The cost of key renewable energy technologies is falling more rapidly than thought, with wind already competitive with fossil fuels in many major energy markets, and solar like to achieve grid parity with conventional fuels on utility or wholesale costs in the second half of the decade.

The forecasts from global banking giant HSBC accord with some of the predictions made by the US, Chinese and Indian governments in recent months, and the outlook within the EU. But HSBC says the cost falls appear to be even more rapid, and will coincide with a carbon price that will become a “global phenomenom” in the second half of the decade.

The HSBC report says the best wind projects are already competitive with conventional power generation in many key markets, and will achieve parity in other markets over time. The biggest change has been in solar, which is moving towards grid parity quicker than expected. “The recent change of tone on this subject from many solar companies suggests that producers are becoming more confident that grid parity is a realistic ambition, given the scale of system price reductions,” it writes.

And, HSBC notes, despite the fact that nuclear and conventional fossil fuels had historically benefited from huge investments in R&D and ongoing subsidies, the rising costs of fossil prices and nuclear, and the technological advances for both solar and wind, means that renewable subsidies will be progressively cut back to zero “as cost competitive alternative energy becomes a larger part of the energy-generation mix.”

The HSBC report includes capital and operating costs estimates for all the major conventional and renewable technologies, reflecting recent transactions, as well as capital costs, fuel costs and operating and maintenance costs. It does not include solar thermal (due to slow growth) or geothermal (niche market despite interesting cost position) in its analysis.

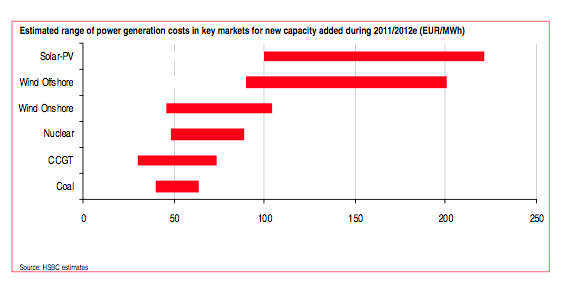

These graphs from HSCBC show where generation costs were in 2011 and where they are heading. The first graph shows the estimated range of power generation costs (in Euros) for 2011.

While this one shows where HSBC expects power generation costs (again in Euros) to be in 2015 – just three years away. The difference between these and the estimates included in Australia’s draft Energy White Paper, which contends that solar PV will still be twice as expensive in 2035, is startling.

The HSBC report goes on to make some other interesting points:

The capital cost of solar and wind (especially offshore wind) are on the higher side, but the only cost going forward is operating and maintenance cost as the fuel is essentially free.

Wind and solar costs are relatively predictable compared with fossil fuel-driven sources of power generation, as the raw material costs are zero, whereas all fossil fuel-based generation is subject to volatility in the prices of oil, gas and coal.

The least-cost onshore wind is already competitive with conventional technologies at current fossil-fuel prices and using carbon price in the EU. In the US, low gas prices (owing to shale gas availability) are posing a challenge for the competitiveness of wind technology. However, declining wind capital costs will reduce average wind generation costs by 2015, despite the risk of removal or reduction of subsidies. And in certain parts of Asia, such as India, wind is now close to the electricity sale price being offered by new coal facilities coming on line.

It says offshore wind still has a long way to go to become cost-competitive and the bank is not expecting any significant decline to capital costs until the latter half of the decade, when technology improvements, larger turbines and higher installation volumes should result in beneficial economies of scale effects.

On solar PV, HSBC says that rooftop systems have reached – or are about to reach – retail grid parity in key markets such as the US, Spain, Germany, India and China, and will achieve wholesalegrid parity in the latter half of this decade.

It noted that coal- and gas-based technologies “look very cheap on a capital-cost only basis”, but in fact the bulk of the ultimate cost of power generation is in the fuel and, to a lesser extent, the carbon costs.

It said nuclear faced a number of potential issues, including increased costs because of new safety requirements and the lack of political support in many countries. In any case, HSBC said, the capital cost of nuclear remains difficult to accurately forecast, given the complexity and scale of new build projects, decommissioning costs were variable and the cost and environmental impact of radioactive waste disposal difficult to quantify realistically

Despite its declining cost curve, or maybe because of it, HSBC warns that renewable technologies will be a difficult environment for investors.

“It seems increasingly clear that subsidies for new renewable capacity will continue to see a decline until they are withdrawn entirely. This cut in support will enforce the industry to become competitive with traditional power generation, presumably at the expense of many present participants who cannot breach such a transition. We therefore expect strong medium-term growth prospects for wind and solar, notwithstanding the current near-term pressures.”

In the near term, however, that poses challenges for people investing in listed solar stocks, even if over the longer term it will become a “mainstream technology” with volumes growing in leaps and bounds.

“Despite attractive solar system prices supporting the longer-term growth story, is it now a question of the survival of the fittest in our view.” It says demand will remain weak in 2012, pressure on margins will grow and industry rationalization will gather steam.