This is a report all state and federal governments should be reading: On September 19 the Massachusetts Department of Energy Resources released State of Charge Massachusetts Govt, analysing the national and storage storage industry landscape, reviewing economic development and market opportunities for energy storage, and examining potential polices and programs to better support energy storage deployment.

This report follows on from the earlier 2015 Brattle report, storage for Texas prepared for Oncor, one of the main T&D companies in the Texas ERCOT network.

These reports are detailed, professionally modelled and far more forward looking and sophisticated than anything so far produced by traditional Australian electricity consultants such as Jacobs, Frontier, IES, Ernst & Young or ACIL Allen.

In ITK’s view, Australia is being held back, in part, because consultants in Australia provide advice to federal and state governments based on expensive models that are basically out of date. The models don’t, and in fact can’t, take an integrated (whole of system) view.

The Australian models typically add on distributed and renewable generation as an afterthought and often pay little attention to societal benefits. As a result, governments fail to get the quality advice they should get and therefore don’t fully appreciate costs and revenues of the policy decisions that they make.

Good advice makes for good policy. Good advice has to be bold and imaginative at the same time as it is holistic and conservative. Government, just like business, can’t move ahead by doing tomorrow what was done yesterday.

No doubt the consultants would argue that if they were asked the right questions they could provide the correct advice. Another problem for the consulting industry is that a modern model requires access to a large amount of transmission and distribution information. That information is typically privately owned and not made available publicly.

In order to help the modellers, the Queensland government and the federal government to get themselves back on the right track, we review these two US studies, which are exemplars of the approach that needs, in our view, to be taken in Australia.

Unsurprisingly, they come to similar conclusions. For those who don’t wish to read the detail, the short summary is that Brattle concluded that 5GW of storage was economic in ERCOT, and Alevo that 1.8GW was economic in Massachusetts.

Ahead of a proper study in Australia, or more specifically Queensland, we (ITK) would argue that even more storage is economic if the numbers are done right:

Storage adds value, but only if shared between generation and network

Both of the reports discussed below come to essentially the same conclusion. Adding storage of between 5 per cent and 15 per cent of the state’s maximum demand is economic, even considering the lower levels of renewable penetration and the lower electricity prices in those states, relative to Australia. However, it’s only economic if the benefits to both the generation and network are jointly accounted for. Neither the generation or the network system alone can get a sufficient return.

In Queensland, where the state owns both the distribution system and much of the generation, there must be an opportunity to overcome this problem. Of course, both Energex and Ergon are subject to the AER and other national framework rules just as Stanwell and CS Energy are subject to the AEMO rules. Still, we think if there was a will there would be a way.

The need, though, as Queensland starts to move towards its 50 per cent renewable by 2030 is going to become overwhelming.

Massachusetts “State of Charge” report

Massachusetts has 54TWh of electricity consumption – about the same as Qld – and the average retail price of $US153MWh is one of the highest in the US, although still well below Queensland household prices.

Modelling in the report showed that 1.7GW of storage would maximise Massachusetts ratepayer benefits. The benefits were measured by a detailed model at $2.3 billion. A summary of the benefits was:

Brattle Report

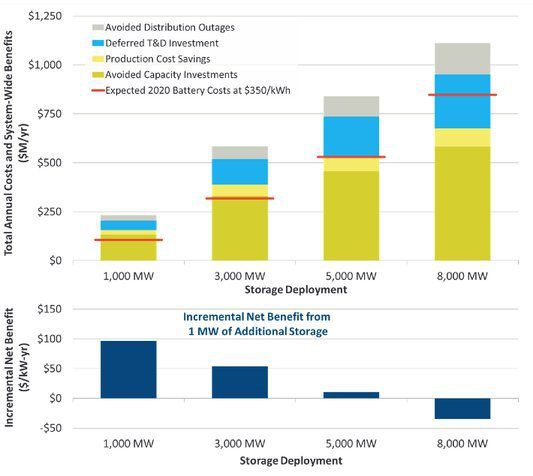

Another way of categorising the benefits and also illustrating the need for change was presented by the Brattle Group.

ERCOT in TX has 113GW of Summer capacity, and 340TWh of retail sales, with an average retail price of $US89MWh.

The Brattle Group estimated, using only some of the benefits detailed in the Massachusetts report, that up to 8GW of battery storage could be added to the ERCOT system even with Texas prices at less than 50 per cent of those in Australia. The incremental benefit was maximised at 5GW of storage.

In our view, as the amount of renewable generation on a grid grows, the amount of storage to maximise benefits also increases. In the extreme, for a grid that was 100 per cent PV-based storage needs to be about 70 per cent of final demand. We would say that the more PV there is, the more the need for storage. PV-centric systems likely need storage more than wind-centric systems.

The key policy problem – private costs shared benefits

The policy issue is that storage in several of the examples above provides benefits to the electricity system considered as a whole, but the provider of the storage can only access some of those revenues. This means that to the individual storage provider the economics may not justify the investment, even though from an overall perspective benefits accrue.

The Massachusetts report identifies policy recommendations to generate 600MW of additional storage by 2025, to capture $US800 million of system benefits.

Despite the attractive economics identified in the Brattle Report, no substantial storage projects are underway in the ERCOT network because the rules don’t allow networks to earn “generation” revenues and because of other regulatory impediments. However, at least in the US they get good advice.

Policy recommendations – Australia?

A summary of the policy recommendations from the Massachusetts report are:

- Grant and rebate programs

- Storage in state portfolio standards

- Establishing/clarifying regulatory treatment of utility storage

- Options that include statutory change to enable storage as part of clean energy procurement

- Other changes: easing interconnection, safety and performance codes and standards, and customer marketing and education

In Australia the ring fencing debate misses the wood for the trees

Despite the Brattle report indicating up to 15GWh of storage would be economic, none has been deployed because network rules only allow storage to be used for grid purposes. To maximise storage benefit requires joint revenue streams across generation and distribution. Texas ring-fencing rules prevent this. Australia has the same ring-fencing rules. If storage is economic in ERCOT, it almost has to be economic in Queensland.

The Utility industry in the USA sees storage as a game changer

We quote from the Massachusetts introduction because the message resonates like church bells here in Australia.

“Over 300 stakeholders including representatives from the utilities, municipalities, competitive suppliers, storage project developers, renewable generation developers, storage technology companies, and the regional grid operator, ISO New England (ISO-NE), participated in the stakeholder process.

The message was clear: energy storage is recognized as a game changer in the electric sector. An overwhelming proportion of stakeholders are optimistic about the future of grid-connected energy storage in Massachusetts. Utilities and developers cite renewables growth, technology advances, and technology cost decreases as factors why energy storage will shape the grid both near-term and longterm.

While recognizing the potential of energy storage, however, stakeholders identified numerous challenges and barriers that are preventing widespread deployment in the Commonwealth. Challenges highlighted are uncertainty regarding regulatory treatment, barriers in wholesale market rules, limitations in the ability for project developers to monetize the value of their energy storage project, and the lack of specific policies and programs to encourage the use of innovative storage technologies. “

USA storage market is exploding, policy is keeping up

We can put this in context by looking at the US 2015 storage scoreboard, never mind 2016:

Over 20 American States now have policies on storage. We also observe that in the US, provided the storage is deployed at the same time and on the same site as renewable energy, it is eligible for the Investment Tax Credit (the Federal level renewable subsidy).

Why are we seeing this explosive growth?

- Storage is dispatchable;

- Storage is proven;

- Storage is easy to site;

- Storage is quick to market;

- Storage is modular;

- And of course the cost of storage is coming down rapidly.

Modelling process in Massachusetts

The State of Charge modelling was done by Alevo Analytics. It took 1,497 nodes in the zone, including generator substations, transformer substations, transmission line from and to substations and load substations. From this, a subset of 250 substations were selected based on values associated with the wholesale market and distribution. Transformer ratings were factored in, but not land.

Step 1 fed the 250 substations into an “optimiser” to select the best candidates and allocate MW of storage to that substation.

Step 2 calculated the size of storage that would minimise total system cost to ratepayers before considering storage deployment cost.

Step 3 quantifies the storage according to transmission, distribution and behind the meter applications according to an optimization goal (I guess some version of a liner program) with the following parameters:

- Minimisation of wholesale market costs

- Minimisation of Massachusetts emissions

- Increased utilisation of transmission and distribution assets

- Minimisation of incremental new transmission assets

- Increasing resiliency with wide scale transmission and distribution and generation outages

- Minimisation of requirements for peaker power plants

- Stress testing with varying levels of power demand, fuel price, and renewable

Objective function of model

“The objective function of the production cost optimization determines the least cost system operations including generation cost, emission cost, and cost of lost load. These considerations are subject to maintaining system reliability of operations in terms of transmission line flows, generators’ physical limitations, power balance, and chronological ramping constraints of the generation fleet.” Source State of Charge Report

Results

The optimization results demonstrate a grid need for both short duration high power energy storage and long duration energy storage. The use of short duration, high power energy storage, where feasible, will result in a lower cost and higher flexibility of the electricity system Energy duration of the storage can be extended by decreasing the power output for a given installation of MW/MWh ratio. Source: State of Charge report.

David Leitch is principal of ITK. He was formerly a Utility Analyst for leading investment banks over the past 30 years. The views expressed are his own. Please note our new section, Energy Markets, which will include analysis from Leitch on the energy markets and broader energy issues. And also note our live generation widget, and the APVI solar contribution.