Competition, they say, is good for the market. We can but hope. Right now, it is clear there is not enough competition in the Australian wholesale electricity market, and the big players – and some new ones – are intent on making hay while the sun shines, knowing that it is their “cherished” consumers who will have to foot the bill.

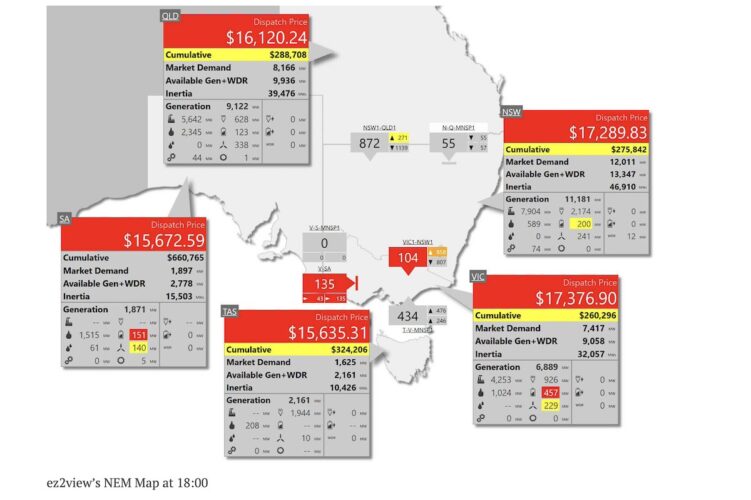

Wholesale electricity prices hit a new landmark on Tuesday night when all five states that make up Australia’s main grid, the National Electricity Market, had prices pushed above $15,000 a megawatt hour (MWh) at the same time. According to market observers, this has never been seen before.

Geoff Eldridge, from GPE NEMLog, says the average wholesale price across all NEM regions hit a jaw-dropping $16,419/MWh in the early evening on Tuesday. That smashes the previous record of $12,491 /MWh reached on July 14, 2022, at the height of the international fossil fuel crisis sparked by the invasion of Ukraine.

At this point it is too early to pin the blame on any particular generator, or any particular company for the latest price surge. But there is one thing for sure, the price has nothing to do with the actual cost of supply. At the time, there was ample in all regions. The opportunity simply arose to push the prices higher, and the generators simple couldn’t control their urges.

This has been happening for some time. Pushing wholesale prices to the market cap was a regular activity for the fossil fuel industry before the arrival of renewables. It was part of the business model, how they put cream on the cake, and in its day it this behaviour was even lauded as clever trading.

Renewables are supposed to challenge this and lower the price on wholesale markets by introducing competition. But as the number of fully dispatchable generators declines, competition at critical times has actually been reduced – at least for the time – and like seagulls around a box of chips, the market players dive in.

What we see here is naked greed, around an essential service, enabled by the ability to manipulate prices to unreasonable peaks, and the complete inability to keep any sense of proportion or perspective.

We have seen the images at the front doors of department stores for Boxing Day sales. On the energy markets, this occurs in the privacy of offices and is performed by screen jockeys. High fives and bonuses all around, and the utilities are making enough money to buy whatever they want, including governments and media.

And the problem is that in a hotly partisan energy debate, and a lop-sided and populist media disinterested in actual facts, it will be renewables that get the blame. We saw it last week with the reports on the latest June quarter wholesale prices.

But as the Australian Energy Regulator made clear, prices in NSW – the biggest grid – would have actually fallen in the June quarter were it not for the surge in prices in May when the market had to be suspended, and an automatic cap imposed.

You won’t read that much in mainstream media, if at all. According to them, it was all the fault of wind energy not blowing hard enough.

Yes, wind output was down, but the AER chronicled in forensic detail how big players took advantage of the competitive power after multiple coal plant trips and failures, to indulge in a whole series of deliberate bidding patterns, removed capacity at low prices, and were also caught in the apparent deliberate slow ramping up of units for this situation.

Not that the AER could do much about, because apparently no rules were broken. Must have been good for consumers then, although clearly not, as the AER itself observed.

The same situation likely happened on Tuesday, and to a lesser but still significant extent on Monday. And the price forecasts suggest it is going to happen again on Wednesday, and Thursday too.,

On Tuesday evening, at 6pm, there was the extraordinary sight of all five NEM markets above $15,000/MWh. It was not because of a shortage of supply, as the individual tables in this graph makes clear, but various events and transmission constraints eliminated competition enough in each of these markets to push the prices towards the market cap.

It will take some time to work out what exactly happened, and who did what, and the obligatory AER report won’t be completed for a couple of months. But some gas station trips, network constraints, and some “clever” bidding all combined to throw the prices up towards the new market cap of $17,500/MWh.

This new market cap was introduced supposedly to encourage more “peaking capacity”. And it will rise further in coming years. But rather than a price of last resort, the cap is now being used as a daily target for the industry.

And, or course, wind output was down, particularly in South Australia, where the market hit the cap on several occasions this week and which could be headed for a period of administrative pricing, particularly if the forecast prices later this week occur.

This has happened in South Australia before, most notably on multiple occasions in 2008 and 2009, which made the government determined to embrace the shift to renewables. Now it’s happening again, as the fossil fuel industry tries to have the last laugh on its way out of the market before the state reaches its goal of 100 per cent net renewables by 2027.

Battery storage is supposed to throw a bit more competition into the market. But the problem is that many of these assets are now owned or contracted to the very same energy giants that control the rest of the generation. If anything, it’s made it easier for them to control prices and profits.

And being in the grip of the big energy players doesn’t feel like a safe place to be at the moment, especially with gas prices at such highs – five times the price of other international markets – according to Tim Buckley, from Climate and Energy Finance. And it gives the Coalition plenty to crow about, something that is now taking hold in the minds of the public.

Buckley also wrote last week how gaming by the big gentailers exacerbated the outages of unplanned coal power plant breakdowns and the network outages.

“Coal power was unreliable and offline when it was needed and this was opportunistically gamed by AGL and EnergyAustralia,” he wrote on his LinkedIn page. “So when their executives bank their bonuses this year, consumers crushed by fossil energy price inflation can thank them for gouging us.”

“We need firmed renewables replacement capacity now. We have a climate crisis, an energy crisis and a cost of living crisis.

“We can solve all three by building firmed renewables. Consumers pay the price because investors won’t build new thermal power, but they can’t build new renewables if they can’t get them through our chronically dysfunctional, backlogged planning approval system. Governments need to accelerate evaluation and approvals. In NSW, it takes 10 years to approve.”

But as BloombergNEF notes in a new report released on Wednesday, investment in the sector remains slow and steady, despite the ambitious government targets.

“Sluggish grid buildout, lengthy permitting processes and the self-cannibalising nature of solar, especially from rooftop PV, remain the key challenges facing the sector today,” it notes of the market for big solar.

“Investment in the wind sector is picking up on the back of clear government policy, and greater demand in the market as coal assets start to retire. However, protracted permitting processes and slow grid expansion continue to act as headwinds in the sector.”

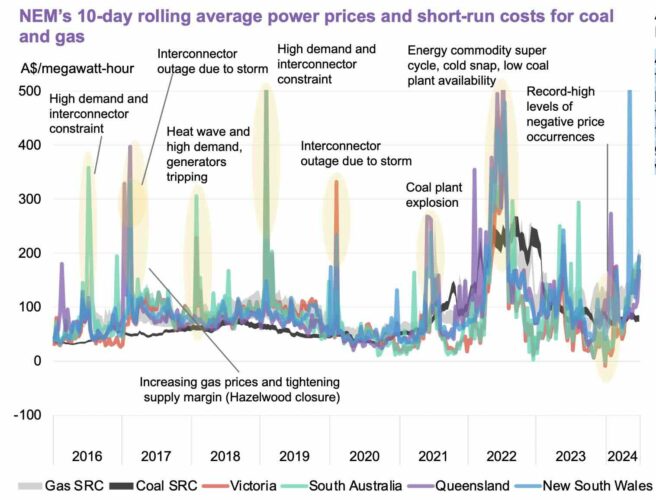

Battery storage and behind the meter solar (thanks to “stubbornly high retail tariffs) remain the strong points, but BloombergNEF also notes that average daily power prices in Australia’s main grid tend to follow the short-run costs (SRC) of coal and gas plants, which still make up roughly 60 per cent of all power in the NEM.

It notes in this graph above how nearly all the price spikes in recent years have followed some sort of incident which has reduced competition, often among fossil fuel generators themselves. But the average price follows that of the marginal cost of fossil fuels, because they are still in control of the market.

“Although most power plants have long- term supply agreements for fuel, a part of their generation is usually dependent on spot purchases, which often dictates power prices,” it notes.