What’s interesting this week – South Australia firming

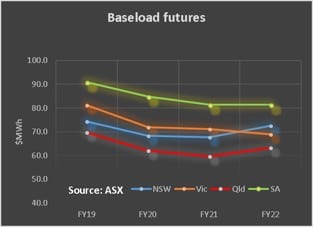

South Australia remains interesting. South Australia’s base load futures are higher than those of other States and show no sign of moving, or trading.

They don’t trade much because, let’s be clear, AGL has lots of influence in South Australian electricity. Its investment in the State is minimal, less than $200 m for the retail business back when it was loss making and maybe another $100 m cash as the price net of the 150 MW station in Victoria for TIPS in 2007, but it has paid off.

I think it’s reasonably well understood that baseload prices are high in South Australia because either gas or imports from Victoria set the price most of the time. Wind is a price taker, gas is a price setter. (Ed: I’d add lack of competition).

Well over 1GW of project talk, but only Barker Inlet committed

As usual, entrepreneurs of all flavours see the high prices in South Australia as an opportunity.

First off the rank was the Hornsdale battery, but, as expected, this has of course done nothing to average wholesale prices. That’s not its job.

However, several new projects will have some battery storage. Individually they may not make a difference but in aggregate they could take the edge off arbitrage pricing.

Second is 210 MW, $245 m, 210 MW gas fuelled reciprocating engine Barker Inlet power station. This plant could do a lot to influence power prices, but because its owned by AGL, it’s likely to be used quite strategically.

We expect this plant on its own to improve AGL’s profitability but not to have much impact on price. Its flexibility might influence AEMO decisions about how much reserve gas needs to be operating in the State.

Next up we have firmed renewable options. These include 4 pumped hydro proposals totaling 745 MW and 5.6 GWh of storage.

Obviously, not all of these will go ahead. Delta’s Goat Hill has arguably the best economics, low environment impact, simplest technology, and is the most advanced of the projects.

But Delta has no real presence in South Australia. So it could perhaps sell the project if someone made it the right offer.

Pumped Hydro needs somewhere between $70-$90MWh difference between buy and sell price.

One problem in South Australia, is that if gas is required for backup and is setting the price, it may be harder to get the daily arbitrage potential that the wind and PV alone naturally provides.

Next there is the SolarReserve, Aurora concentrating solar project, 150 MW, 1100 MWh plant. The plant may go ahead despite its technology risk thanks to strong Government support.

If it does work it will take some of the market that might otherwise have been available to say one of the pumped hydro projects.

Then we have LNG import plans. These have been driven by the mining industry, but particularly BHP. BHP’s Olympic Dam project was hurt by South Austalia’s blackouts.

According to Matthew Stevens in the AFR, Olympic Dam was within 10 minutes of molten metal freezing in its smelter requiring a $3 bn rebuild.

As a result there are two proposals to put floating LNG off the coast near Pelican Point and the gas sold to a new gas fired power station of, according to the AFR, 750 MW.

ITK estimates that the capital investment would be closer to $2 bn than $1.5 bn. Olympic Dam though only uses 125 MW or around 7% of South Australia consumption.

You can’t base $2 bn of capex on that.

Nor on some long mooted but never committed potential Olympic Dam extension.

Unlike NSW there is an arbitrage opportunity in South Australia

Repeating the same exercise for South Australia as for NSW that we recently did, we downloaded half hourly prices over the past 12 months, sorted these into a 365 x 48 table of daily half hourly prices and then sorted the days from low price to high price.

We see that for 4 hours storage a comfortable margin of $119 MWh could be had on average but this was influenced by a few high price events and the median returns were materially lower. 6 hour median return were not that different to NSW.

So many projects but no commitment except from AGL

Only the Barkers Inlet 210 MW is committed. AGL’s market power gives them the confidence to make that commitment.

We’ve written about the SolarReserve project before. In our view the publicly available evidence suggests there is still some technology risk. But because of Federal and State backing it may still go ahead.

So far none of the Pumped Hydro projects are committed. The usual obstacles remain in an energy market to going merchant. What will the other players do?

If there is an arbitrage return in South Australia for one plant there may not be enough for two plants. The usual way around this is via some capacity contract.

South Australia though is a special case where there is no one much to contract with. No one wants to contract with AGL because AGL will get by far the better end of the bargain.

This really only leaves, individual corporate PPAs such as the Gupta steel works and Olympic Dam. These too are difficult contracts.

The South Australian Govt took itself out of the picture by awarding its contract to SolarReserve. We think, with the benefit of hindsight, this was a risky decision, but it’s done now.

The market action

There was a brief price spike in South Australia and Victoria for half an hour but weekly average spot prices were broadly in the low $70s MWh across the NEM.

Consumption was essentially seasonally normal and broadly unchanged from the past couple of years.

Out year REC prices continued to dive, and we expect renewable developers to have to seek alternative revenue under the NEG in that period. Gas prices were lower than last year but the gap is if anything narrowing a fraction.

Oil prices strengthened and if maintained this will drive up the gas price in Australia as LNG exports will have a greater incentive to export.

More importantly perhaps, US 10 year treasuries have fallen back below 3% and various investment banks are once again re evaluating global prospects.

Leaving aside USA growth and inflation the other key variable in the world economy is always China’s housing growth.

China builds about 15 m houses a year, 20 m in some years and this produces a massive demand for steel, cement, plastics, electricity and subdivisional roads, notwithstanding that the buildings are high rise and small.

The residential demand in China produces corresponding commercial property demand. At the moment residential floor space starts are showing a 12% growth rate and this essentially will prop up the Chinese economy pretty much all by itself.

SHARE PRICES

20% of Tilt Energy changes hands. This morning Mercury Energy, a $4bn listed NZ gentailer, 51% owned by the NZ Govt announced it had purchased 19.9% (just below the takeover threshold) from a NZ electricity consumer trust.

Investors will wonder if this is a prelude to Mercury seeking to control Tilt. It’s a national sport for New Zealand companies to venture to Australia, Powershop is already active, and can Contact be far behind?

Tilt may look to accelerate its investment plans here. There is not much point on Mecury sitting on 20% of Tilt as a passive shareholder.

Base load futures, $MWH

Figure 12: Baseload futures financial year time weighted average

Gas prices

David Leitch is principal of ITK. He was formerly a Utility Analyst for leading investment banks over the past 30 years. The views expressed are his own. Please note our new section, Energy Markets, which will include analysis from Leitch on the energy markets and broader energy issues. And also note our live generation widget, and the APVI solar contribution.