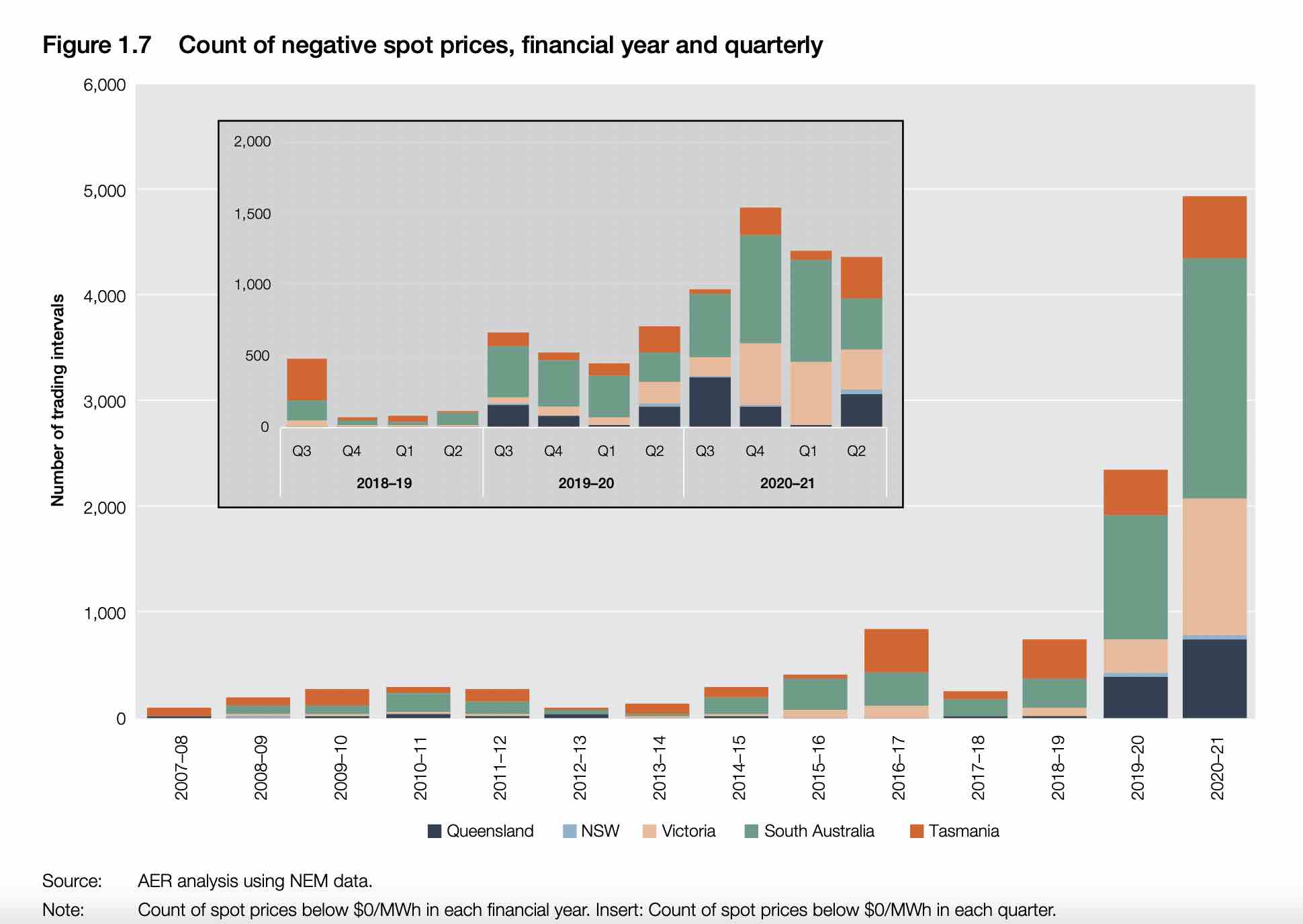

Australia’s main grid recorded a record number of negative price trading intervals in the last financial year – nearly 5,000 – as the growing impact of rooftop solar forced baseload coal generators to scramble to try and avoid having to stop and then re-start their generators.

New data from the Australian Energy Regulator shows there were 4,931 negatively priced trading intervals in 2020–21 – more than double the previous high recorded a year earlier.

The number of negative priced intervals were at record highs in each quarter, and increases in every state apart from Victoria. South Australia led the way with more than 2,000 negative pricing intervals.

Negative prices are not a new phenomenon, because coal generators have for years bid prices below zero – particularly overnight when demand was low – to ensure they got “dispatched” by the market operator and didn’t have to switch off or ramp down their generators.

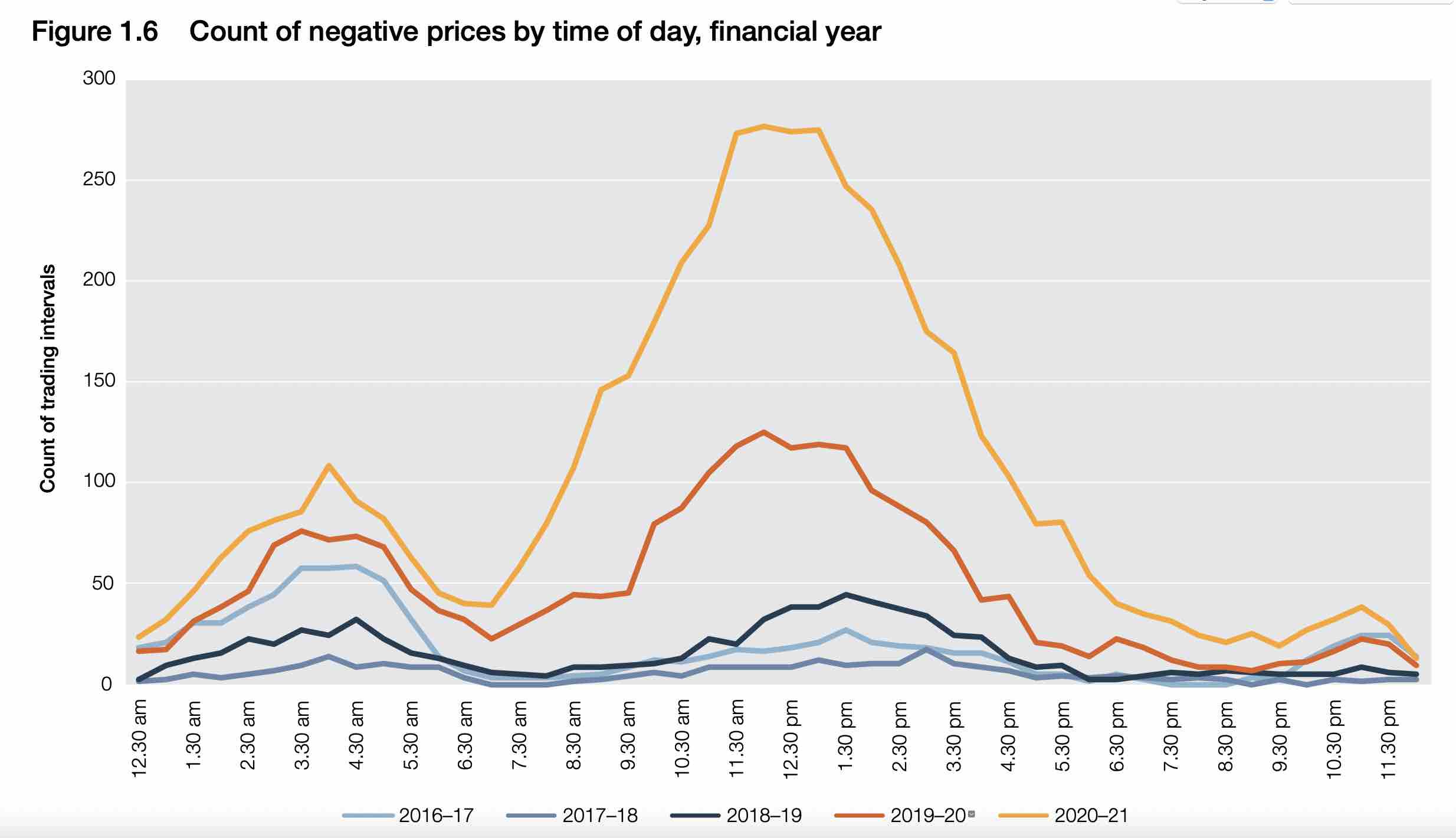

Now the arrival of rooftop solar – and the reduction in “grid demand” – is causing most of those negative pricing events to occur in the middle of the day.

Wind and solar farms usually dodge the negative pricing events – either because they are required to do so by the contracts they sign with big retailers, or because automated trading systems allow them to respond quickly to changes in prices.

Coal generators, as Queensland coal company Stanwell explains, “incur significant costs stopping and starting and require many hours to restart.

“This means they continue generating throughout negative pricing periods as it is more cost-efficient to incur the costs of negative pricing than shutting down and then starting up again.”

That means that it is the coal generators bidding the prices below zero to ensure they are “dispatched”. The problem is, there is not enough room in the market for all the inflexible “baseload” in the grid.

It is why most in the industry accept that the days of “baseload” is over, and will be replaced by flexible and fast-reacting kit, mostly inverter-based technologies such as wind, solar and battery storage.

The negative pricing events are also a strong signal for battery storage, but so far Australia does not have enough big batteries to make a serious dent in the market.

One reason is that batteries need multiple revenue feeds to make them profitable, and many of the services they can provide are not rewarded by the market, although new services such as “fast frequency response” are being introduced.

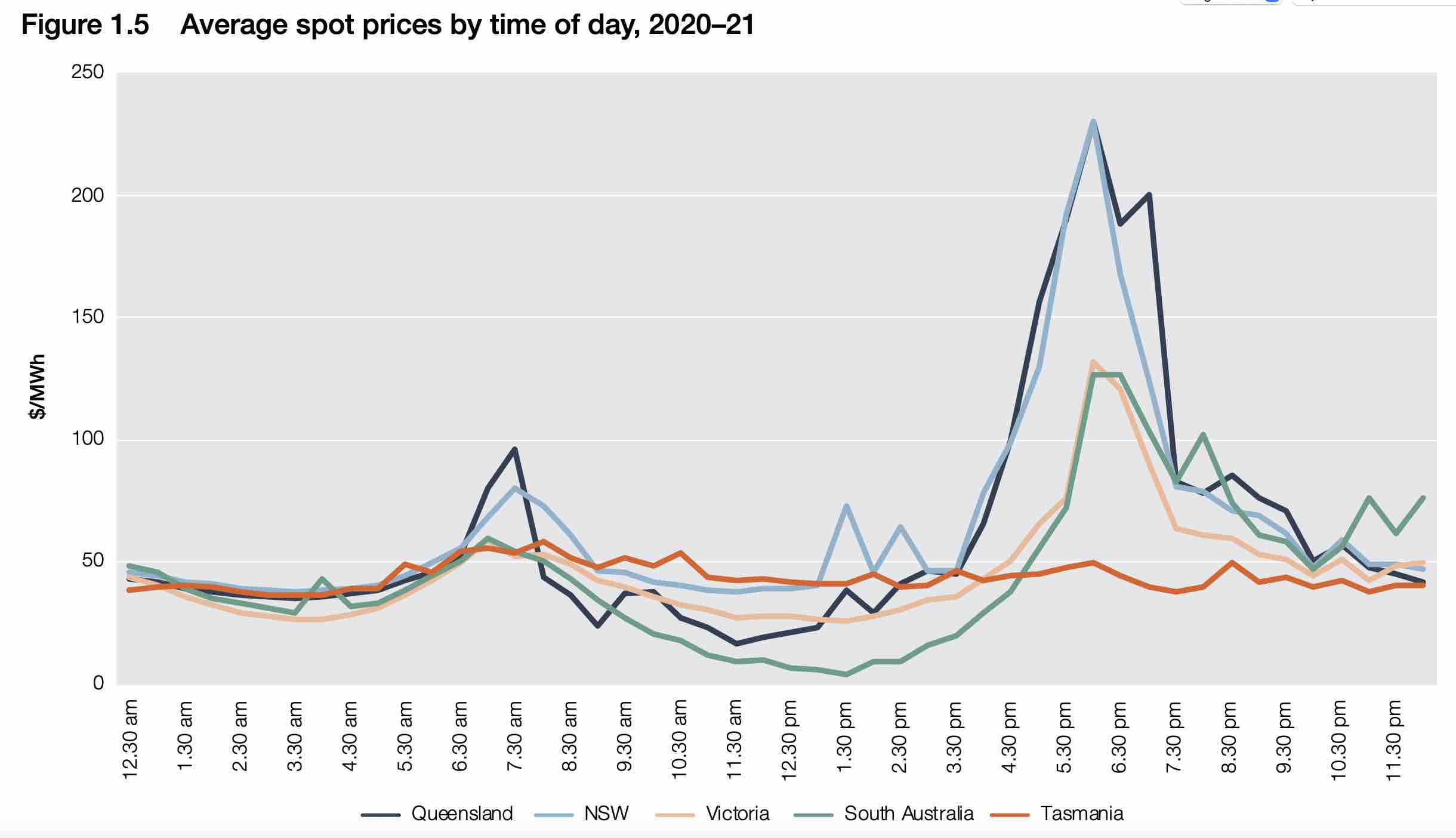

South Australia has the most negative pricing events because it has the highest share of rooftop solar, and it also has to cram enough gas generation into the system to ensure there is enough “system strength” in the local grid.

The commissioning of four new synchronous generators – spinning machines that do not burn fuel – means that the amount of gas generators needed to run at any one time for grid services will be significantly reduced. Over time, that service is expected to be provided by battery storage and “grid forming” inverters.

See also: 1,000 days of baseload outages: Coal failures send electricity prices to record highs