The Strait of Hormuz is far from Australia, but in every energy crisis there is a reminder that energy security is not currently measured by how much sun a country has falling on rooftops. It is measured by what keeps moving when oil markets seize up, shipping insurance rates spike, or refined fuel cargoes get repriced in a week.

Australia likes to describe itself as a renewable energy superpower in waiting, and on electricity supply potential that is fair enough. But the country still runs a large share of its economy, and especially its mobility, on imported liquid fuels exposed to global chokepoints.

The lesson from Hormuz is not that Australia needs a new panic plan for the Gulf. It is that the country needs to get serious about electrifying the parts of its economy that remain tied to traded oil.

Richard Rumelt’s kernel of good strategy is useful here because it forces discipline. Diagnosis comes first. Then guiding policy. Then coherent actions. Australia has spent years discussing electrification, vehicle charging, bidirectional charging, rooftop solar, batteries, tariffs, and standards as if they were all equivalent pieces of a buffet. They are not.

The diagnosis is that Australia is behind on economy-wide electrification. The guiding policy should be to accelerate electrification where it is commercially ready and strategically important. The coherent actions should start with the measures Australia can control directly, rather than the technologies it can only encourage from a distance.

On the diagnosis, the numbers are plain. The Department of Climate Change, Energy, the Environment and Water’s Australian Energy Flows for 2023-24 shows final energy consumption of about 1,121 TWh, of which only about 241 TWh was electricity.

That means Australia is only about 21.5% electrified on a final energy basis. The rest is still mostly oil, gas, and smaller amounts of coal and other fuels. Oil alone accounted for about 654 TWh of final consumption.

This is the reality hidden behind the solar success story. Australia has done a great deal on renewable electricity generation, but it has not yet done nearly enough on replacing combustion across end uses. The country is not failing to build electrons. It is lagging on using them to displace molecules.

Australia’s formal organizations are all in petajoules (PJ), but I choose to express energy in its final, dominant expression, units of electricity. Electricity is billed, planned, modeled, and debated in kWh, MWh, GWh, and TWh. PJ is useful in national energy statistics because it lets coal, oil, gas, and electricity all sit in one accounting frame.

But it obscures the practical question: How much electricity would Australia need to replace fossil energy services, and where is it being used now? TWh is the more intuitive unit for that conversation. One TWh is 3.6 PJ. Once the article turns from aggregate fuel accounting to strategy, TWh makes the scale of the problem easier to see.

The transport data make the point sharper. Transport consumed about 489 TWh of final energy in 2023-24, and only about 7.2 TWh of that was electricity. That is about 1.5%. In other words, the biggest block of final energy in the economy remains barely electrified.

Residential is already much further along, with about 70 TWh of electricity out of about 133 TWh of final energy. Commercial is further still, with about 64 TWh of electricity out of about 87 TWh. In large part that’s due to Australia being a sunburnt country that needs more cooling than heating.

Manufacturing and mining are lower than buildings, but both are still substantially ahead of transport. If the objective is to move the national electrification needle in the late 2020s and early 2030s, passenger road transport is the obvious place to focus. This is not because industry, freight, or buildings do not matter. It is because road transport is where the largest unelectrified energy block overlaps with a mature and scaling technology path.

That strategic focus looks even stronger through a useful energy lens. Australia’s TWh energy flow Sankey diagrams make the core point well. Australia uses far more input energy than it needs for the services it actually values because combustion wastes so much energy as heat.

Internal combustion vehicles are a clean example. A battery electric vehicle commonly turns 70% to 80% of the electricity stored in the battery into motion at the wheels. A gasoline vehicle often turns only 20% to 25% of the fuel’s energy into motion, with the rest lost as heat. Even if one stays away from exact one-for-one comparisons across driving cycles, the order of magnitude is not controversial.

Replacing combustion in passenger transport is not just fuel switching. It is a large efficiency gain. That is why electrification can cut total energy demand while improving the same energy services.

Australia is well placed to benefit from that in a way many countries are not. The country has built one of the world’s largest distributed solar fleets. The national CER roadmap says Australia reached its 4 millionth rooftop solar system in December 2024, average rooftop system size reached 9.9 kW in the first quarter of 2025, and smart meter coverage reached 60% of National Electricity Market customers.

The Clean Energy Council reported that rooftop solar had risen to 4.3 million households by the end of 2025, with 28.3 GW of installed capacity. Australia does not have a lack of midday electricity in many places.

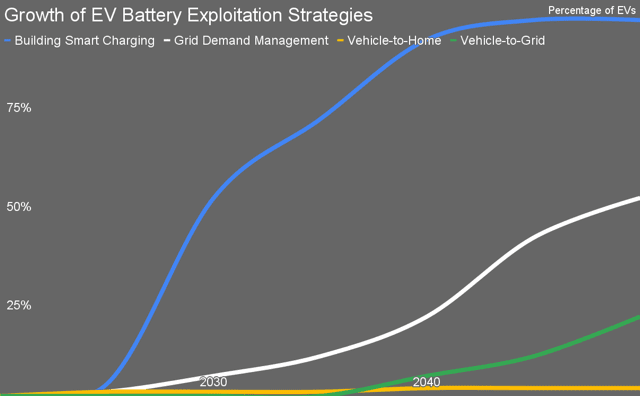

It increasingly has a challenge of using that electricity productively and then managing the late afternoon and evening when rooftop solar output falls away. That is why the first and biggest grid value from electric vehicles is not glamorous. It is demand management.

Growth of EV Battery Exploitation Strategies by author

This is the point many discussions still miss. The first systemic prize from millions of EVs is not that they can discharge to the grid. It is that they do not have to charge at the wrong time.

AEMO’s 2025 Electricity Statement of Opportunities for the NEM and the parallel WEM outlook for Western Australia both point to the same broad pattern. Peak stress is increasingly in the late afternoon and evening, after solar generation fades, and in Western Australia the peak is extending later into the night.

That means badly timed EV charging can deepen the problem, while well timed EV charging can help solve it. A car that simply waits until after the evening peak, or better yet charges during a midday solar soak window, is already providing system value. No bidirectional power flow is required. No export settlement is required. No debate about battery warranty is required. The charger just needs to be smart enough, and the tariff or control signal clear enough, to avoid charging at the wrong time.

That makes demand managed charging the highest value proposition for Australia in the near term. It is the part of the solution that the country can influence most directly. Distribution businesses and regulators already shape tariff structures through Tariff Structure Statements approved by the Australian Energy Regulator.

The AER’s own work on facilitating consumer energy resources points directly to time of use tariffs and solar soak periods as ways to steer EV charging into times when distributed solar is abundant.

Network proposals in Victoria are already moving in that direction. CitiPower’s tariff proposals reference an 11 a.m. to 4 p.m. solar soak period and assume EV charging responds to time of use pricing by shifting away from peak. Jemena has proposed a default residential time of use tariff with a daytime solar soak component. This is the sort of thing Australia can do with its own institutions, its own rules, and its own retailers.

As Daniel Kahneman argued in the work that led to his 2002 Nobel Prize in Economics, people do not approach choices as frictionless optimisers. They rely on fast intuitive judgment, are loss averse, and show a strong bias toward the status quo.

In his Nobel autobiographical essay, Kahneman said loss aversion was central because people respond more strongly to losses than equivalent gains, and that this helps explain a widespread bias favoring the status quo in decision making.

Applied to EV charging, that means a complicated mandatory time of use tariff asks households to study unfamiliar rules, trust that they will not be penalized, and actively change established behavior, all of which feels like risk and effort. A default smart charging profile does the opposite. It uses choice architecture to make the beneficial behavior automatic, while preserving the option to override it.

Behavioral economics and cognitive science both suggest that when a policy depends on millions of households making repeated complex decisions under uncertainty, adoption will be weaker than when the system quietly makes the low-cost, low-risk choice the default.

There is an important nuance here. Australia can do more with opt out or default smart charging than with universal mandatory time of use billing in the near term. Most consumers don’t understand dynamic tariff structures. Not every consumer trusts them. Some will be worse off if poorly designed tariffs shift risk onto households that do not have flexibility. But an EV charger does not need the owner to become a part time energy trader.

It can come with a default profile that delays charging out of the evening peak unless the driver overrides it. A retailer can offer an EV charging product with a simple off peak default and a visible price advantage.

A network can create the framework for dynamic EV charger management without forcing every household into a complicated tariff. The strategic insight is simple. Consumers should have to opt out of good charging behavior, not opt in after reading a small thesis on network pricing.

If demand management is the first value proposition, vehicle to home is the second. Australia has a housing stock and consumer energy stack that make V2H more plausible than in most jurisdictions. According to the Australian Bureau of Statistics, 72.3% of occupied private dwellings are separate houses. Car ownership is high. Owner occupation is high. Rooftop solar penetration is high.

The federal government’s V2X (vehicle-to-any) guidance notes that V2H can reduce home energy costs during peak times and reduce reliance on the grid when it is constrained.

That is a logical fit with Australian housing. A household with a detached home, driveway, rooftop solar, and an EV parked at home in the evening has a clean use case. The car can absorb midday solar or off peak electricity and then cover part of the late afternoon and evening household load.

For many households, that value proposition is easier to understand than exporting back through market arrangements to support the wider grid. As I’ve noted a couple of times, it’s much more aligned with Kahneman’s prospect theory insights than vehicle-to-grid’s (V2G) value propositions.

But V2H has headwinds, and they are not trivial. The federal government says that currently very few EVs in Australia have V2X capability confirmed by the vehicle manufacturer.

That is a blunt statement, and it matters. It means the household case may be attractive, but the product market is immature. There are also charger costs, interoperability concerns, installation requirements, and battery warranty questions.

The Arena and RACE for 2030 National Roadmap for Bidirectional EV Charging is useful partly because it admits, in polite language, how early the market still is. It is a roadmap to commercial adoption, not a review of a mature mass market.

It also notes that certification processes under the latest standards were still untested and that this creates a risk reward tradeoff for international supply chain participants. In plain terms, the market is not ready for rapid mainstream takeoff.

That is why V2G sits third in the sequence. This does not mean V2G lacks value. It means it requires more moving parts and more maturity. A V2G proposition needs compatible vehicles, compatible chargers, standards alignment, certification, network permissions, retailer arrangements, communications standards, aggregation logic, and consumer confidence that the car will still be charged when needed and that the battery warranty will still hold.

It is notable and in my opinion incorrect that ARENA’s roadmap emphasizes V2G as the highest value and most scalable bidirectional use case and targets 300,000 V2G capable EVs by 2030. The practical reading is not that V2G is about to become the defining feature of Australian EV ownership. It is that institutions are trying to lay the groundwork for a later stage of market development, and possibly missing the forest for the trees.

This is where the distinction between what Australia can control and what it cannot becomes decisive. Australia can influence tariff design, network rules, smart meter deployment, EVSE installation standards, charger communications, retailer product design, and fleet procurement. It has policy leverage there. It has very limited leverage over global automakers’ product roadmaps.

Australia is a small global vehicle market, around 1% to 1.2% of global new vehicle sales, and it is a minority right hand drive market. That matters. A country of that size can shape the conditions under which charging happens.

Australia cannot force automotive original equipment manufacturers to prioritise bidirectional capability for consumers if they see higher priority markets elsewhere. It can help make Australia an easier and more profitable market to serve. It cannot dictate global platform decisions.

That points to a clean policy sequence. First, make demand managed charging normal. Require that new chargers supported through public incentives or retailer programs be smart chargers capable of responding to time based and dynamic signals. Require default charging profiles that avoid the evening peak and favor overnight and solar soak windows.

Standardise communication requirements so chargers can participate in flexible load programs without proprietary lock in. Continue the work on EVSE technical standards and service and installation rules. Expand smart meter coverage and data access where it is still thin.

Use fleet procurement, workplaces, and apartment charging programs to build large pools of controllable load. None of that depends on waiting for global OEMs to include standardized bidirectional charging at scale.

Australia can change how chargers deliver electricity to cars much more easily than it can make global EV OEMs build cars to Australian desires.

Second, prepare the market for V2H without pretending it is already a mass market. Australia should keep reducing standards friction, support charger certification, and make sure home energy management systems can integrate rooftop solar, batteries, and EVs cleanly.

It should focus on the near term consumer story that makes sense. Use your own solar better. Reduce your evening imports. Have a household backup option where appropriate. That is easier to sell, easier to understand, and easier to regulate than early stage V2G participation across a fragmented retail market.

Third, keep V2G alive as a longer horizon pathway, but do not let it dominate the 2020s policy agenda. V2G may become important, especially as EV fleets become larger, standards settle, and interoperable products become common. It may well be part of the 2030s and 2040s system architecture. But a strategy built around near term V2G scale would be a strategy built around the least mature piece of the stack. Rumelt would call that bad strategy. It mistakes an interesting possibility for a leverage point.

What should Australia do if it wants a coherent and effective strategy rather than a technology shopping list?

Start with the oil problem exposed by Hormuz. Passenger road transport is the most exposed and least electrified major energy use. Make EV adoption the central transport electrification priority. Then treat those EVs first as flexible demand.

Build opt-out smart charging into the market as the default behavior. Make smart chargers a near term must have for new dedicated home charging. Shape tariffs and retailer offers so that cheap midday and overnight charging becomes the normal economic choice.

Support V2H as a secondary value proposition where the housing stock and consumer economics fit. Keep working on V2G standards and pilots, but do not confuse preparation with immediate scale.

If Australia gets this right, the gains come from several directions at once. Household fuel bills fall because electricity displaces imported oil. Grid costs are reduced because EV load shifts away from the hours when the system is under most pressure. Rooftop solar gets used more productively. The national electrification rate starts moving upward faster because the largest fossil fuel demand block finally begins to convert.

Every increase in electric kilometers driven reduces the economy’s exposure to events in places like Hormuz. That is the strategy. Not gadgetry. Not technology tourism. Diagnosis, policy, and coherent actions lined up around the part of the problem Australia can solve fastest.