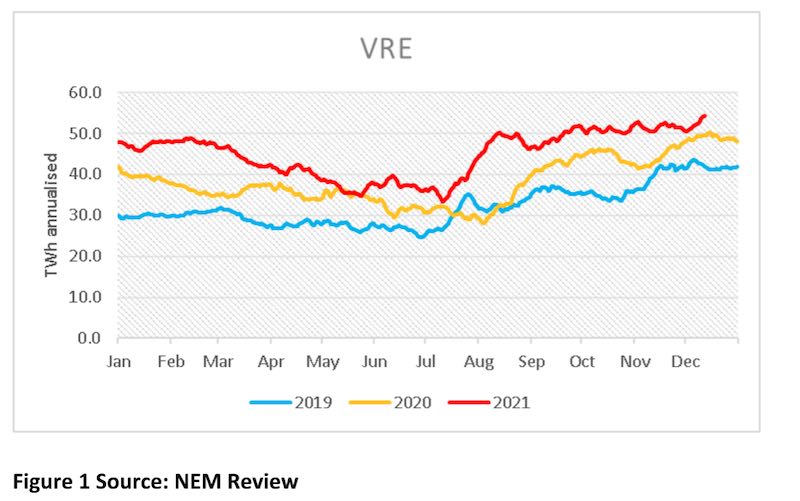

Wind and solar production has run at an annual rate of 54 terrawatt hours (TWh) over the past 30 days (about 28% of demand), which is a new record for the National Electricity Market, although only marginally above where it’s been for a couple of months.

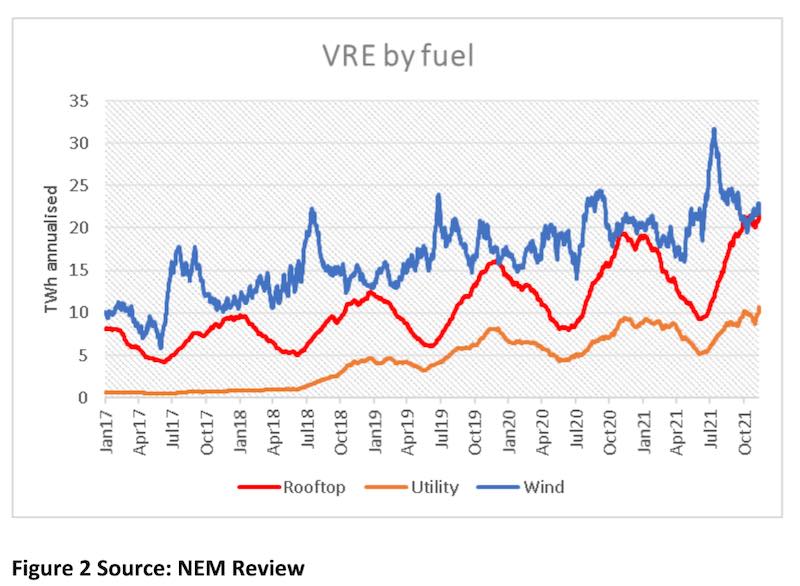

All three segments of variable renewable energy (VRE) – wind, utility solar and rooftop solar – are up on the previous corresponding period, but it’s rooftop solar that really catches the eye, currently running neck and neck with wind at an annualised 22TWh.

As regular readers will know, one of ITK’s big themes is that we are going to move from peak prices in early Summer to peak prices in mid-Winter. There are two main reasons for this.

First – and you can see it in the above figure – the increasing size of solar means that it’s seasonality becomes a bigger driver every year. Recasting solar in GW there is already a greater than 2GW gap between Summer and Winter.

But the second thing is that solar production will in general be reasonably reliable even on very hot sunny days when thermal and wind generation struggle and demand is high.

That, in turn, confers two benefits to the system. Firstly, it means resilience to individual thermal plant breakdowns and, secondly, it reduces the strain on thermal plants in the middle of the day, leaving them more capable of doing the business as the sun drops off.

Of course, all that’s only for the next few years, until storage picks up the thermal load. But during that time it matters.

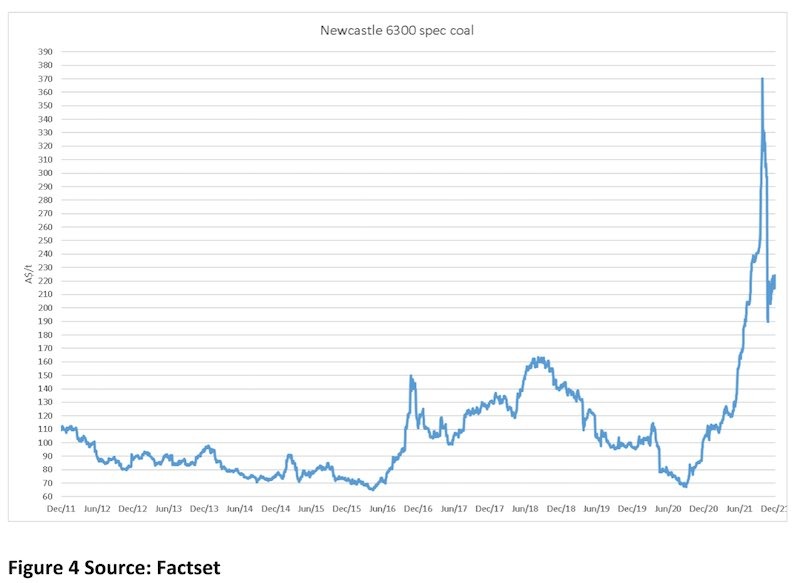

Futures prices have drifted up as gas and coal remain elevated

Although not mentioned in the ISP 2022 draft, you can bet your bottom dollar that if thermal coal prices stay at current levels, which they won’t, Eraring and Vales Point will close early.

Origin is still negotiating new short-term coal contracts to supply Eraring, but the truth is that it’s not a great time to be doing it. Sure, $A220/t for top spec is better than than $370, but it still works to a fuel cost of, say, $A70/MWh at spot:

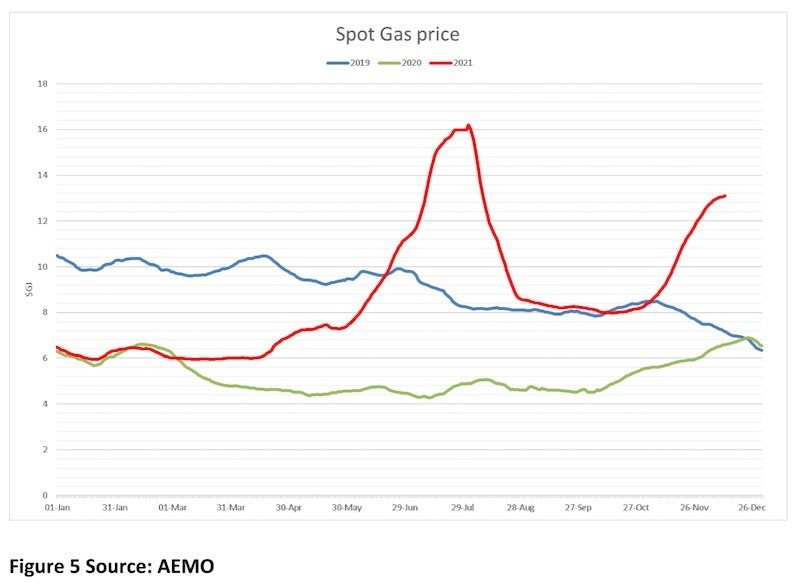

And gas prices seem to have got a second wind.

So it’s just as well not too much gas generation is needed. All this means that the market thinks prices will be flattish for the next few years, but by and large the bigger a state’s VRE share, the lower the price outlook is:

Of course the other reason for Victorian and South Australian prices being lower than their northern neighbours’ is because of constrained transmission between Victoria and NSW, and indeed between Queensland and NSW.

Still, the Vic-NSW constraint is super bad for NSW consumers, but it’s also a real problem for Victorian producers, particularly Brown coal guys.

Victorian, and for that matter South Australian, generators are consistently getting, say, $40/MWh less than NSW but transmission constraints don’t let the power flow north the way it should.

We don’t exactly know what is driving all the transmission constraints, but we do know that northwards flow is way less than even the historic average, let alone what AEMO shows as capacity. We suspect three factors:

1. Constraints in North West Victoria to deal with the “rhombus of regret.” These come into play because some Vic to NSW power want to flow the long way round and AEMO’s dispatch engine dealing with that has some issues;

2. There are constraints on the NSW side, dealing with upgrade/early works for Hume link, etc;

3. Snowy sits in the middle.

Alleviating constraints isn’t cheep cheep so to speak

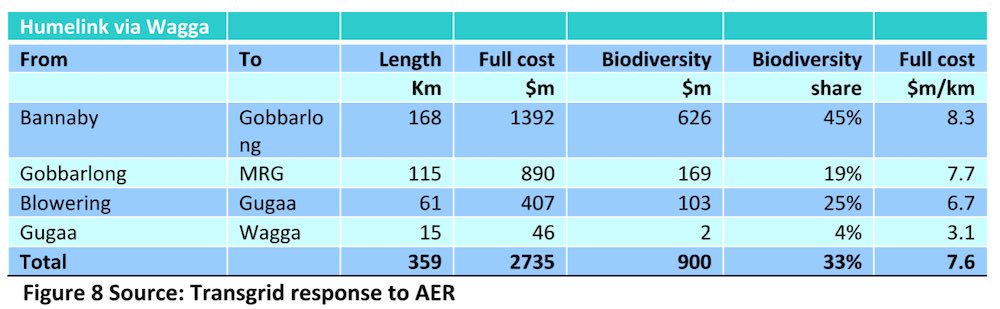

Recently, most of us following the sector had to have a BEX and a good lie down when the AER sent the Humelink transmission proposal back to Transgrid to do some more costing. Can’t have enough analysis.

What caused me to take an extra BEX was looking at the Humelink Biodiversity costs. I can barely spell biodiversity and it hasn’t been a big factor in my limited modelling. Yet for Snowy Mountains sections of transmission it’s virtually half the cost and $900 million in total.

The level of biodiversity costs is certainly high, but I am sure the reason for that is that there are lots of environmental issues. In some ways, the higher the level of costs, the greater the underlying concern we all have to have.

On the other side there are competition benefits going through Wagga which one would not underestimate.

Social license is vital, but it doesn’t come cost free

Social license and the ISP is a massive issue.

Whether Snowy should have to pay, as generators in the NSW REZ will have to for their transmission access, is an interesting but ultimately useless argument for the anti-Snowy 2 brigade because, even if it did have to pay, Snowy would just get another handout from the federal government.

Social license extends so far beyond transmission though, it also goes to wind and solar farm acceptance, pumped hydro development in National parks and who controls behind the meter. A separate note and a long discussion for sure.

In the end, though, you can’t buy social licence, but you can ensure that licences are paid for. Or at least you could if there was a federal government that was actually interested in doing a good job.