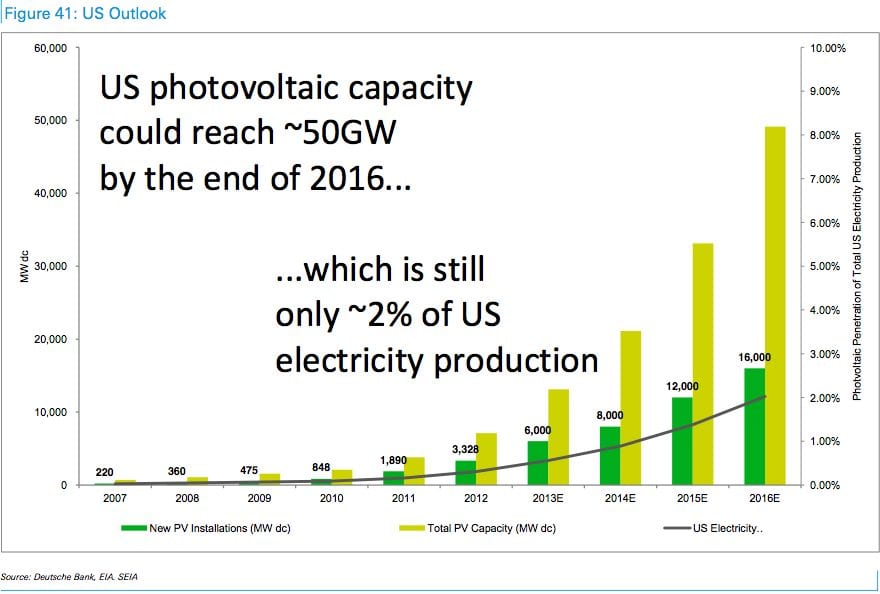

Energy analysts at Deutsche Bank are predicting a huge surge in the uptake of distributed solar PV in the United States, the world’s biggest economy and electricity market, saying solar PV installations could rise 7-fold in coming years and lift overall solar PV capacity to nearly 50GW by 2016.

The expected boom in distributed solar – installations placed on homes and commercial businesses – is based on predictions that solar PV module prices will continue to fall, grid prices will continue rise, and innovative financing options will provide ample and cheap capital.

The US solar market has been dominated by utility scale installations to date, with comparatively little rooftop solar. But Deutsche Bank estimates that in 2015 and 2016, annual installation rates will jump to 12GW and 16GW, meaning it will likely overtake China, Japan and Germany for the most annual installations.

It says total capacity will grow to 50GW under this scenario (Germany is currently 35GW but slowing, while China aims for 35GW by 2015) and it says up to 30GW of this installed solar capacity will come from distributed generation.

“We believe 2015 will be a key inflection point for solar power in the United States,” the Deutsche Bank analysts say. “The economics are already compelling in 20-30 per cent of US states and we expect this to improve as soft costs (balance of systems) come down and potential customer awareness begins to ramp.”

The Deutsche Bank scenario suggests the US will become the biggest solar market in the world. And while 50GW will only represent 2% of the country’s total generation by 2016, its impact on the incumbent electricity market could be considerable, as former Energy Secretary Stephen Chu, NRG CEO David Crane, Duke Energy boss Jim Rogers and Jon Wellinghoff, the chairman of the Federal Energy Regulatory Commission – among many otherr – have predicted.

“We see solar becoming increasingly mainstream as it passes cost competitiveness with traditional forms of generation,” the Deutsche Bank analysts write.

“While we will likely see some utilities fight at every step of the way (because it threatens their business model), we expect system economics will ultimately win in the longer run and yearly installations will continue the general upward trajectory.”

Deutsche Bank estimates that solar PV is at grid parity in 10 states in the US without additional subsidies. The key to this is the falling price of modules, and the growth of financing options, which benefit from a 30 per cent investment tax credit in the US.

It estimates that the long term cost of electricity(LCOE) for rooftop solar is currently at 11-15c/kWh in the 10 states at grid parity, which compares to a retail price of 11c-37c/kWh.

If, as it expects, solar module prices continue to fall to around $2.50 a watt from $3/watt now, then the LCOE in the grid parity states (mostly states with the best solar resource) will fall to 8c-14c/kWh, and another 12 states will come into grid parity. (See graph below).

It notes that economies of scale make modules for commercial and industrial systems even cheaper, with systems estimates at $US2.50/watt for commercial and $2.25/watt for industrial. Both prices are before the benefit of the investment tax credit.

By 2016, the number of US states at grid parity for distributed solar would be 36, if the investment tax credit was reduced to 10 per cent, or 47, if the ITC remained at 30 per cent. It says that uncertainty over the extension of that credit could cause a boom in solar investment before the deadline expires in 2016.

Deutsche Bank’s focus on the cost of financing is the key, as it plays a critical role in which technologies will be “investable” in future years, as Bloomberg New Energy Finance pointed out in its assessment of the cost of renewables versus fossil fuels earlier this year.

Deutsche Bank says the growth and popularity of “yieldco” type structures – and the fact that they make a lot of money for their investors – means that solar financing costs by will fall by 200-300 basis points, and would boost liquidity.

Deutsche Bank says the growth and popularity of “yieldco” type structures – and the fact that they make a lot of money for their investors – means that solar financing costs by will fall by 200-300 basis points, and would boost liquidity.

It says that every 100 basis point reduction in financing costs results in 1 c/kWh reduction of LCOE (see graph to the right).

“We believe solar LCOE could potentially decrease from 10-16 c/kWh to 8-14 c/kWh as a result of wider acceptance of yieldco type structures,” the analysts say. “Wider availability of financing options could provide project developers some cushion in a rising interest rate environment.”

Another big factor is the increasing price of fossil fuels. Deutsche Bank estimates that 50GW of coal-fired capacity will be removed in coming years due to pollution and emission laws.

Some new power stations may be built to guarantee supply, but this would force the regulated price of electricity higher, and make solar even more competitive. “We view this as a positive,” it says.

Finally, the bank says the price path is already proven by what has happened in Germany, which until a few years ago was the biggest solar PV market in the world, and still holds the most by aggregate with more than 35MW installed.

“We have seen dramatic reductions in system costs over the last decade and expect this to continue in the US.

“We believe we can see 10-15 per cent annual reductions in system cost/watt over the next several years, which should drive pure LCOE down to the 9-14 c/kwh range for potential grid parity states.

“Historically, we have seen this play out, although we note that much of the reduction going forward will come from non-panel costs.”

It says trends in German installation costs (shown above) show a clear down trend in a more mature industry. “We believe the US can continue its downward trend as systems become larger and soft costs couple with industry efforts towards standardization and efficiency gains to reduce the cost per watt peak before the ITC is reduced.”