the moment renewables still has a long way to go. There is a bit over 5.5 TW of global installed generation capacity and as of 2012, 3.6 TW or 66% of that was fossil fuel.

So at a rate of 110 GW of new global renewables and very implausibly assuming no growth in electricity demand, allowing for the higher capacity factor of thermal it would take 40 years or more to replace the thermal with renewables.

Thus the chart below provides a good lead in to part 3 of our “Thinking global” series where its time to look at coal fired electricity in general and in China in particular. In the chart below renewables includes hydro and we ignore pumped storage.

This is the second in a series of thinking global series on climate change and energy. The first can be accessed here.

David Leitch was a Utility Analyst for leading investment banks over the past 30 years. The views expressed are his own. Please note our new section, Energy Markets, which will include analysis from Leitch on the energy markets and broader energy issues. And also note our live generation widget, and the APVI solar contribution.