At the Climate Commission public meeting in Melbourne on July 24, when responding to a question, a Commissioner used what some call the drug dealer’s defence: if Australia stopped exporting coal, others would fill the gap.

Climate Commissioner Gerry Hueston explained that, in relation to Australia’s exports, “The key is to reduce the demand for these greenhouse heavy fuels, and if we stop supplying coal and perhaps even gas to some of these developing economies they’ll get it from somewhere else. So, it doesn’t solve the problem… they’ll get it from somewhere else too, if you put the price up.”

The previous night, a somewhat larger crowd gathered for the launch of the new report Laggard to Leader: How Australia can lead the world to zero carbon prosperity, published by climate and renewables think-tank Beyond Zero Emissions.

Report authors Fergus Green and Reuben Finighan outlined a very different view on Australia’s coal exports. Not only are they our responsibility, but they could be a point of leverage to kick-start a serious global response to climate change. If Australia stopped the expansion of our coal and gas export industry, and started moving towards phasing them out, it would accelerate the global transition to renewable energy.

In the absence of a global agreement in which all countries – including those who import our coal and gas – have domestic emissions reduction targets that “add-up” to a safe climate trajectory, Australia must take at least partial responsibility for the emissions caused when that coal and gas is burned, as Australia derives part of the economic benefit. Ultimately only we can choose whether to mine and ship these fuels.

But more than that, Hueston’s argument is misleading. Our coal customers can’t simply go down the road (or shipping lane) and get their coal elsewhere. It would take years for any nation or nations to replace the quantity of coal and gas that Australia ships – 27 per cent of the world’s traded coal and growing.

On paper, coal reserves to fill the Australian-sized hole exist. But there are significant barriers to that kind of expansion, and Australia is uniquely positioned to be able to grow its coal industry at that speed.

What’s involved in our coal expansion? Why can’t any other country do it?

It’s not just a matter of building new railways and ports (no small ask in themselves).

It’s trucks, roads, rolling stock, locomotives, draglines, generating capacity, transmission lines, barges, tugboats, workers, water and sewerage pipes, housing and more.

The mines need massive custom-built trucks that consume millions of litres of diesel.

Other equipment uses large amounts of electricity. For instance, Australia’s open cut mines need to co-ordinate the use of enormous dragline rigs, that weigh up to 13000 tonnes, because they each draw so much power that if you start them all at once it triggers blackouts.

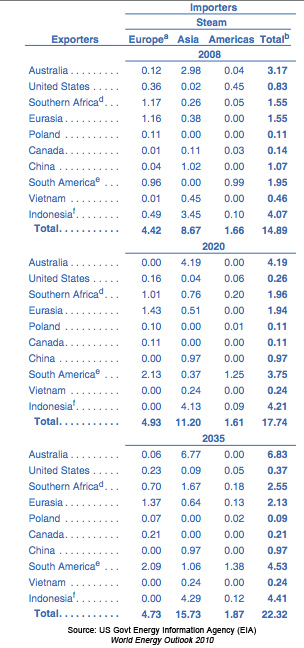

The following table is from the International Energy Agency’s World Energy Outlook 2010, based on 2008 data. It shows Australian thermal coal exports doubling from 2008 levels by the year 2035 (current estimates put this doubling forward to 2020). This is based on new mines in the upper Hunter and Gunnedah basins in NSW, and Surat and Galilee basins in Queensland, coming online.

(Note: the figures in this table are in quadrillion BTUs, a unit of energy, not tonnes).

Nevertheless, the projected rate of export increase by the other key producers in this chart gives an indication as to which countries have spare capacity, and how much they would all have to lift production to fill the gaping hole left by an Australian moratorium, let alone a phase-out. They would have to replace not just our current production, but also our projected increases.

Laggard to Leader points out that “The Waterberg mine in South Africa, for example, will take a total of 12-15 years from the application for a mining permit (in 2008) to the commencement of full productivity (in 2020-2023).”

Colombia (the main contributor to the South America figure) seems to be the only producer that is projected to expand its exports on anywhere near the scale of Australia. But even if Colombia brought its 2035 total output forward to 2020 like Australia is doing – no small ask – there would still be a big gap.

According to a 2011 Business News Americas report, Colombian coal production “could rise as high as 200Mt/y thanks to an investment pipeline of $US12.5 billion for the 2010-20 period, but at the same time major infrastructure investment is needed,” and “many of Colombia’s coal projects face the challenge of inadequate infrastructure. Investment in roads, trains and ports will be a deciding factor in whether the sector reaches its potential.”

The IEA’s Didier Houssin notes that “Among the big exporters, only US and Australia provide the market with significant spare capacity,” based on their having both spare mining and port capacity. The US, however, currently has less than a fifth of Australia’s exports (see graph).

Graph from http://www.iea.org/speech/2012/houssin_mtcmr.pdf

The challenge of replacing Australia’s coal is also exacerbated by growing domestic energy demand in some exporters. While their increased use of domestic coal doesn’t help the climate, it does make it harder to replace Australia’s exports.

Indonesia is planning to ban the exports of low-grade thermal coal by 2014. “As the world’s largest thermal coal exporter, Indonesia has often found it difficult to procure enough supplies for domestic consumption. Earlier this year, it implemented a series of measures to ensure that a portion of production was allocated to local industry,” reported the Business Standard in March 2011.

In South Africa, “Industry sources expect the growing domestic coal consumption to be in conflict with exports in the future. Eskom has responded to this challenge by locking most of the major coal mining companies into long term supply contracts.

“The South African government has previously hinted at the possibility of placing a moratorium on coal exports and ensuring security of coal supply to Eskom.”

Australia’s coal industry has taken decades of groundwork to reach where it is today, and this in a rich country with governments that legislate in favour of the coal companies, subsidise them, and help to override community opposition to new mines.

These economic and political circumstances cannot simply be cut and pasted into other countries that may already have other simmering social discontent, and whose governments don’t have billions of dollars to prop up this kind of coal expansion.

And it’s another thing again to have the political and social mandate for what could be seen as an act of climate bastardry and sabotage of Australia’s moratorium.

For example, Indonesia and Colombia are located in tropical regions facing ever more severe flooding and storm events as a result of global warming. South Africa will witness its northern neighbours enduring chronic heatwaves, horrific droughts and associated acute food and water shortages and famine on a more and more consistent basis.

Australia’s climate-denial lobby does not have a counterpart in most nations. The extreme flooding events in Manila are uncontroversially linked with global warming, and that’s normal across most of the world. Blame will increasingly be apportioned for such events.

A massive coal mining rush will cause friction in its own right; but it would probably attract far more opposition were it to also undermine what would be a highly publicised decarbonisation initiative by Australia.

The global economic impact of a freeze on new Australian thermal coal exports would in its own right help to keep coal prices up, to say nothing of phasing them out; while renewable energy is inexorably reducing in price. It could play an important role in making renewables the cheapest source of electricity worldwide.

However the global political impact of an Australian coal moratorium and phasedown would be at least as important. The and coal gas moratorium advocated in Laggard to Leader would attract global attention, and build political momentum, for a cooperative phase-down in key countries and do further damage to the already increasingly bruised moral license of the global fossil fuel industry.

So what can restricting Australia’s coal and gas exports achieve, and what is the best way to do it?

Commissioner Hueston continued, in his comments quoted above, “So the key is to work to get the demand down, in those economies, and that is a big task, and I think that is the thing that we need to confront.” In this, he is at least partly on the right track.

Hueston apparently hasn’t grasped that restricting Australia’s exports would itself lead to a contraction in demand, by pushing up the international market price.

This will only work, and be equitable, if we simultaneously make renewable energy cheaper.

The second installment of this article will look at some of the potential for “co-operative decarbonisation” that the Australian government could work towards with our regional trading partners, to help make renewable energy substitutes cheaper than coal.

Ben Courtice works as the media co-ordinator at Beyond Zero Emissions

Zane Alcorn is a BZE volunteer from Newcastle and is involved in community campaigns to phase out coal exports from the region