The Australian Energy Market Operator (AEMO) quarterly gas report highlights electrification of gas use is contributing to a downward trend in forecast gas consumption for commercial, residential and industrial users.

Since the 2024 Gas Statement of Opportunity (GSOO), AEMO notes domestic gas consumption has continued to decline. The reduction in gas consumption has coincided with noticeably higher retail gas prices compared to recent years and slower growth of new building approvals.

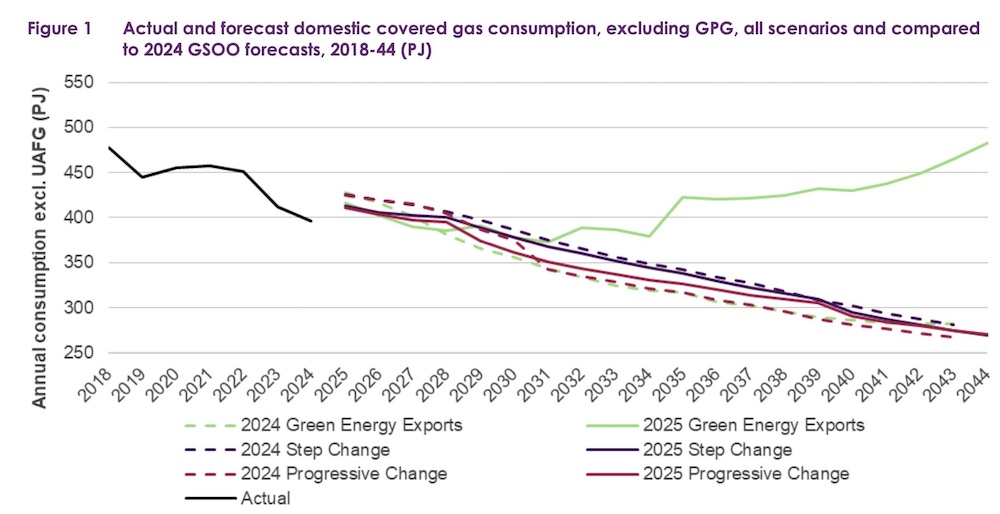

Gas consumption continues to follow a declining trend with several drivers. AEMO’s shortfall predictions are later than previously stated.

AEMO forecasts methane gas use in the National Electricity Market (NEM) will drop 60% from 145PJ in 2020 to a multi-decade record low of 60PJ in 2027, but will then miraculously more than double to 130PJ again by 2034.

Has AEMO modelled the uptake of battery energy storage systems (BESS) at an unprecedented scale in 2025 and 2026 as a permanent erosion of thermal power use? And how much V2G functionality has AEMO modelled by 2030 and 2040?

Has it factored in a significant use of the potential 1,000GWh of EV battery capacity across Australia by 2040 (up to 20m EVs at ~60kWh, plus trucking)? Think BYD charging in 5 minutes!

Given there are precisely zero new gas power plants preparing for final investment decision (FID) in the NEM, where is all this new gas capacity going to come from?

It has been entirely unbankable over the last decade, absent massive taxpayer subsidies, so why now will private investors invest in stranded assets to be following a 50% year-on-year drop in BESS prices from China over 2024 and 2025?

Climate Energy Finance is seeing a boom in Australian utility-scale solar and battery storage. We are seeing battery deals progressing across the NEM weekly, if not daily.

Think Rio Tinto and Edify Energy. As Giles Parkinson writes: “Solar battery deal for giant smelter is a stunning game-changer for Australian energy.”

AEMO’s definition of green energy exports needs re-defining.

More fossil gas is not a clean trajectory, we can’t allow the fossil fuel lobbyists to use green exports as an excuse to permanently lock in increased methane gas use.

That is definitely a risk if BlueScope contrives to wangle massive tax payer funded open-ended subsidies for methane gas to lock in increased gas use in Whyalla to make direct reduced iron (DRI). This needs to be countered by a clear contractual phase-down over time, unless there is a clear legally binding path to further decarbonisation.

Commercialisation of green hydrogen is delayed, but not dead. Time for AEMO to get real!

This article was originally published on LinkedIn. Republished here with permission of the author.