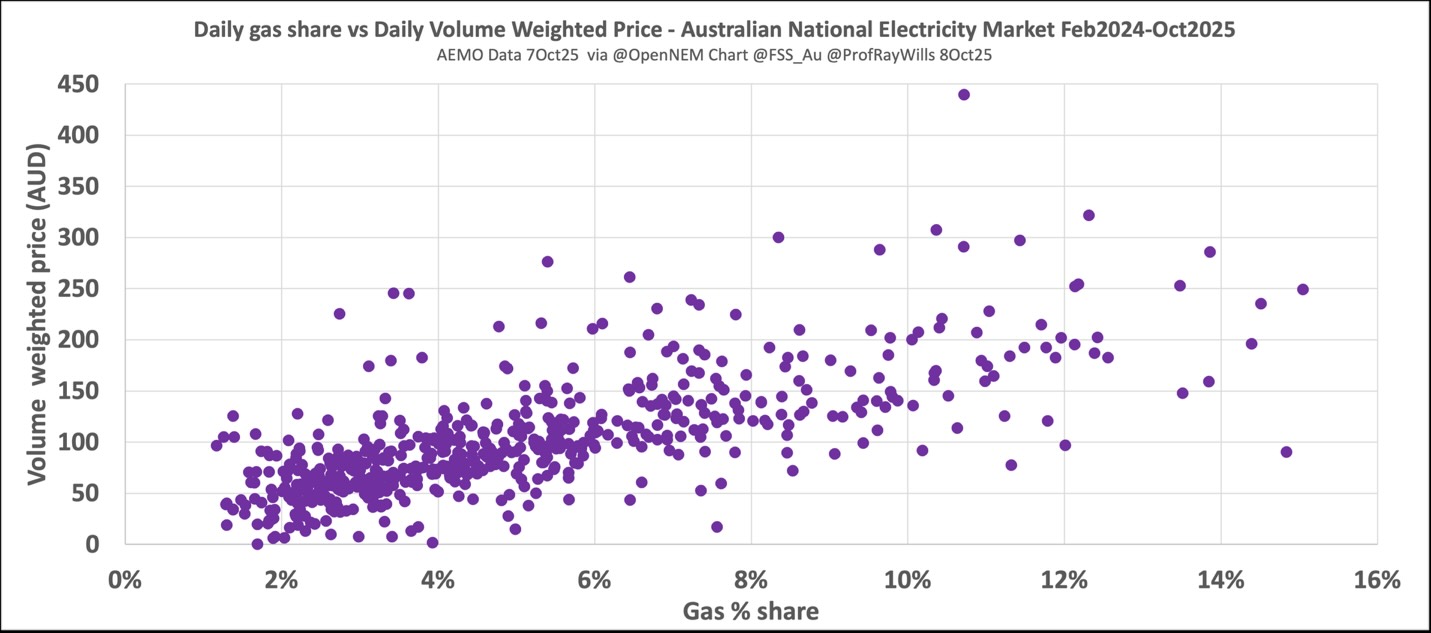

Analysis of National Electricity Market (NEM) price data reveals a strong relationship between the share of gas and coal generation and wholesale electricity prices.

When gas-fired generation exceeds 6% of the supply mix, nearly all volume-weighted prices (VWP) rise above $100 per megawatt-hour (MWh). Once the gas share passes 10%, the VWP typically approaches or surpasses $150/MWh.

Similarly, when coal maintains a share above 55%, the average price not only increases, but the market also experiences more pronounced volatility. This is a result of inflexible base-load operations and the ongoing costs associated with maintaining ageing coal infrastructure.

The Tipping Point: High renewables lead to cheaper power

NEM data also demonstrate that when renewable energy consistently provides more than approximately 50% of electricity supply, wholesale prices fall below $100/MWh.

This represents a crucial tipping point: before renewables reach this “critical mass,” gas and coal continue to set the market clearing price, keeping overall prices elevated—even when significant renewable generation is available.

Longitudinal, volume-weighted data from the NEM shows that as the share of renewables increases, price spikes become less frequent and baseline prices drop.

However, these benefits only become reliable once renewables constitute a majority of the supply, rather than just a notable minority share.

This is a fundamental aspect of market design: until renewables are setting the price in more than half of trading intervals, fossil fuels with their high and volatile costs will continue to keep prices high.

The transition challenge: Learning from real data

A significant challenge during this transition is the lack of historical data, as such high levels of renewables have not previously existed in the market.

Policy risk aversion, lobbying from fossil fuel industries, and traditional grid planning approaches often underestimate the effects of high renewables because the scenario is unprecedented.

While many models have predicted “zero cost” or even negative pricing outcomes, real-world evidence is now supporting these projections.

The transition follows an “S curve” pattern, particularly for solar and other cheap power sources. The change is not gradual but marked by a regime shift: moving from insufficient to sufficient renewable generation leads to rapid, non-linear change.

The fastest transformation in energy history (https://theconversation.com/climate-action-can-feel-slow-but-the-fastest-energy-leap-in-history-has-begun-264483).

New Data, New Policy Logic

As Australia surpasses the 50% renewables threshold, further increases are expected to drive even sharper reductions in prices and volatility.

This trend is already visible in South Australia, parts of Victoria and Queensland during high-renewable periods, and internationally in countries such as Germany, Denmark, the United States (California, Texas), under certain conditions.

Continued expansion of energy storage, flexible demand, and grid interconnection is essential to maximise these benefits, absorb excess generation, and ensure that fossil generators are no longer setting the market price.

However, the full impact of large-scale batteries is still to be determined as more operational data becomes available.

What the data tells us

Wholesale electricity prices are fundamentally shaped by the market mix. Renewables have become so affordable that, once they consistently set the majority of market prices, the benefits extend to all consumers – except legacy fossil fuel generators.

Policy decisions should move beyond misleading “snapshots” and focus on comprehensive, system-wide, weighted data at scale.

The evidence – both in observed data and modelled projections – shows that delaying the attainment of critical mass for renewables does not result in cost savings. Instead, it prolongs high prices and entrenches reliance on fossil fuels.