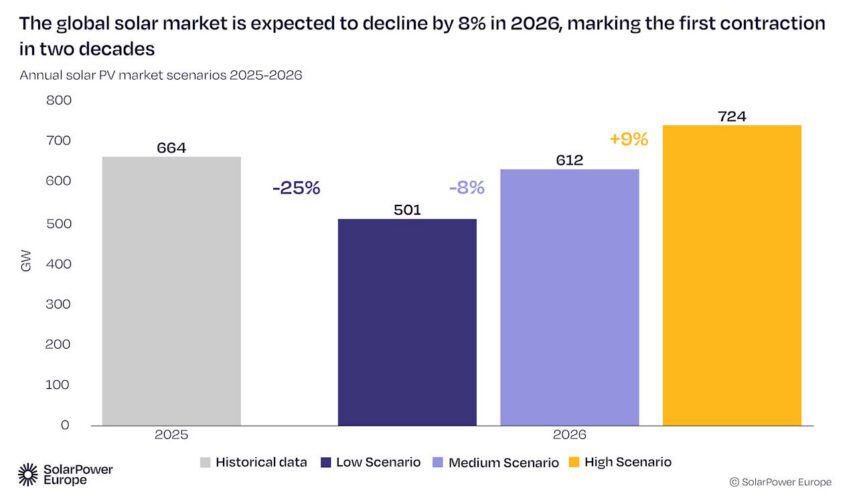

A record 664 gigawatts (GW) of new solar PV capacity was installed across the world in 2025, helping to take the total solar fleet across the 3 terawatts(TW) mark in early 2026, tripling global capacity in just four years.

The new Global Solar Market Outlook 2026-2030, published this week by SolarPower Europe, says the 2025 capacity installation of 554 represented an increase of 69 GW compared with 2024, and 212 GW compared with 2023.

Solar PV accounted for 77 per cent of all new renewable capacity additions recorded in 2025, and finished the year by generating 2,778 terawatt-hours (TWh) – around 9 per cent of global demand.

However, the rate of growth is slowing, from 85 per cent in 2023 to 32 per cent in 2024 and 12 per cent in 2025, and SolarPower Europe also expects a temporary decline in overall installations in 2026, before growth resumes in 2027.

“The solar age is firmly established,” said Walburga Hemetsberger, CEO of SolarPower Europe. “With another record year in capacity additions in 2025, solar continues to outperform all other energy technologies.

“However, the slowdown in growth we observed in 2025 and the expected dip in 2026 are important signals highlighting a new reality: scaling solar is no longer just about deploying more capacity but about how well it can be integrated into the system.”

The global solar market remains concentrated in a handful of countries, led of course by China, which installed 382GW in 2025, accounting for 57 per cent of all global installations.

India stepped into place as the world’s second-largest solar market, installing 45.7 GW, beating out the United States which slipped to third as well as slipping in total capacity additions, reaching only 43.2 GW, down from 50 GW added in 2024.

It is partly China’s ongoing dominance which will lead to the first contraction in the solar market in over 20 years, where domestic policy changes are expected to see their annual capacity installations drop by 24 per cent.

As a result, global solar installations are expected to decline by 8 per cent in 2026 to 612GW in SolarPower Europe’s “Medium Scenario”.

The dip in annual capacity additions is expected to be temporary, though, with growth returning in 2027 on the way to reaching an annual market of 864GW in 2030.

“Despite the expected dip in 2026, the long-term outlook for solar remains robust,” said Markus Elsässer, CEO of Solar Promotion GmbH.

“Annual installations are projected to reach around 864 GW by 2030, while total global capacity is expected to grow to 6.6 TW, with upward potential to 7.6 GW in the High scenario.

“Solar will continue to be the main pillar of the energy transition, also in the short-term delivering around 60% of the renewable capacity needed to meet global 2030 targets.”

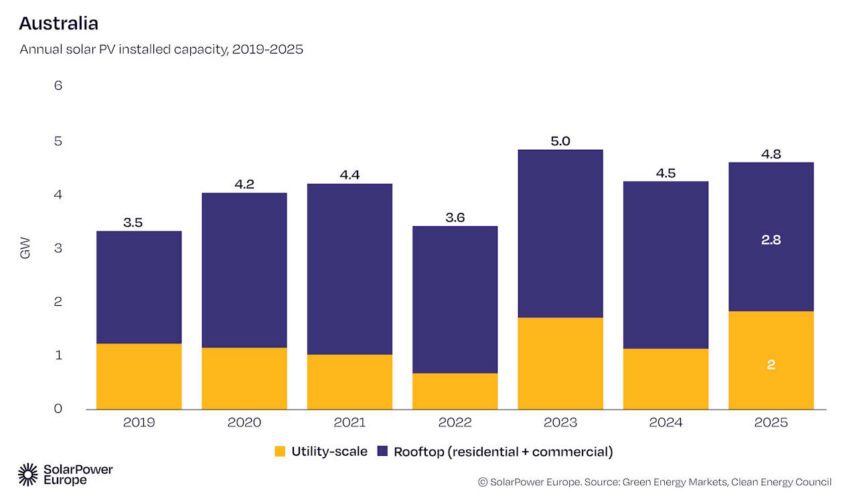

The report also carved out a sizeable chunk to highlight the role that solar PV plays in Australia, where solar capacity surpassed 45GW at the end of 2025 – up from only 5.1GW at the end of 2015.

Australia’s solar capacity remains predominantly rooftop based. For example, in 2025, around 2.8 GW of the 4.8 GW of new solar installed came from rooftop residential, commercial, and industrial systems.

The dominance of rooftop solar in Australia’s energy mix is due in large part to long-standing consumer incentives and strong political support.

However, this rooftop solar dominance also highlights the need for utility-scale solar to accelerate if Australia is to reach its 2030 target of reducing greenhouse gas emissions by 43 per cent compared to 2005 levels, and pushing the renewable energy share to 82 per cent.

If you would like to join more than 29,000 others and get the latest clean energy news delivered straight to your inbox, for free, please click here to subscribe to our free daily newsletter.