What do Bill Gates and Warren Buffett have in common? Apart from being very, very rich, it is a growing interest in battery storage and other “smart” technologies that will redefine the way our electricity grid operates – hopefully to the benefit of the consumer.

Gates has built up a collection of energy storage investments – including Aquion Energy, Ambri, and LightSail – and Buffett is a major investor in Chinese electric car and battery developer BYD, soon to unveil a home battery storage solution in Australia.

Last week, Gates and well-known cleantech investor Vinod Khosla last week bought into Varentec, a US company that is developing “smart” technology that will link storage devices and renewables, and lead to what Khosla describes as “cost-effective, intelligent, decentralized power grid solutions.”

Energy storage, as described by investment bank Citi in its new “Energy Darwinism” report, is likely to be the next solar boom. Citi says the main driver of this investment will not be just to make renewables cost competitive, because they already are in many markets – but for the need to balance supply and demand.

This, in turn, will make solar and other renewables even more attractive. It may even mean the end to the domination of centralised utilities, as storage will allow the industry to split into centralised backup (based around the old rate-of-return regulated utilities model) and much smaller “localised” utilities that harness distributed generation such as solar and storage.

This could be deployed even on a “multi street” basis, Citi says. (Yes, Grant King, the Sydney suburbs of Pymble and Gordon could go off grid – see our interview with the Origin CEO here). In Germany, some small towns are doing just that, and Citi notes that KfW, the German development bank that kicked off the solar boom 10 years ago, has now begun an energy storage subsidy program.

This presents yet another challenge for generators, which are being displaced by the huge impact of solar generation in markets such as Germany, and in Australia too.

“If, as we expect, storage is the next solar boom and becomes broadly adopted in markets such as Germany, the electricity load curves could once again change dramatically causing more uncertainty for utilities and more disruption to fuel markets,” Citi notes.

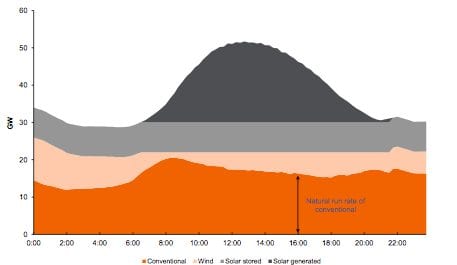

This could be good news and bad news for generators and network operators. The first graph below (figure 26) shows what is happening to baseload generation on sunny days in Germany with lots of solar. Similar impacts are being felt in Australia and the US. Baseload generation is squeezed out, but flexible gas generation finds a role.

With storage, this evens the output of solar. That’s bad news for flexible gas, because it is no longer needed as much, and while the overall level of baseload is reduced, at least it is fairly consistent.

“So, solar initially steals peak demand from gas, then at higher penetration rates it steals from baseload (nuclear and coal) requiring more gas capacity for flexibility, but then with storage, it benefits baseload at the expense of gas,” Citi writes.

“Who would want to be a utility, with this much uncertainty?”

Citi says that while energy storage is in its infancy, and subsidies will be needed for solutions that right now are still expensive and largely uneconomic, increasing amounts of capital are being deployed in the industry.

“Much of the historic investment in battery storage technology has been in the automotive sector given the development of electric vehicles. However, increasing efforts are being made elsewhere, most notably for the purposes of either small-scale residential storage (via the integration of Li-ion batteries into the inverters which convert solar electricity from DC to AC), or at a grid level.

It is important to note that while the holy grail for the automotive industry has been maximising energy storage capacity while reducing weight (electric vehicle batteries are enormously heavy, and thereby affect range, performance etc), at a residential or grid level, size and weight is far less of an issue.

“The industry is still at that exciting (and uncertain) stage where there are many different competing technologies, and it is not yet clear which will emerge as winner(s).

“At a grid level investments are being made into compressed air storage, sodium sulphur batteries, lead acid batteries, flow batteries, Li-ion batteries, and flywheels to name a few. These are all discussed in more detail in the report highlighted below.

So while storage is still very much a nascent industry, we should remind ourselves that this was the case with solar in Germany only 5-6 years ago. The increasing levels of investment and the emergence of subsidy schemes which drive volumes could lead to similarly dramatic reductions in cost as those seen in solar, which would then drive the virtuous circle of improving economics and volume adoption.”