Australia stands to lose its place in the world’s foremost global solar research group, a leading industry insider has warned, in the absence of federal government funding to support the participation of Australian experts.

Renate Egan, the secretary of the Australia PV Institute, or APVI, says time is running out to ensure Australia’s ongoing role in the Photovoltaic Power Systems Program (PVPS), established by the International Energy Agency in 1993 as an international collaborative effort to advance the role of solar in the global energy transition.

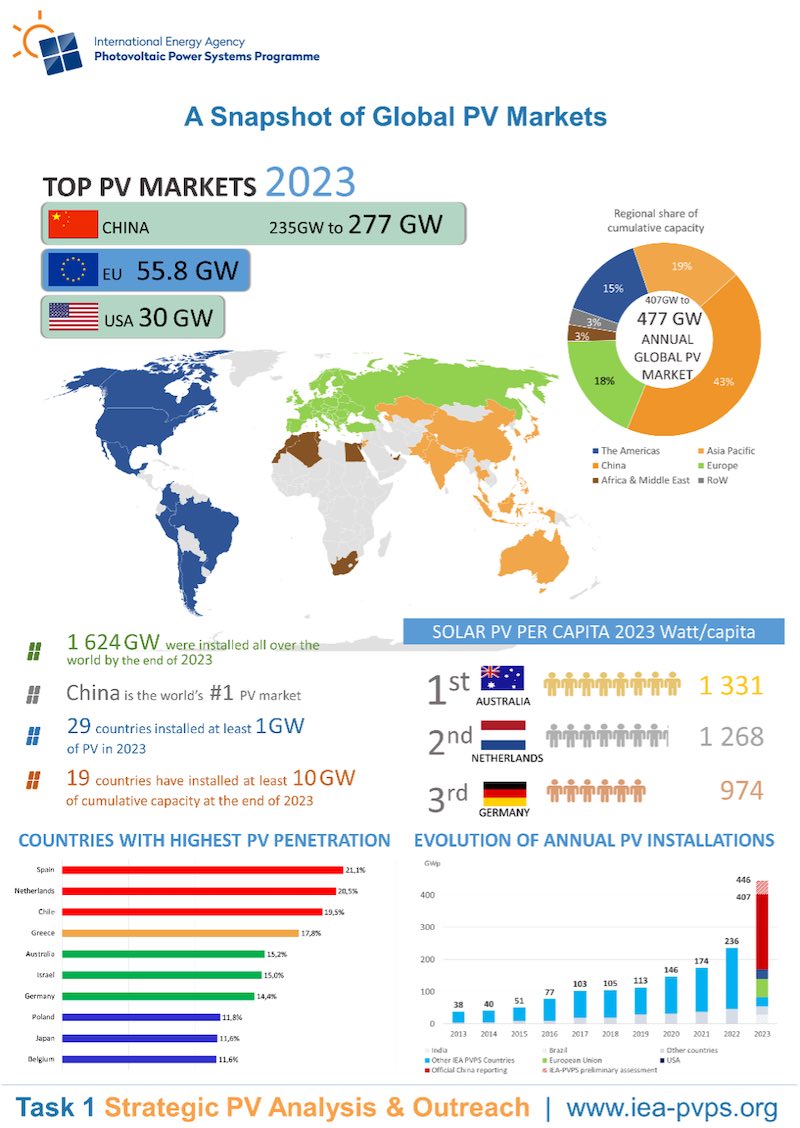

As part of its mission, the IEA PVSP puts together an annual Snapshot of Global PV Markets, the latest of which was published this week. Australian data used in the report is supplied by APVI.

Egan says that without renewed funding, Australia risks losing its place as one of the 31 countries contributing expertise to the IEA PVSP and major research efforts like the annual Snapshots – an “extraordinary” turn of events, considering the federal government’s newly announced $1 billion dollar plan to build a domestic supply chain.

“We’ve been trying to work with government on a solution for close to a year and if we don’t have a solution soon, then Australia will need to withdraw from the IEA solar programs, which is an extraordinary situation, given the commitments that Australia is making to solar,” Egan told RenewEconomy.

Meanwhile, a look at the 2024 Snapshot of Global PV Markets, reveals some more areas where Australia is losing ground in the race to solar, despite its huge natural advantages of abundant space, rooftops and sunshine.

Egan says that while Australia in 2023 retained its world number one status for installed solar per capita, it is at risk of losing this title to the Netherlands, which Egan says is gaining ground “really quickly” and could edge ahead by the end of 2024.

And while Australia remains in the chart for the highest fraction of total electricity demand met by solar, at number five, it has – for the first time in 20 years – fallen out of the Top 10 countries for new installations, falling well short of the 4.2GW of new PV capacity required to be included for 2023.

More broadly, the IEA PVPS 2024 Snapshot reports that global cumulative solar capacity grew to 1.6 terrawatts (TW) in 2023, up from 1.2 TW in 2022, with from 407.3 GW to 446 GW of new PV systems commissioned – and in the order of an estimated 150 GW of modules in inventories across the world.

“After several years of tension on material and transport costs, module prices plummeted in a massively over-supplied market, maintaining the competitivity of PV even as electricity prices decreased after historical peaks in 2022,” the report says.

The standouts for the year once start with China, which the report reveals installed a record 235GW (or even up to 277GW) or over 60% of new global capacity reaching 662GW of cumulative capacity.

“Remarkably, this annual capacity represents over 15% of the total global cumulative capacity and is nearly the equivalent of the second largest cumulative capacity: Europe,” the report says.

Europe, meanwhile, installed 61GW for the year (55.8GW in the EU), led by a resurgence in Germany (14.3 GW) and increased volumes in Poland (6.0 GW), Italy (5.3 GW) and the Netherlands (4.2 GW), while Spain dropped slightly (7.7 GW).

The US installed 33.2GW while India’s installations slowed a little to a total of 16.6GW. In the Asia Pacific region, Australia slowed – as we know – to a total 3.8GW for the year – while Korea installed 3.3GW and Japan 6.3GW.

The report also notes that the share of solar in electricity grids around the globe continues to grow, with the number of countries with theoretical penetration rates over 10% doubling since last year to 18.

On this metric, Australia remains a global leader, coming in fifth in the world for the biggest share of solar in its national electricity mix – most of this, of course, generated on rooftops.