There’s a particular kind of irony building in Whyalla. The man now potentially in line to transform the troubled South Australia steelworks has just acquired the most methane-intensive coal portfolio in New South Wales. The question now remains, could this coal baron become Australia’s best hope to tackle its methane emissions?

According to reporting from the AFR, Matt Latimore’s M Resources and India’s Jindal Steel are now the last two bidders standing for the Whyalla steelworks and its Middleback Ranges iron ore mines.

While BlueScope still holds a right of last offer, it’s board is busy fending its third take-over offer this year, and South Australia Premier Peter Malinauskas has suggested that either the Indian steel major or a metallurgical coal trader could now give Whyalla “the best chance to realise the end game.”

For Jindal Steel, its experience developing low-emissions iron and steel facilities in Oman and India could indeed be a boon for Whyalla. For Latimore, that end-game pitch includes a potentially innovative approach to methane pyrolysis to create what might be called, “teal steel” instead.

If successful, Latimore & co. will not only be responsible for managing the steelworks, but its more than a million tonnes of CO2 emissions each year.

When combined with the newly expanded portfolio of coal mines, GM3 – a partnership between Golden Energy and Resources (GEAR) and M Resources – could soon be responsible for one of the largest greenhouse gas emissions portfolios in the country, comparable with a company like Shell.

It could also become our best hope of tackling industrial and fugitive emissions over the next few years.

The coal mine methane challenge

While Latimore is actively pursuing the Whyalla opportunity, his GM3 joint venture also recently acquired a different stranded Gupta asset, the Tahmoor colliery.

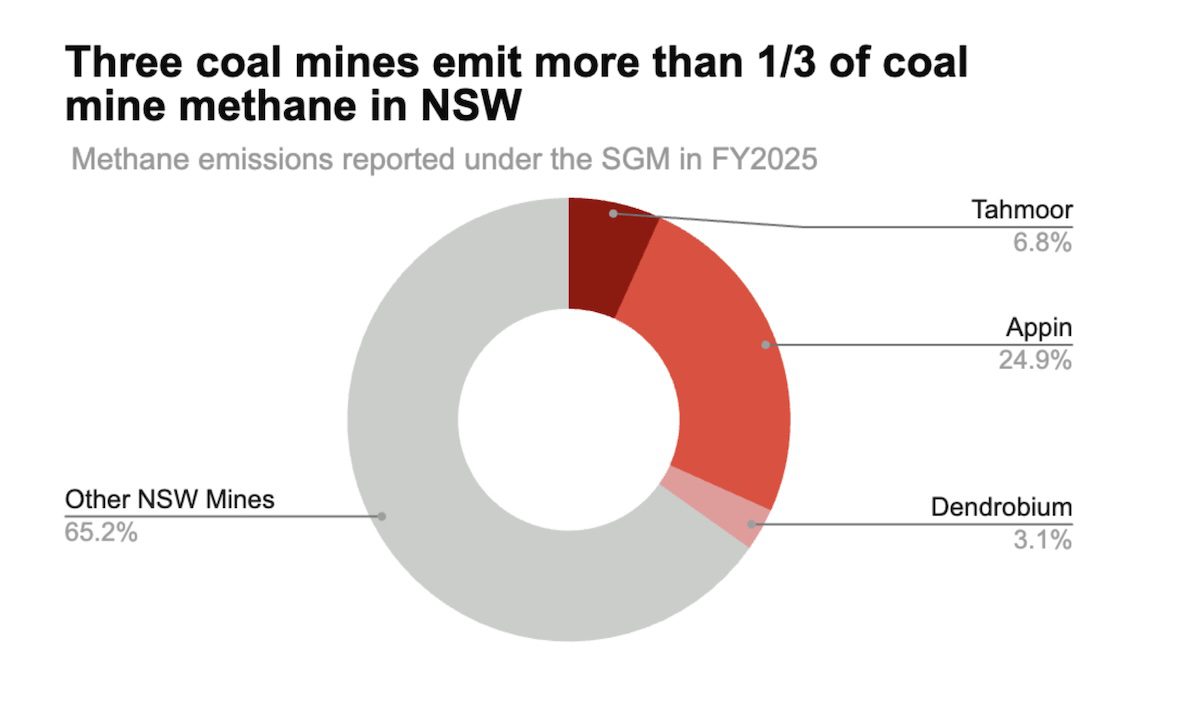

The underground mine is just up the hill from his 2024 purchases of the Appin and Dendrobium coal mines. Together, the suite makes up three of the most critical metallurgical coal mines in NSW, and collectively mine some of the gasiest coal seams in the country.

When Sanjeev Gupta previously acquired the Tahmoor coal mine in 2018, he did so hoping to create a fully-integrated Australian steel empire that would directly input into the Whyalla steelworks. Interestingly, Latimore is now reassembling a very similar jigsaw puzzle, from the wreckage of Gupta’s collapse.

Across the three mines, M Resources now carries a combined climate footprint of around 3.6 million tonnes of CO2-equivalent per year. However, once production resumes at Tahmoor, the portfolio is likely to push past 4 million tonnes of CO2-e annually.

Together, the three mines also make up a significant share of the state’s coal mine methane emissions. Last year, the three mines collectively emitted 112,000 tonnes of methane. This may not sound like a lot, but it represents more than a third of the state’s total coal mine methane emissions, while only accounting for less than 3% of its coal output. Going forward, that share could easily increase in the coming years.

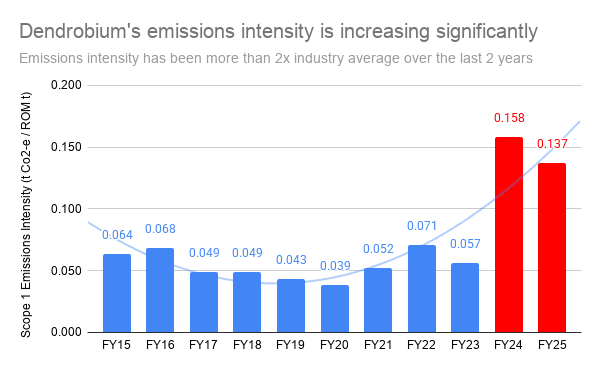

The Appin mine saw its methane emissions increase by 30% last year alone, while Dendrobium, the smallest emitter of the three, has seen its greenhouse emissions more than double since 2022. Once Tahmoor colliery comes fully online in the next few months, we should expect its emissions to increase, too.

A new regulatory landscape

These fugitive methane emissions have been the focus of a year-long Parliamentary inquiry, a series of EPA reforms, and a Spotlight report from the NSW Net Zero Comission. However, tackling these emissions requires not only policy scrutiny and safety reviews, but a transformational shift in how coal mine owners and operators understand their commercial and social responsibilities.

After years of consultation, the NSW EPA confirmed in March that it was now seeking to transform the regulatory landscape for high-emitting underground coal mines. The highest emitting underground mines now face new obligations to seal methane leaks, engage in pre-mine drainage, and to actively abate ventilation air methane in the 2030’s.

These regulatory changes fundamentally shift the operating landscapes for these mines. When combined with increasingly challenging Safeguard requirements, it should provide the positive incentives needed to invest, and address onsite methane emissions for existing and ongoing operations.

Appin is already moving. Tahmoor could too

To its credit, the Appin coal mine is already getting on with its ventilation air methane demonstration plant, with commissioning targeted for Q4 2026. While it will only abate a small fraction of the mine’s annual emissions, it will act as a critical pilot site for both operators and the state’s regulators to learn from.

Interestingly, the Tahmoor coal mine could also go down a similar path, as the regenerative thermal oxidiser technology needed to mitigate its fugitive emissions has been deemed feasible at the colliery since at least 2021. In fact, Tahmoor’s own consultants estimated that on site mitigation could reduce fugitive methane emissions by at least 79%.

While there are still technical hurdles to overcome, GM3 could potentially be sitting on a transformational opportunity for the industry.

What about “teal steel?”

Here’s where the story gets genuinely unusual, especially for a coal baron. Back in Whyalla, Latimore’s M Resources also has pitched an innovative approach to steel production that similarly centres on methane.

Through a binding deal with ASX-listed Hazer Group and engineering giant KBR, the consortium hopes to deploy methane pyrolysis at the Whyalla steelworks.

The process works by splitting methane gas molecules into hydrogen and solid graphite. The hydrogen would then be used as a feedstock in a future direct reduction ironmaking process at a transformed Whyalla steelworks.

This is what the hydrogen industry calls “turquoise hydrogen.” It’s not “green,” as it doesn’t run on renewable energy, but it does transform the methane into hydrogen and graphite, with a much lower greenhouse gas emissions intensity than simply feeding methane gas into a DRI facility.

As such, it could perhaps represent an opportunity to transform the 10-year gas supply agreement recently signed by Santos, into a low-emissions play to produce what could be called, “teal steel.”

The final twist

While Bluescope has the right of final offer at Whyalla, GM3’s competing bid and its coal portfolio presents a genuinely intriguing tussle. Appin, Dendrobium and Tahmoor are also critical suppliers to Bluescope’s Port Kembla’s steel facilities. Previously, Bluescope held pre-emption rights to buy Appin and Dendrobium, as well, but didn’t go ahead. Now, it holds the same rights of last offer on Whyalla.

If Latimore wins the Whyalla bid, he not only remains a critical coal supplier for Bluescope, but potentially a major rival in the Australian steelmaking sector.

However, the way I’d like to put it, is that if he pulls both off, he’d be responsible for not only transforming the Whyalla steelworks, but be in the prime position to tackle coal mine methane emissions as well.