Back in July 2020, in a largely unheralded fashion, I wrote about Cheng Cheng and his ANU presentation on 100% renewable energy in Japan.

Given that Japan’s Prime Minister Yoshihide Suga is meeting with the US president this week, and climate change initiatives are bound to be on the agenda, it seems timely to take a break from a busy agenda on AGL, Tilt and Origin Energy domestic affairs to review Japan.

Australia exports about $25 billion of thermal coal and LNG combined to Japan and that’s about 1/3 of our total exports of those products. So the fact that Japan is pivoting towards supporting decarbonization rather than trying to stop it should be of great interest to Australia.

There is a geo political context that should be obvious to every Australian but simply put Japan and the US present a countervailing power to China in the Pacific. I won’t write any more about the politics but a starting point is this story here.

Cheng Cheng and the ANU team’s presentation is here and my write up for RenewEconomy can be read here.

I am going to repeat some of last year’s article because parts of it need repeating.

I still regard the ANU presentation as the best thing I have read on where Japan “should” focus its efforts if its serious about decarbonizing its economy.

Yes, there is a place for hydrogen, but on the face of it offshore wind could provide Japan with energy independence and lower its energy cost to be largely competitive with its competitors in the global industry.

In ITK’s view, it may take a long time for a nation to work out where its self interest really lies but eventually you can rely on self interest getting the job done.

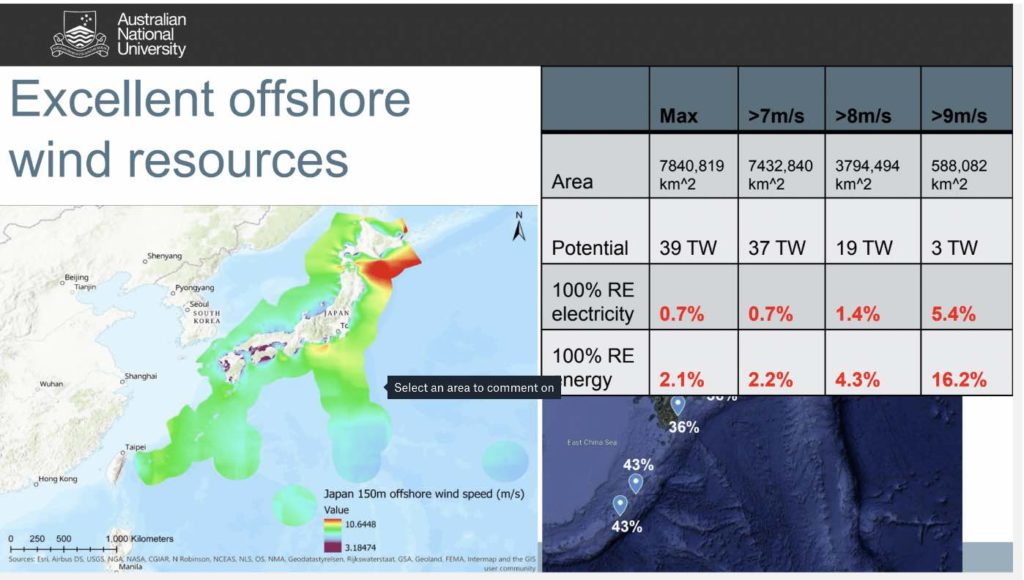

The real question about offshore wind in Japan, as covered in my article, is that it’s in water depths of up to 150 metres, when about 50-70 metres is the most for fixed foundation.

So it will require floating offshore wind.

The technology difficulties of this, although far more minor than those associated with green hydrogen, are still not to be underestimated. Imagine 15 MW turbines with 200 metre rotors, secured to ocean by cables. Imagine what might happen in a typhoon.

ANU found a wind resource of 19 TW within a 150 metre water depth horizon and with expected wind speed > 8 m/s

So, to be clear, 19 TW is 19,000 GW. It would take less than 300 GW of offshore wind to provide 100% of Japan’s electricity requirements, and yes Matt (Canavan) it would have to be firmed.

Japan energy consumption

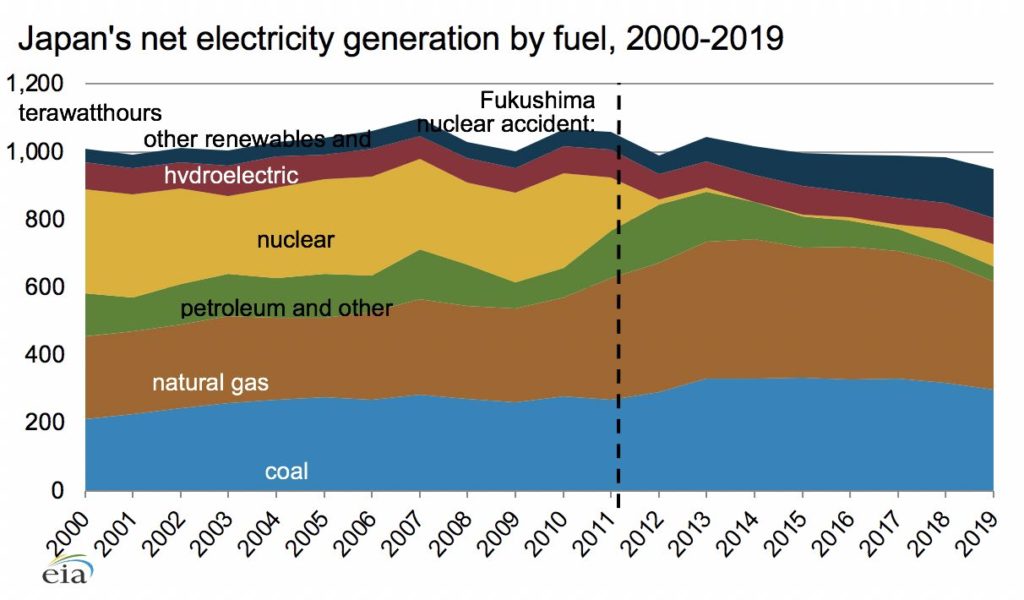

Japan imports all its coal, gas and oil and these are by far the most important sources of energy for Japan.

And the electricity production is heavily coal and gas oriented in a market only 5x as large as Austalia and similarly showing flat to declining demand.

The obvious point for Japan is that there is no point in going for Electric Vehicles if the electricity is coming from coal and gas.

Historically, Japan appears to have concluded that if decarbonisation was required then hydrogen was the only option. As this would leave Japan in a worse global position on relative costs than it was with fossil fuels then (1) resist decarbonization and (2) pursue advantages in hydrogen (and ammonia).

Japan appears to have implicitly agreed with Australia, and to an extent, other countries in South East Asia to resist decarbonization for as long as possible.

In a way you could argue that strategy has worked because, by waiting, technology has now enabled Asia not just to be competitive in decarbonizing, but possibly to gain further advantage.

Virtually every country in Asia has a strong renewable energy resource of one kind or another and growth driven out of Europe, the US and China has made the costs of accessing that resource globally competitive.

But Japan, and Singapore and perhaps Indonesia have struggled a bit on the resource side, even as South Korea, Taiwan, China, India and Vietnam have progressed their understanding of wind and solar to the point where Governments are starting to get the confidence to make big bets.

Floating offshore wind

At first blush floating offshore wind seems like a risky technology. However it can be seen as the combination of two existing technologies both of which are largely derisked:

First: fixed offshore wind, where the cost profiles and outlooks are now quite well understood. The leading example is the 3.6 GW UK Doggers Bank project with a price of around £40 (A$71)/MWh. When you add in a capacity factor of 50% (reducing firming costs) and the fact that offshore wind is better correlated with demand the price looks reasaonable. Compared to an electricity price in Japan of A$135/MWh it ought to look very attractive.

You can see costs of offshore wind here:

Second: Oil industry technology for semi submersible platforms. When you look at the European firms interested in developing offshore floating wind, its common to find oil and gas firms.

The scale of the projects and the expertise required is well suited to their skills.

Cost projections for floating offshore wind

Consider this quote from a “self interested” but very well written consortium looking at offshore wind for the UK:

“Cost reduction in UK FOW will happen much faster than it did in bottom-fixed wind. It will benefit from using state of the art turbine technology and O&M innovations.

It will also benefit from greater levels of competition for project financing, particularly in the development phase.

This, in combination with the maturity of the broader offshore wind sector means the industry will have much lower cost of capital than bottom-fixed offshore wind at the same stage of commercial maturity.

By the time the first commercial-scale projects (500MW +) are deployed in the UK around 2029-2030, we expect WACC of ~5.5%, reducing to a steady state of 4.2% by 2035.”

Figure 5 Source: “Floating offshore wind centre of excellence” January 2021

The graph shows that learning rates drive costs down more quickly in the early years if deployment is higher (ie the Govt commits). By 2030 costs are £60 (A$105)/MWh and £40 (A$71)/MWh by 2040. It’s hard to understand why this would not be an appealing prospect to Japan.

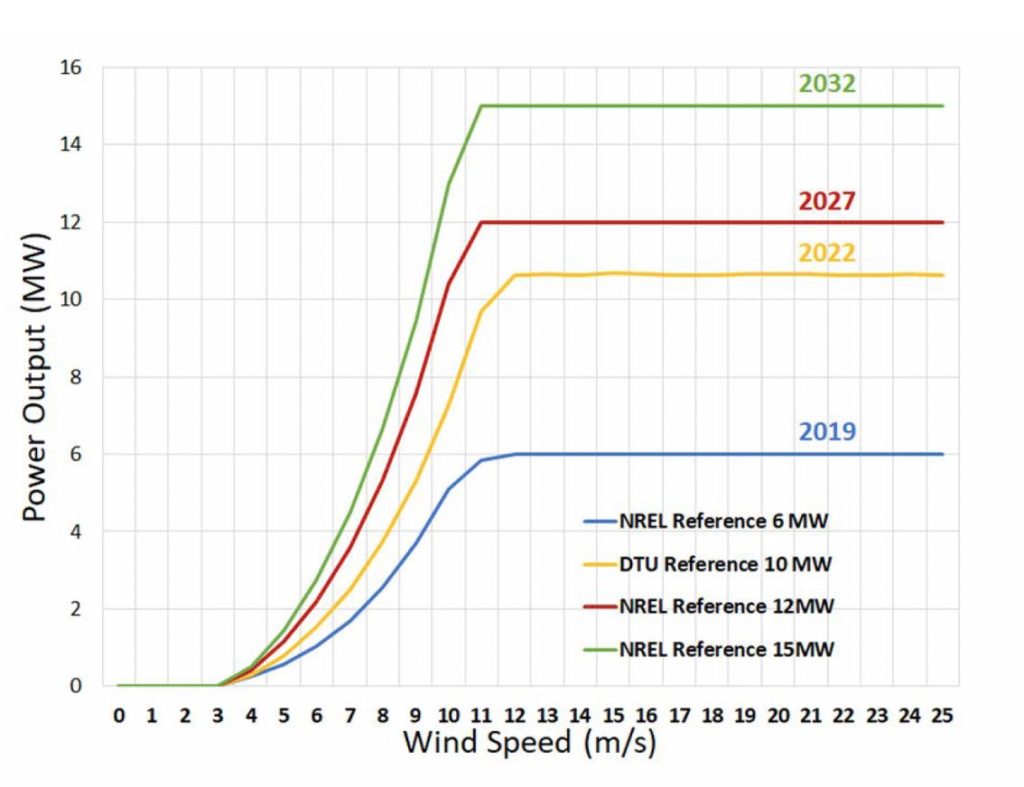

However, these projections are still conservative compared to what NREL thinks is achievable. And historically I have found NREL to be a reasonable source:

Looking at the following figure it’s probably best to focus on the 7-10 (m/s) section and not the very high wind speed best case. Even so over 10 years power output can probably double but turbine costs per MW of rated capacity decline by 1/3.

Plugging these numbers into a “Levelised cost of energy [LCOE]” model NREL finds that by 2032 offshore floating wind in Maine can be US $57/MWh.

Readers could also reference a just released study from NREL’s cousin the Lawrence Berkeley National Laboratory and reported by James Fernyhough for Reneweconomy. Actual costs have of course fallen far faster than predicted.

Current expectations for costs in 2050 are HALF what was predicted 5 years ago.

Most of the predictions are still being made by folk in North America and Europe because Asia hasn’t even properly woken up to the opportunity.

It’s funny Australian’s experience of Asia is it rarely misses a trick, but in this case, they are, so to speak, missing the boat.

Japan’s (current) targets

Japan’s Govt and Industry (Public-Private Council) released a document on Dec 15, 2020, setting out some conservative but strong foundational plans for offshore wind development.

The document complained that Japan had zero expertise in component manufacture in this sector and would have to import all the equipment etc.

So the whole program is effectively delayed while Japan gears up to 60% local content (Australian submarines anyone?)

The current targets are thus 1 GW a year to 2030 average and then accelerate to 30-45 GW by 2040. Even if the upper end was achieved that’s still just 200 TWh of electricity or around 20% of electricity demand.

Looked at another way it would result in replacement of about 30% of the existing coal and gas generation.

The document does detail the outline of a Japanese style centralized model, with a planned approach to transmission, wind development zones, port and harbor “initiatives” and

“So as to attract a wide range of companies and contribute to the realization of carbon neutrality in Japan as a whole, expedite considerations on hydrogen generation that leverages surplus electricity from offshore wind power generation and the construction of a marine transportation network for transporting hydrogen to various locations in Japan.”

Again this is as ITK has predicted (we are on a lucky streak with predictions) but it was an easy prediction.

Why wouldn’t Japan develop its own green domestic hydrogen industry if it could? And in any case it’s politically smart to work with the strong Japan hydrogen lobby.

The industry also stated it would reduce cost of “fixed bottom” offshore wind to 8-9 yen/kWh by 2030-2035 (A$ 100 MWh). ITK sees that as a very low bar, considering where the UK already is.

As we demonstrate above, Japan’s cost forecasts are likely to ridiculously conservative and the sooner they realise that the better off they will be.

Japan will have to accelerate but good foundations will help

Japan’s approach is unambitious on the face of it. For instance, there is still no pubic recognition that a strong offshore wind, and domestic solar industry, could reduce oil imports by facilitating and electric vehicle industry in Japan.

Implications for Australia

The coming NSW by-election for Upper Hunter is a classic example of the disconnect between reality and politics. The current generation of coal miners in the Hunter, at least the younger ones, are quite likely to be the last generation.

Yet every political party has a candidate that speaks lovingly of coal mining and declares warmly about its long term future.

Anastacia Paluszczuk in Queensland put it most clearly more than 4 years ago when she talked about simultaneous support for renewable energy and coal mining. “It’s what Queenslanders want” she said.

And she was right, which may partly explain why she is Premier. But actually not even Queenslanders can have their cake and eat it to.

Neither the Coalition nor the ALP federally is within cooee of the global pace. The ALP’s recent conference apparently agreed that some sort of 2030 target was desirable. Doh!

But you won’t find what that target is, because as Chris Bowen said, the ALP haven’t worked out how to achieve it, whatever “it” is.

The idea seems to be a kind of keep the flag flying approach telling coal miners and the coal mine owners (often offshore owned) it’s all wonderful and at the same time trying to slow change in Asia down as much as possible.

However, without a credible domestic policy the idea of dealing with the international implications is laughable.

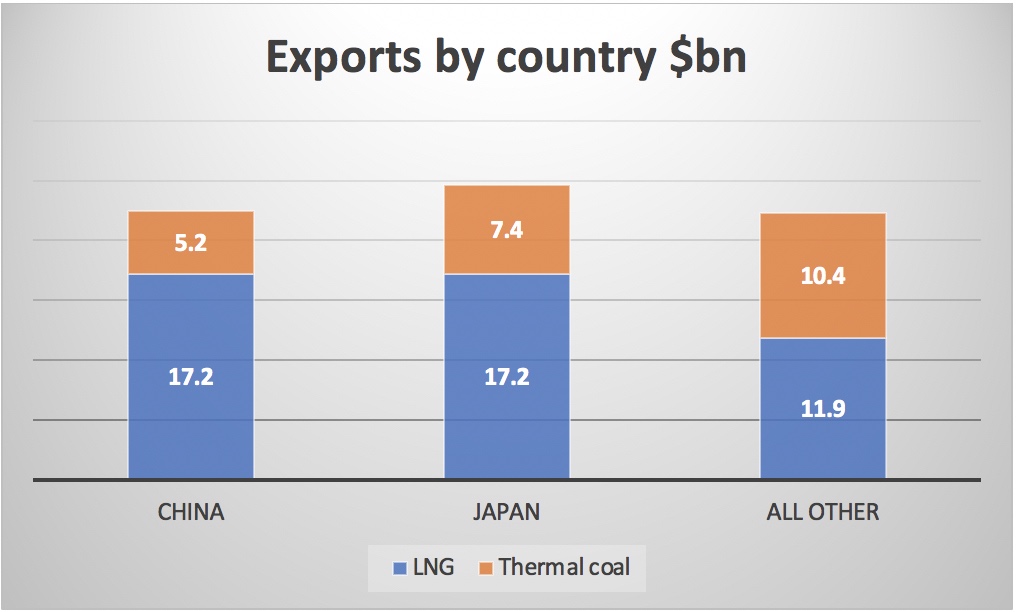

ITK already observed that Australia is the world’s third largest energy exporter, it’s all fossil fuels and it all goes to Asia. If Asia goes green, Australia needs to change. Start with gas and thermal coal. I used A$11/Gj (A$590/t) for LNG and A$100/t for thermal coal.

Looking at this chart, you can see that when the Australian Govt wants to have lower domestic gas prices it is, as usual, throwing classical economics out the window.

The highest value use of the gas is in the export market and that’s where it was sold. All Australians get the benefit of the stronger balance of trade.

Metallurgical coal is beyond the scope of this article, but for the sake of completeness Fig 4 can be extended.

On this most broad basis Japan is about 26% of Australia’s energy exports but if we look over the next 10 years with the analyst’s hard hat and hi viz vest and say not much will happen to metallurgical coal in that time (even though it should) then Japan is about 36% of the value of our combined thermal coal and LNG exports.

So change by Japan will dramatically impact those industries within the next decade. And that’s what one hopes the Government understands.

Finally the implications for Japan and Australia in electric vehicles

It’s reasonably well accepted, that Toyata the world’s leading or second largest vehicle manufacturer is nowhere in the world of electric vehicles and Japan is still clinging to the hope that world will buy hydrogen cars. But the rest of world is taking no notice of Japan.

In Europe it’s all EVs whether you look at VW, MB, BMW or Renault. In China it’s all EVs. In the US it’s nearly all EVs. When you look at your capex budget, R&D budget, logistics chain, these are company making and breaking bets.

Companies from Blackberry and Nokia have found that no amount of market share will protect you in the long term from disruptive technology once consumers get the, irony intended, bit between their teeth.

It’s hard for senior management to admit they are wrong. It’s a lot better than losing the business. There is still time for Toyota and the Japanese car industry to get with the program but maybe not so much.

Once Toyota goes electric Australia will be following suit. This is very much a second order consequence but still.