News flow – Frydenberg’s election losing speech

Mainstream media, specifically “The Australian Financial Review” and “The Australian” have taken the Federal Minister for “The Enviroment and Energy” speech to a conference today to state that the Government is “set to dump clean energy target”.

The key quote from the speech the journalists appear to rely on is

“Should reliability and affordability be compromised, public support for tackling climate change will quickly diminish and previous gains will be lost. This is in nobody’s interest….it is against this backdrop of a declining cost curve for renewables and storage, greater efficiencies that can be found in thermal generation and the need for sufficient dispatchable power in the system that we are considering the Finkel Review’s 50th recommendation to which we’ll respond before the end of the year”

There are some obvious comments that have to be made.

- The key question is political. Is a no CET policy an election winning strategy? Betting odds roughly put the ALP at 60%-65% probability of winning the next election, and that’s consistent with the opinion polls. We cannot see a no CET policy as changing those odds. The good news when the CET is officially abandoned is that at least new projects will know where they stand. And so will voters.

- Without some kind of incentive for new generation the risk of undersupply [unserved energy] increases. The NEM sends a price signal to justify new investment but as we have seen there is no political will for extended periods of high price, let alone blackouts.

- It’s quite clear to most people that the 8 ageing coal generators that supply the vast majority of electricity to NSW and Victoria need to be replaced. Ruling out a clean energy target [CET] will not get them replaced.

- The Prime Minister and the Environment and Energy minister are far from stupid. Mr Frydenberg’s speech in so far as he recounts facts is reasonably accurate and in a way balanced. As the need for more investment is obvious we therefore expect that Turnbull and Frydenbeg have some cards up their sleeve and that like Scherazades “dance of the seven veils” there is more to it than shown in this speech.

- About 2/3 of business supports a CET according to recent polling. State Govts have largely said they would support it, the Federal Opposition supports it and all the major energy companies support it.

- It’s NSW that is getting thrown under a bus if the CET is abandoned. Victoria and QLD have renewable share policies that incentivise new generation. NSW has no policy and despite being an energy importer is not getting its share of new generation investment. It’s NSW that faces Liddel risk and is having to push through environmentally unfriendly legislation to legally allow Springvale coal mine to operate when the Court of Appeal said it didn’t have a valid license. Centennial and Mt Piper have had years to address the problem. Not good enough.

- Frydenberg is the Minister for the Enviroment and the environment does have to be considered from a security point of view. Soil in Sydney is drier today than ever before recorded. CO2 emissions do cause significant damage. A good recent read on this is https://feu-us.org/case-for-climate-action-us2/ We recreate two graphs from this report that relate solely to the USA extreme weather events and consequent damages. We note the single biggest factor is severe storms.

From this perspective it’s not just electricity/stationary energy something has to be done about oil consumption both globally and in Australia. Frydenberg states that Australia has a plan, but its clearly a subtle plan because most of us can’t see it. Australia won’t change the world but being Australian means a willingness to do our bit. Since we are one of the largest per capita CO2 emitters in the world doing our bit requires an effort.

Turning to the weekly action

- Volumes:. Were up 1% this week. QLD volumes were up 4% compared to PCP which may well have been due to some rain impacting household PV production as well as higher airconditioning loads. Only Victoria saw a year on year reduction

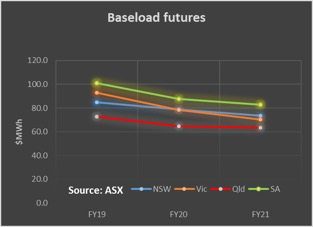

- Future prices were mixed. We have removed FY18 as the September quarter has ended and no longer quoted. FY19 prices showed only minor movement and broadly the market indicates an $80 MWh baseload outlook

- Spot electricity prices were little changed on last week, but remain broadly double last year.

- REC. No change

Gas prices rose last week over the previous week in QLD and SA and fell in NSW. NSW prices remain 20% up on PCP but SA prices have fallen 5%

Utility share prices. Utility shares in general have performed poorly over the past week. Investors don’t like it when utilities such as AGL are singled out by the Government. Additionally interest rates in the USA have risen, generally a negative for utilities, and the oil price, which drives gas prices, have been softer. The two largest drivers of global share market performance are industrial activity in China (8% year on year growth and decelerating) and USA interest rates (rising). The figure below shows the USA yield curve:

Share Prices

Volumes

Base Load Futures, M$WH

Gas Prices

David Leitch is principal of ITK. He was formerly a Utility Analyst for leading investment banks over the past 30 years. The views expressed are his own. Please note our new section, Energy Markets, which will include analysis from Leitch on the energy markets and broader energy issues. And also note our live generation widget, and the APVI solar contribution.