Back in 2019, the Australian Energy Market Operator considered the viability of coal generation for the Integrated System Plan, its 20-year planning blueprint. In AEMO’s words a summary of the findings was:

- “Finding 1: In AEMO’s neutral scenario, there is a forecast of sufficient revenues such that coal assets are NPV positive and are therefore likely to remain in the NEM for at least as long as AEMO estimates in the ISP.

- Finding 2: Although all coal assets are forecast to generate sufficient revenues, forecasts highlight significant variability in profitability between coal assets. Some generators may be vulnerable in particular if there is a failure in a critical part of the plant that requires costly repairs.

- Finding 3: In scenario modelling, there are some scenarios, especially those with lower demand, in which coal assets may exit earlier than AEMO estimates.

- Finding 4: The early exit of one coal asset in the NEM would improve the profitability of the remaining coal plants on the system – as such, once a coal plant exits, the chances of subsequent unplanned closures due to lacking profitability are diminished.”

ITK never agreed with finding 1.

To start with, it was contrary to our basic assumption namely that decarbonization is a sufficiently large problem that there will be enough policy around to increase the share of renewables to say 50% by 2030.

Now we think our 50% by 2030 assumption, seemingly bold in 2017, was actually too conservative.

And if renewables are going to have a big share then definitionally there will be less share and lower revenue for thermal and particularly coal generation.

For what it’s worth, we now think that if today’s quoted futures prices were accepted as accurately portraying what prices will in fact be in the relevant years, then lots of coal generation will be closing sooner rather than later.

An obvious straw in the wind was Sunset Power knocking back federal Governmnt money to refurbish units at Vales Point B in NSW.

However, it’s been ITK’s long held view that the first power plant at risk is Yallourn in Victoria.

Essentially we look for a re-run of the competition between NSW and Victorian generation that goes back to the early days of the NEM.

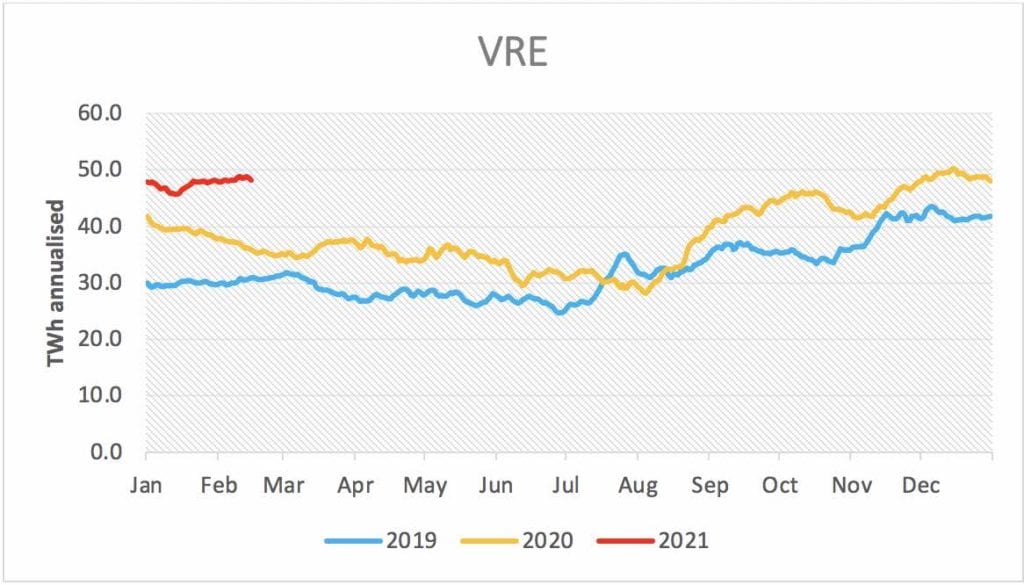

A few figures can illustrate things. And there are a couple of small inconsistencies in the data, but they don’t alter the story.

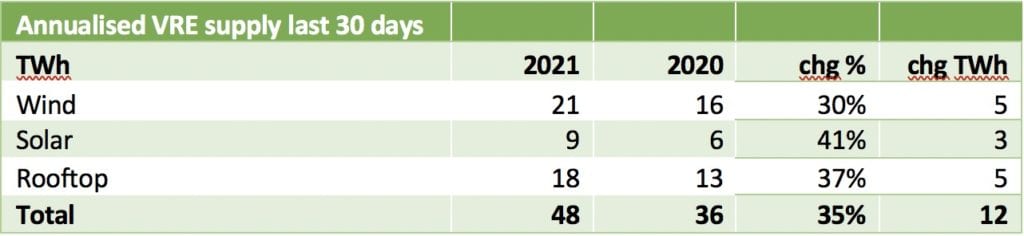

Firstly demand, even including rooftop, is down 7% on last year due mainly to a cool Summer.

Note these numbers are annualized (365/30 day moving total) but not seasonally adjusted, so the total is not representative of the full year total. And it’s just 30 days.

At the annualized rate there is a 10TWh decline in demand.

But new supply from wind and solar has strongly increased and is running at an annualized 12TWh higher than last year:

So for thermal and hydro generation they have lost 13% of their supply in 12 months.

That’s equal to 24TWh, and in turn that’s about 2 or 3 coal stations (say 3000-4000 MW depending on capacity assumption).

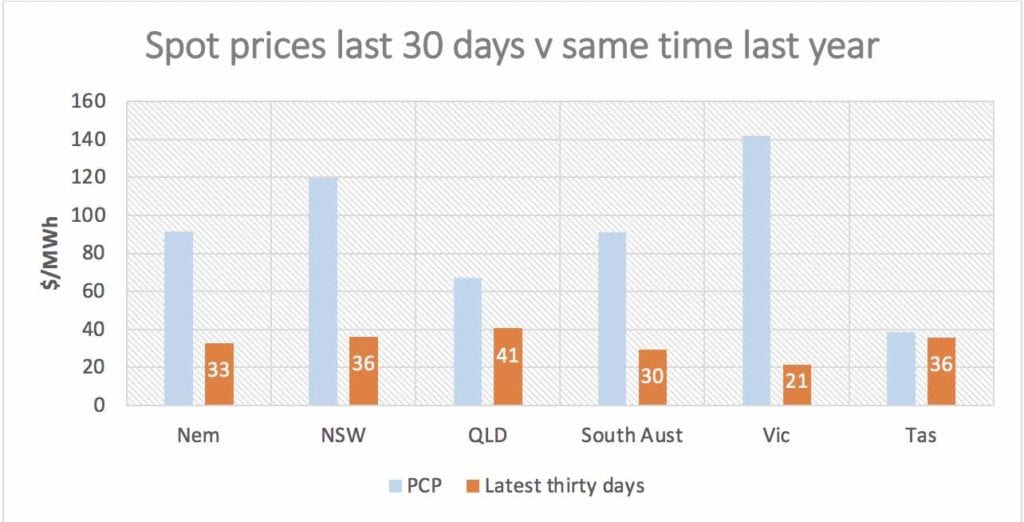

And resulting competition for share has lead to a complete collapse in spot prices.

In more detail brown coal from Victoria has lost just minimal share and has outcompeted NSW and QLD coal.

I’ll state without proof that spot prices are a lead indicator of contract prices (swaps), but they are only an indicator.

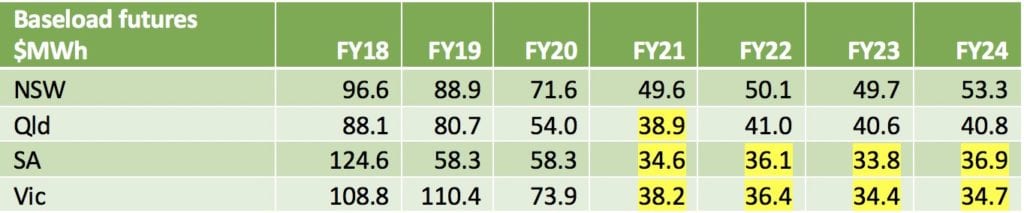

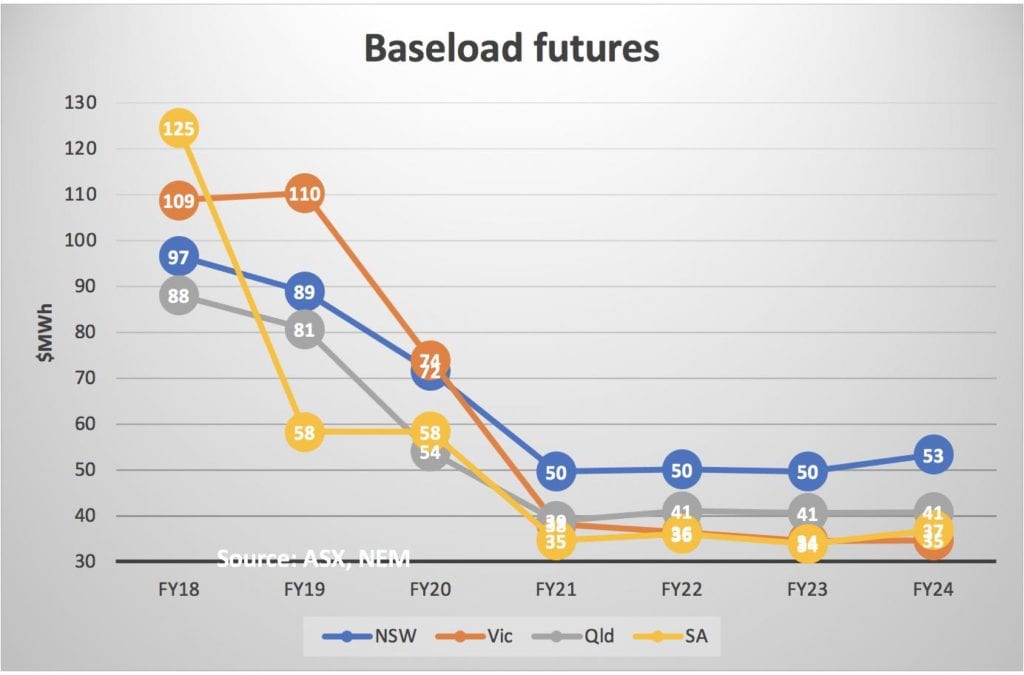

The market indicator of the contract (swap) flat or base load price is ASX futures.

For maximum clarity we show a table and a graph.These are the prices that are scary for producers particulary those that can see old hedges rolling off.

From facts to opinions

Futures prices are opinions and they can and do change.

Right now sentiment is obviously very bearish and generators will be as reluctant to contract long at prices starting with a $3 as consumers were when the price was greater than $90/MWh only a couple of years ago.

Secondly, the mild weather this Summer is very, very likely to be an anomaly and so even though things are terrible for thermal generators and going to get lots worse, it will nevertheless be the case that total demand will likely be higher next Summer.

But the real issue for thermal generation is the unending waves of new wind and solar going hitting the market every year.

About 1GW of new construction broke ground in the December quarter according to ITK records, to bring the total of assets under construction to around 2.4 GW.

On top of that we identify 3.4 GW of committed projects yet to start construction.

So that’s a lot of locked in new supply right there. And that’s all utility scale, then there’s the seemingly unstoppable momentum of behind the meter which couldn’t do less than 3-4 GW in total over the next 3 years and in all likelihood it will be more.

And beyond that is the NSW policy.

You can see the year after year squeeze in the same way that a python gradually squeezes its prey.

Two years ago VRE was an annualized 30TWh, now it’s 50TWh. Next year it will be 60TWh and the year after 70TWh.

Maybe it’s a bit slower or faster but the course is locked in.

Risk in Victoria, NSW and even QLD

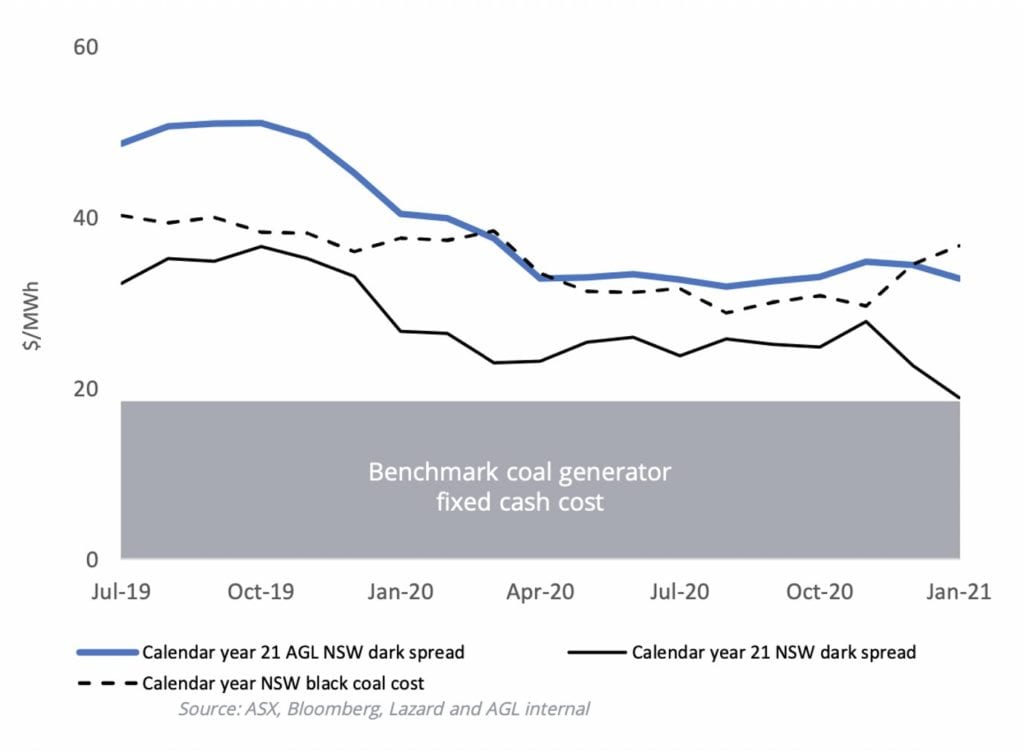

To show the problem we repeat a well publicized graph from AGL’s results presentation last week. It shows the NSW “dark spread”.

The solid black spread is the pool price minus the coal cost both in $/MWh, then the solid grey rectangle shows that according to AGL NSW coal generators have around $20/MWh of fixed cash costs.

The chart shows that as of January a generator exposed to spot couldn’t cover their cash costs (unless it was an AGL generator).

But actually, in ITK’s opinion, it’s not NSW where the problem really is, it’s Victoria.

Brown coal (mud) costs are much lower than in NSW but fixed costs are higher. External parties haven’t been able to see the actual costs of the brown coal generators for some years.

Not in fact since AGL bought out Loy Yang A minorities in 2012.

In the 2006-2012 period LYA fixed costs were increasing at about a 7-8% pace per year due to an ageing, highly paid, heavily unionised work force, the fact that the coal mine moved about 100 metres further away from the generation plant every year, higher royalties and various other issues.

Perhaps, even probably, cost increases have slowed but there is likely still some absolute increase.

In short we think every brown coal generator in Victoria struggle if prices are going to be $30-$40/MWh every year. None more so than Yallourn.

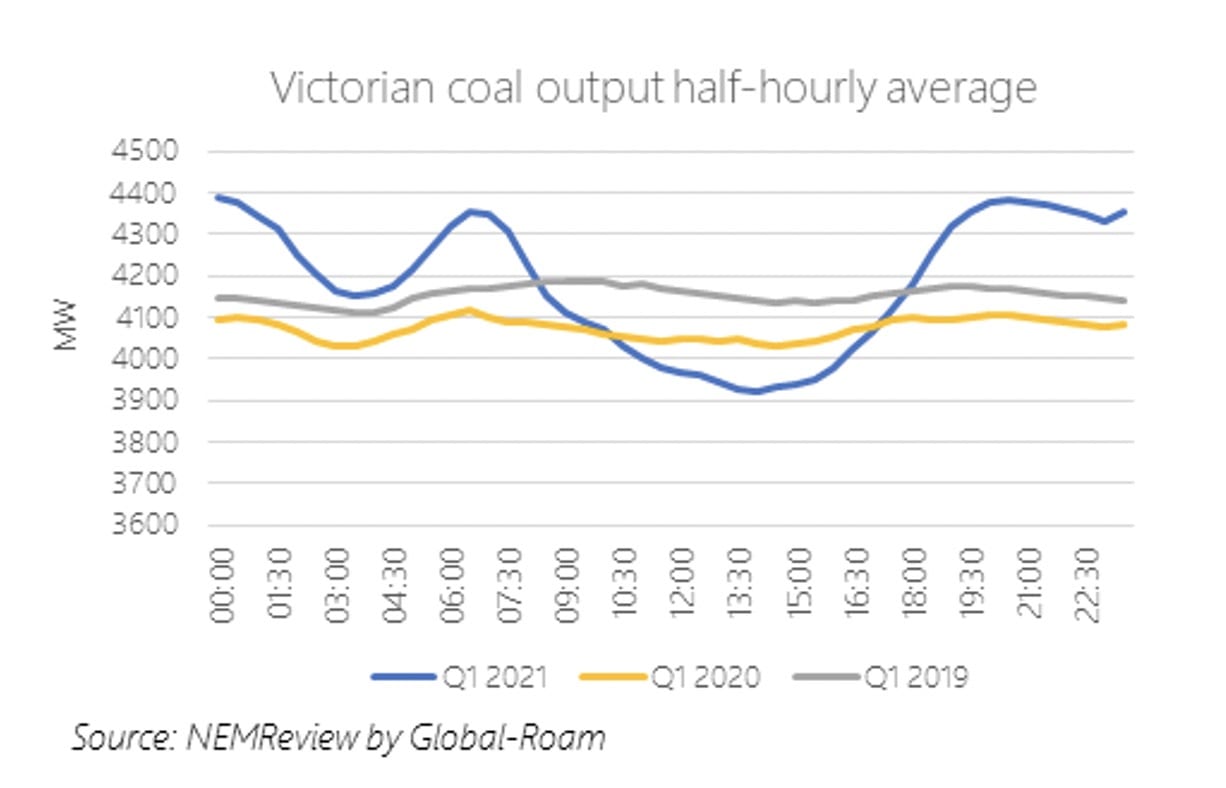

To cover fixed costs when prices are low and variable costs are low the time honored approach is produce like crazy and hope the other guy dies first.

And you can see this in Victorian brown coal output. It’s having to ramp a bit now but doing it from a higher level.

We don’t think brown coal likes to ramp but it seems to be doing 10% ramping OK.

So, Figure 8 is looking at daily or monthly averages, but in fact prices vary significantly over the day. Black coal in NSW is quite flexible and can ramp down to say ¼ of rated capacity in say 3 hours and back up again.

The plant was designed to be capable of that even if it’s not the preferred operating mode.

Not so for Victorian brown coal generators. Once we introduce significant ramp rates ITK strongly believes its Victorian brown coal generation most at risk.

The only way around that is for Yallourn to export to NSW as much as possible.

Yallourn will have to hope there is enough transmission capacity to export as often as it wants and that it can operate reliably because maintenance capex is going to be hard to justify.

If Yallourn or Loy Yang B is exporting to NSW during the day it’s likely that there will be periods of very low spot prices due to ever increasing solar share. Once the sun goes down all the NSW and QLD black coal, the gas and the hydro will compete to be dispatched.

In short there are good reasons to think that Liddell, Yallourn, Vales Point and maybe a couple of units in QLD could all close before 2030. Individually each should be quite manageable. In total it needs thinking about.