On May 14, the federal government announced almost $23 billion worth of initiatives under the “Future Made in Australia” Framework to spur domestic industry and accelerate the path to net zero. Since the announcement, there have been completely diverging views of its merits.

Critics have labelled it a “protectionist Ponzi scheme”, a return to old school industrial strategy and a waste of taxpayer money. Proponents have lauded it as an example of the government being proactive in laying the seeds for Australian industry to effectively compete in a new geopolitical era.

The truth is we don’t yet know and a lot will depend on the implementation details. To help understand what an effective activist industrial strategy may look like in the Australian context, it is important to look at approaches from other nations, both past and present, to ascertain how to steer clear of potential pitfalls and ensure the initiative is a real spur to Australia capturing the economic opportunities associated with the clean energy transition.

Industrial activism has, at best, a mixed record. For example, while Finland’s focus on communications technology created a world leader in Nokia and a regional cluster employing more than 18,000 people, France’s failure to turn Bull into a leading software and hardware player cost it over €15 billion.

But we also need to be clear that doing nothing is not an option either. Fossil fuel exports, which have for a long time sustained the economy, face inevitable decline.

It is also worth noting that, according to the Australia Institute, Australia provided $14.5 billion of subsidies in 2023–24 to fossil fuels, an increase of 31% on the $11.1 billion recorded in 2022–23. So industrial strategy is part and parcel of government policy. Our research from past approaches on industrial activism suggest five “non-negotiables” for success.

Lesson 1: Know thyself

Effective industrial strategy has to be based on a clear understanding of the current and potential future comparative advantages of the country, not on a wish list of what we would like to be.

For example, while Australia may harbour hopes of being a leading battery manufacturer, the lead of Chinese manufacturers like CATL and the advantages China has in terms of market size, labour costs, and R&D budget, make it unlikely any approach by Australia will yield much at least in the typical lithium battery manufacturing space. If we want to win in batteries we either need to develop new chemistries (like redox flow or Li-S or work from our critical minerals down).

Given limited government resources, interventions always create difficult choices. A strong fact base is needed to determine where government intervention can have most impact.

The Future Made in Australia Framework outlines five “tests” guiding areas to support through public investment: 1) Australia’s grounds for lasting competitiveness; 2) the role the industry will play in securing an orderly path to net zero; 3) the role the industry will play in building Australia’s economic resilience and security; 4) whether the industry will build key capabilities; and 5) whether the barriers to private investment can be resolved through public investment in a way that delivers compelling public value.

These tests are useful guidelines for public investment, and it will be important to complement this with a rigorous assessment of the economic impact of each marginal dollar invested.

In particular, it is crucial to understand what drives competitiveness in each vertical (e.g., technology, market scale, labour costs, etc.) and to dispassionately assess where Australia is at, currently, and what is feasible.

Lesson 2: Move beyond just subsidies

Industrial strategy has become synonymous with government providing strong financial incentives or directly involving itself in economic activity (through state-owned enterprises and other vehicles), often with taxpayers footing the bill.

Sometimes this is warranted; for instance, there is often a cost differential between low-emissions products and incumbent emissions-intensive competitors where markets are not pricing in the externalities from emissions. In other instances, there are disincentives to be a “first mover” into new clean tech markets.

The Future Made in Australia Framework also helpfully points out that such subsidies should “generally be time-limited, encourage early-movers and bridge the gap until an appropriate market signal is established or until the green premium in cleaner production costs shrinks.”

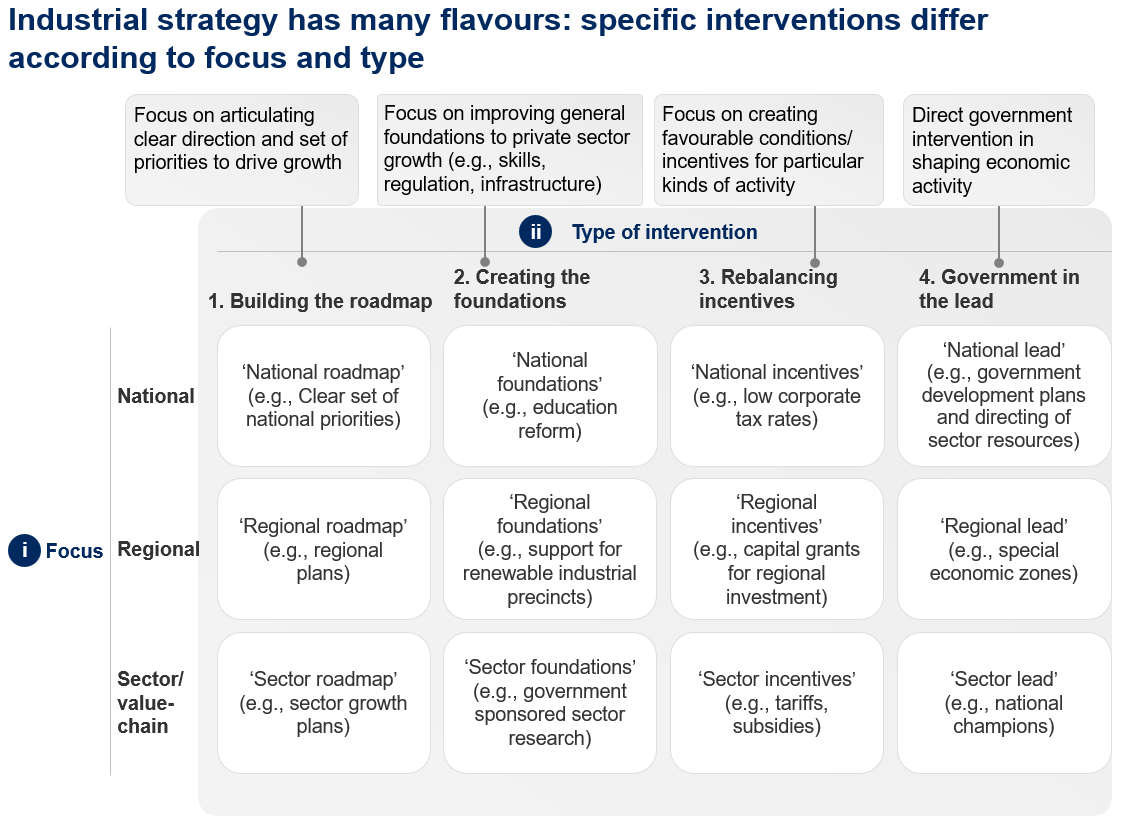

But our analysis shows that the range of options for intervention is actually far broader and more complex than this. There are four types of potential intervention, each of which can apply at the national, regional and sector/value-chain level (Exhibit 1).

The interventions should be based on the unique context related to each opportunity and should include more than subsidies. New evidence on industrial policy job creation in the United States shows that spending on improving the local business environment, such as infrastructure and specialised training, create new jobs at a fraction of the cost of government subsidies.

The focus on customised services and spending allows targeting of the specific issues and market inefficiencies that create barriers to expansion.

For example, one of the key barriers to many clean industries is the cost and time associated with government approvals. This has been partly recognised in the Federal Budget, with $168 million allocated to prioritise approval decisions for renewable projects of national significance.

EXHIBIT 1

In the case of clean energy, this could involve developing coordination mechanisms around industrial renewable energy zones and industrial precincts, supporting community groups with planning activities, streamlining regulation around approvals, developing new public-private financing initiatives and stimulating the supply chain.

The UK’s Humber Industrial Cluster Plan is an example where many of these types of initiatives are being trialled as an integrated approach.

Another general point that can be made is often there is less need for “government in the lead” and more on “building the roadmap”. For example, Australia could and should be a global leader in the production of sustainable aviation fuel given our endowments of biofuel feedstocks and renewable electricity (for power-to-liquid technologies), but Australia is currently lacking a roadmap that sets out a clear aspiration, supporting mandates and partnerships between governments and corporations to realise this.

Lesson 3: Don’t just focus on manufacturing

Industrial policy should go beyond manufacturing. Manufacturing has a role in thoughtful industrial policy but manufacturing only makes up 6% of the jobs in the Australian economy, whereas services make up 80%.

Over time, Australia’s manufacturing sector has become more efficient and automated; making jobs in this sector more, not less, scarce. Australia is not unique, this is the case for every advanced economy in the world (e.g., US manufacturing is less than 10% of total employment).

As part of the “Future Made in Australia” policy, government should think about how services can be incorporated into the industrial policy approach.

The energy transition raises new, interesting questions for services: for example, what services or business models are required to automate the renewable energy build out, what digital services will be needed in the energy transition, what new goods and services can be offered when marginal energy costs fall below zero dollars?

While some of these questions relate to manufacturing, many of these questions relate to new business models, services and organisational models that go beyond manufacturing. Australia’s comparative advantage exists in the use of renewable energy as much as the manufacture of it.

Not many countries are yet thinking innovatively about industrial policy as it applies to services but the service economy will be vitally important to the energy transition.

Renewable energy facilities need to be designed, financed, built, maintained and connected to existing infrastructure, all of which will be done by service companies. Industrial precincts and communities will need new energy sharing and financing arrangements. There is a new story on industrial policy for climate services (and services more broadly) waiting to be written.

Lesson 4: Building local capabilities doesn’t mean doing it all in-house

When Australia decides to pursue an opportunity locally, it may not mean it’s just an Australian opportunity. As a result of ambivalent policy, Australia is a decade or more behind China and many European nations in its approach to pursuing industrial decarbonisation opportunities.

Investment attraction may be a more pragmatic as well as effective way to bring advanced industrial capabilities to the country. Inviting in already established global firms can galvanise investment, skills and a supply chain at speed. Organic growth can work too, but is often slow and only a partial solution.

Australia may need a “lighthouse attraction” approach which brings in global-leading firms to locate their operations in Australia, while in conjunction working with local firms to ensure they are properly integrated into the industrial ecosystem that is created.

The Framework talks about establishing a “new front door” that will support investors with major transformational investment proposals. It is important that this front door is open to the world and not just Australian players.

Singapore is a good example of a country that follows this approach. Singapore often deliberately courts the best global companies to try and bring their capabilities and brand to develop the local economy. This is why many global manufacturing firms from HP to Micron to ABB, Merck and Siemens have set up manufacturing and digital hubs in the country.

Lesson 5: Put in place the right talent and processes to course correct

Effective industrial strategy requires the best capabilities from business and government, and extensive people interchange between the public and private sectors. The success of Singapore’s economic development has been strongly linked to the ability of key public bodies, such as the Economic Development Board, to attract and retain top talent.

No industrial strategy will go smoothly – there will always be unexpected turns. The key to success is not just striving to avoid these, but how to course correct once they occur.

The model of the East Asian development was characterised by a range of rolling approaches to industrial policy as opposed to a single set and forget policy. The industrial strategies of Germany and Finland were also characterised by frequent engagement with the private sector as plans were developed and implemented.

It is better to think of industrial policy now as iterative public-private sector collaboration as opposed to set and forget top-down regulation.

***

Australia can and should win in the development of clean energy industries – we have a bounty of low cost solar and wind sources, critical minerals as well as abundant land and proximity to rapidly growing energy markets in Asia.

Adopting these five lessons will help ensure that the Future Made in Australia Framework plays an important role in realising that aspiration.

About the authors

Dr. Fraser Thompson and Shaun Chau are co-founders of Cyan Ventures. Cyan Ventures is a specialist sustainability project development and advisory firm established to develop the “big bets” to accelerate the transition to a green, low carbon economy.