Battery-based energy storage can play a valuable enabling role when it comes to renewable energy adoption, but storage can also do much more. Services such as peak shifting, backup power, and ancillary grid services are a small subset of the larger matrix of potential future values batteries can provide, but storage is still too expensive to cost-effectively provide these services in most U.S. markets.

However, energy storage may be reaching a tipping point. Analysts at GTM project that 318 MW of distributed solar plus storage may be installed by 2018, for example. Also, California’s mandate to procure 1.3 GW of storage, combined with the Tesla gigafactory and the general trend of moving towards prosumer-based electricity markets, is a testament to the size of the potential market.

Thanks to these projections and no shortage of media coverage (by our count, over forty energy storage articles have been released over the past two months alone), an outsider could be led to believe that distributed storage, by participating in several different kinds of electricity markets using a number of different product configurations, is capable of solving many of our electricity system ills.

However, we’re not quite there yet. In reality the current state of the industry in the U.S. is still simple enough that it can be captured in a single chart that illustrates the two major challenges the energy storage industry is currently facing: high costs and limited avenues for capturing value.

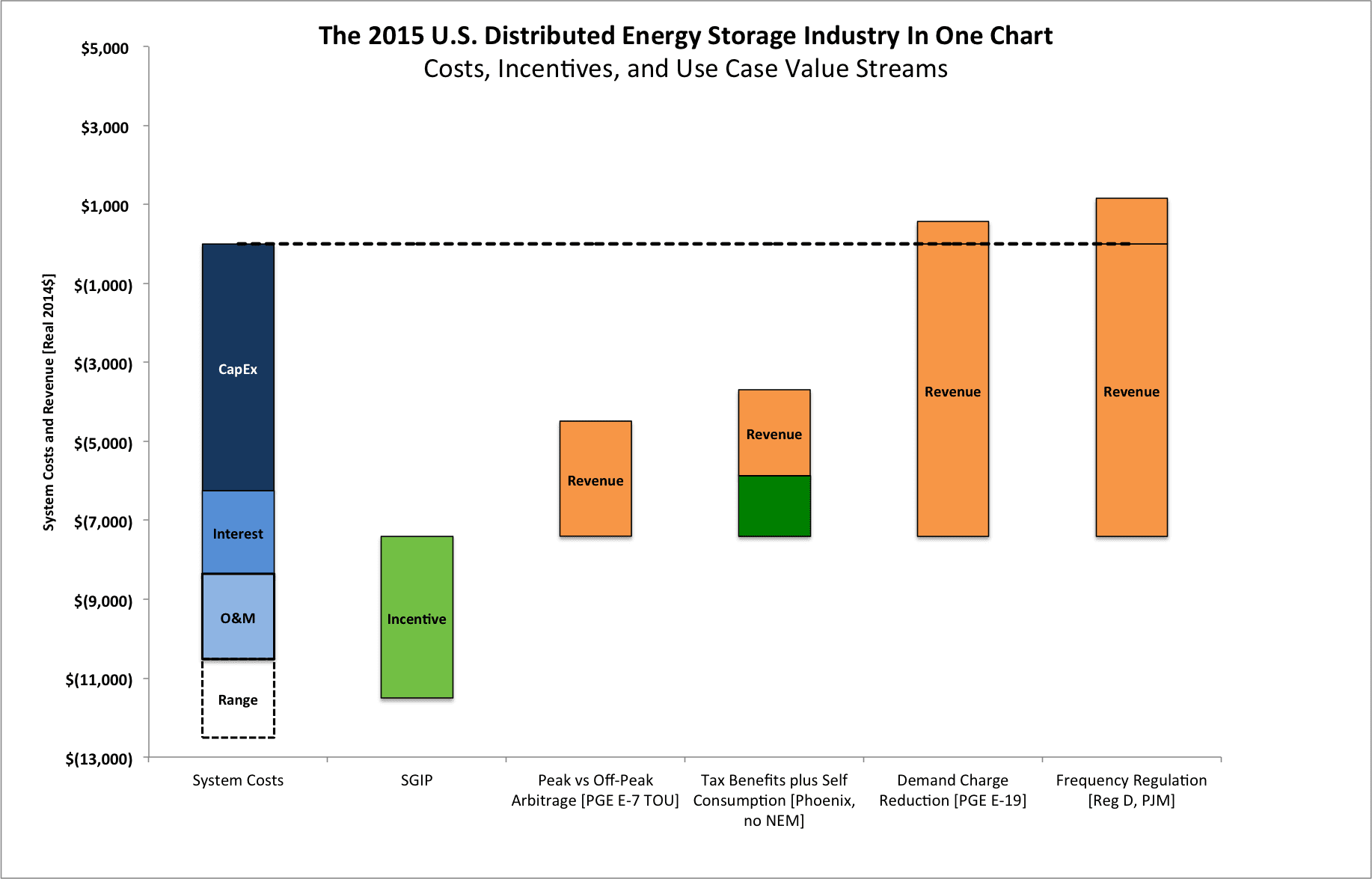

In the following figure we’ve illustrated:

- Installed cost for an energy storage system (blue bars on the left) based on current system pricing and a 20-year system lifetime

- How much money you can make using that energy storage system for the four primary use cases we see right now.

Expanding Storage’s Net Value

Any orange bar that climbs above the dotted black line indicates a profitable business case under current cost and rate structures. For any orange bar below the dotted black line, it’s currently not profitable to pursue that business case. For anyone following the energy storage industry, this makes intuitive sense: the frequency regulation market in PJM territory and the demand charge reduction market for commercial customers in California both currently offer cash-positive scenarios for energy storage companies like STEM and Coda. But other opportunities, such as self-consumption in Arizona and rate arbitrage in California, current have system costs that are too high and use case revenues that are too low to deliver a compelling value proposition.

But here’s the reason this chart explains the state of the entire U.S. energy storage industry: if you remove the green subsidy bar (here we use California’s Self-Generation Incentive Program (SGIP) and pretend it can be used in different states for various use cases) or move beyond regions with extremely generous compensation mechanisms (such as the PJM frequency market), none of these current business models offer anything close to a cash-positive scenario. This means that energy storage is either too expensive for widespread application or the revenue opportunities for energy storage simply aren’t big enough for the technology to capture value right now.

Following closely on the heels of Rocky Mountain Institute’s Battery Balance of System Charrette, our team is now working to attack both the cost and value sides of this equation in order for that blue bar to get a lot smaller and for more and more of those orange bars (and we’d like to see many more of these, not just the four dominant ones we see today) to climb well over the dotted black line in new markets across the U.S.

Decreasing Costs

Right now, you can spend $29,000 (or $21,500 after incentives) for a 24 kilowatt-hour lithium ion battery pack … and you also get a car, since Li-ion batteries at those prices and sizes are found in today’s electric vehicles (e.g., the Nissan LEAF). Alternatively, you can spend nearly $34,000 for a similar battery pack without wheels. It could also take over 100 days for the utility to green-light you to use that wheel-less battery pack and your local jurisdiction might require a water-based fire extinguishing system to be installed (even if all that will do is fry your entire battery system).

During the charrette, we identified a host of similar, “easy to solve” challenges that could reduce costs as well as an array of more fundamental challenges, including:

- the lack of standardization in a variety of key elements,

- boutique interconnection protocols (how a battery is connected to the grid, and what it is allowed to do), and

- lack of interoperability with other systems (how multiple batteries talk to each other, and how batteries talk to other things, like your solar system or home energy management system).

To help overcome these challenges and reduce the cost and time to market for energy storage systems, RMI is taking the lead on developing an energy storage cost roadmap framework in order to help industry, utilities, and customers understand how much storage costs now, outline what an industry-wide “should cost” target looks like (analogous to similar targets in the PV, solar system, and semiconductor industries), and map the various initiatives and research that will need to take place in order to reach the cost targets. Furthermore, we’re taking a hard look at the EV industry’s effort to develop a standard EV plug to better understand how the energy storage industry could develop similar standardized physical interfaces for their products at the building and product levels.

Creating More and Larger Value Streams

Solving one side of the energy storage equation—reducing costs—won’t automatically lead to the creation of a thriving energy storage ecosystem. In addition, our electricity system needs to evolve and allow energy storage systems to compete with other energy resources on a level playing field. Unlike a residential solar PV customer, energy storage customers of all shapes and sizes are compensated differently depending on the market they participate in—if they’re even compensated at all. This, in spite of the fact that energy storage can or will be able to provide various grid services to millions of customers at a lower cost of service than today.

To help incubate a thriving energy storage ecosystem in the U.S. and more broadly, RMI is exploring partnership opportunities with regulators, utilities, and energy storage companies to fully understand the costs and benefits of energy storage (analogous to the effort RMI embarked upon two years ago with our similar study on distributed PV). Over the next year, we hope to help utilities better understand how distributed energy storage can reduce costs on distribution systems in order to drive regulatory change and open up entire new markets for distributed storage.

Cost-effective distributed energy storage is capable of helping electricity systems transform into low-carbon, secure, and reliable backbones of communities large and small. By focusing on the cost and value sides of the energy storage industry, we hope to help this technology reach unprecedented scale and contribute to RMI’s vision of the electricity future. We encourage you to check in on RMI’s efforts in the energy storage space here on our blog and feel free to let us know what you think in the comments below.

This article was originally published on the Rocky Mountain Institute’s Outlet blog. Republished here with permission.