The Federal Election has been run and won, with the Australian Labor Party (ALP) confident of securing enough seats to form majority government.

The wave of support for pro-climate candidates now provides a number of options for the ALP to implement its proposed improvements to the Safeguard Mechanism – triggering the greater contribution of the industrial sectors to Australia’s net zero emissions reduction target.

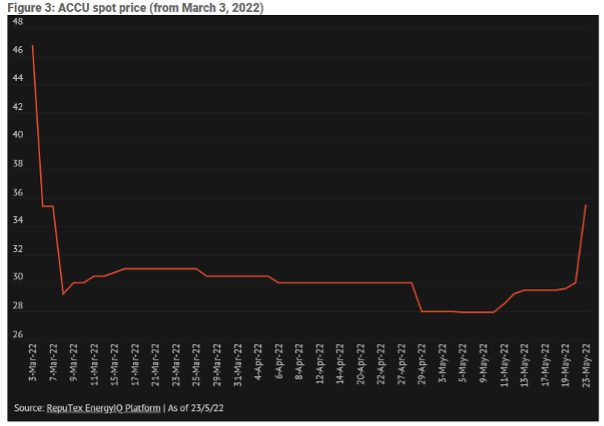

As flagged in our recent updates, the change of government will be supportive for the local carbon offset market, reflected in the return of positive sentiment to the ACCU spot market yesterday. In response to the election outcome, the ACCU spot price grew 18 per cent on Monday, closing at $35.50/t, up 5.50 from Friday’s close of $30/t.

Despite the market response, expectations that a change in government will “significantly increase” demand (and prices) for ACCUs are far from certain, with the local market facing a number of challenges that could impact medium-term price development.

This includes the role of proposed Safeguard Mechanism Credits (SMCs) – or ‘below-baseline’ units created by facilities under the Safeguard Mechanism – with the development of low-cost industrial credits likely to soften compliance and voluntary demand for ACCU offsets.

In addition, following changes to the ERF in March, the Australian carbon offset market now finds itself with a potential surplus of ACCU supply of from existing carbon farming projects. As proponents begin to exit their ‘fixed delivery’ contracts under the Emissions Reduction Fund (ERF), this surplus is likely to weigh on prices, subject to the timeline and magnitude of new sources of demand entering the market.

In this article, we present initial analysis of the impact of the federal election on the local ACCU market, including discussion of the political pathway for the Safeguard Mechanism, and the factors likely to shape medium-term price development.

Election 2022 – climate wave provides strong mandate for action

The ALP is currently confident of securing enough seats in the House of Representatives to govern in its own right. According to the ABC, the ALP currently holds 72 seats to the Coalition’s 52, with Others (independents) holding a record 15 seats. Twelve seats remain in doubt, with the party currently ahead in 78 seats across the country (a government must win 76 to form a majority).

Notably, the election outcome now provides the parliament with a clear mandate on climate action, with pro-climate candidates winning blue-ribbon Liberal seats of Kooyong and Goldstein in Melbourne, North Sydney, Wentworth and Mackellar in Sydney and Curtin in Perth, while the Greens appear likely to take the Queensland seats of Brisbane and Ryan. In total, the Liberal Party could see a loss of up to 20 MPs.

Treasurer Josh Frydenberg was among six Liberals to lose their seats to the teal movement, leaving Peter Dutton as the most likely to become the new Coalition leader.

Labor and the Greens appear set to hold a large progressive voting block in the new Senate as part of a major realignment of the upper house. The Greens appear set to secure 12 seats in the Senate, up from 9, while former Liberal Minister Zed Seselja looks set to be unseated by pro-climate independent, David Pocock.

While the final makeup will not be known for a few weeks, early results indicate that the Greens may hold the balance of power in their own right (or with David Pocock), providing a workable Senate for Labor.

What is the Safeguard Mechanism?

The Safeguard Mechanism commenced on 1 July 2016 under the Abbott Government, covering facilities with direct (scope 1) greenhouse gas (GHG) emissions of over 100,000 tonnes carbon dioxide equivalent (CO2-e) per annum.

In 2020-21 the Safeguard Mechanism extended to 212 facilities across the mining, oil and gas, manufacturing, transport, and waste sectors. While electricity generators are covered by the scheme, the sector is subject to a separate sectoral baseline. As a result, the electricity generation sector is assumed to be excluded from the scheme (and is now covered by separate ALP policy such as the Rewiring the Nation package).

Excluding the electricity sector, industrial facilities covered by the Safeguard Mechanism accounted for 137 million tonnes of CO2-e in FY21, or over one quarter (27%) of national emissions. Of the 137 Mt CO2-e of GHG emissions covered by the Safeguard Mechanism, approximately 61 per cent are from facilities in the mining, and oil and gas sectors (83 Mt in FY21).

Critically, while key sectors of the economy have begun to decarbonise, such as the electricity sector, industrial emissions are projected to increase to around 150 Mt in 2030 (under business-as-usual conditions), to be 26 per cent above 2005 levels.

This will see the industrial sector’s proportional share of national emissions grow to one-third (33%) by 2030, overtaking electricity as Australia’s largest emitting sector by the middle of the decade. Emissions reductions in the industrial sector will therefore be critical for Australia to meet any economy-wide emissions target.

Growth in covered emissions has been driven by the mining and oil & gas industries, in particular the rapid expansion of liquefied natural gas (LNG) export capacity, combined with the design of flexible emissions baselines under the current safeguard scheme.

In FY21, 93 per cent of facilities (198) reported covered emissions below their baselines, with just 14 facilities (7%) liable to reduce their net-emissions.

Notably, of the 171 facilities whose baselines were disclosed by the Regulator in FY21 (excluding 40 facilities on multi-year monitoring periods), over 70 per cent, or 121 facilities, are able to increase their FY21 emissions by 10 per cent or more before breaching their baseline – with some facilities able to more than double their emissions – reflecting the significant headroom built into the current scheme.

Safeguards 2.0: What improvements is ALP proposing

On December 3, the ALP announced its “Powering Australia Plan”, underpinned by policy measures for three key sectors of the economy – Electricity, Industry & Carbon Farming, and Transport.

RepuTex was engaged by the ALP to analyse the greenhouse gas emissions and economic impacts of the Powering Australia Plan. To access the full report click here.

The ALP policy framework includes improvements to the Safeguard Mechanism, adopting recommendations from the Business Council of Australia (BCA) for emissions baselines to be reduced “predictably and gradually over time”, in line with net-zero emissions. The following policy settings were modelled:

- The current eligibility threshold for the Safeguard Mechanism would be maintained at 100,000 tCO2 per annum (excluding electricity generation).

- The scheme was modelled to commence on 1 July 2023.

- Emissions baselines for covered facilities were re-set to reflect reported emissions (in absolute terms), declining in line with an aggregate annual emissions baseline reduction of approximately 5 Mt, reaching net-zero by 2050.

- Tradable Safeguard Mechanism Credits (SMCs) were modelled to be issued where an entity “beats” its emissions baseline, while facilities would be required to surrender credits equivalent to their “above-baseline” emissions.

- Liable entities may meet their obligations for “above-baseline” emissions by surrendering SMCs and/or ACCU offsets.

- Tailored treatment is assumed to be provided to emissions intensive trade exposed industries (EITEs) based on a comparative impact principle, informed by industry consultation and advice from the Department of Industry, Science, Energy and Resources (DISER) and the Clean Energy Regulator (the Regulator).

The current Safeguard Mechanism framework is therefore proposed to be transitioned into a ‘baseline and credit’ system, with the net-zero trajectory creating a gradual and transparent long-term signal for private sector investment in least-cost emissions reductions – in the form of internal emission reductions, industrial SMC trading, or ACCU offsets from the carbon farming sector.

We forecast that improvements to the Safeguard Mechanism, supported by financing under the ALP’s National Reconstruction Fund (NRF), will deliver 213 Mt of abatement between 2023-30. Combined with other policy leavers (such as the Rewiring the Nation package), this is modelled to achieve 43% reduction on 2005 levels by 2030.

Could the Senate negotiate a more ambitious target?

Potentially, however the Senate may not be a factor.

Prior to the election the ALP ruled out any changes to its 2030 emissions reduction target in the event it is forced to negotiate with other parties to form government. Based on current numbers, the ALP appears to have avoided such an outcome, with the party on track for a majority in the house its own right.

The Senate may provide a more challenging environment for the ALP should it be required to work with the Greens to legislate its Safeguard Mechanism framework. In theory, this could pave the way for more ambitious settings to be built into the ALP’s policy framework. In practice, however, the ALP will have a number of pathways to potentially avoid any policy compromises.

Regulation is an option in place of legislation

Outside of legislative pathways, the ALP has previously stated it would enact its climate change policy unlegislated, if need be, rather than amend its position.

This remains a live option, with current emissions baselines overseen via regulation (the National Greenhouse and Energy Reporting (Safeguard Mechanism) Rule 2015), providing the Minister of the day with power to update baselines.

This power has historically been used to relax baseline settings, such as recent changes to implement emissions intensity baselines, providing facilities with the option to select more lenient emissions benchmarks.

This provides the ALP with considerable flexibility in setting more ambitious baselines, and enacting the scheme quickly ahead of the July 2023 start date, following consultation with industry.

While the Minister’s regulatory power provides the ALP with considerable leverage to set more ambitious emissions baselines, legislative amendments are expected to be required to the existing regulatory scheme (the National Greenhouse and Energy Reporting Act 2007, the Australian National Registry of Emissions Units Act 2011 and the Carbon Farming Initiative Act) to allow for:

- The creation of Safeguard Mechanism Credits

- Rules for Safeguard Mechanism Credit ownership and transfer; and

- The surrender of Safeguard Mechanism Credits by covered facilities to meet their compliance obligations.

As a result, the ALP may elect to legislate all or part of its Safeguard Mechanism policy framework. Should it take a legislative route, the Liberal Party may provide a willing partner on climate policy, with one senior Liberal moderate telling the Australian Financial Review it is likely that enough moderate senators would cross the floor to back the ALP’s climate policy if the Greens proved to be inflexible. The Liberal MP noted: “It’s hypothetical, but after Saturday we’re not going to die in a ditch on this [inaction on climate change]. To hell with it,”.

A bi-partisan agreement with the Liberal Party (broader Coalition support may be less likely) may draw an end to the ‘climate wars’, enabling the Opposition to neutralise an obvious policy weakness, while providing the market with improved policy certainty to support long-term investment – a key ingredient for market success.

If a legislative pathway with the Greens is preferred, support for the ALP’s short-term ambition may enable the Greens to press for a new interim target, and regular review of climate science (similar to Zali Steggall’s climate bill). Moreover, the Greens could elect to play a constructive role in Safeguard Mechanism market design (such as rules for the use of offsets/SMCs, new entrants, rolling target reviews, and so on), enabling the development of a robust, enduring bi-partisan (potentially tri-partisan) market for industrial emissions reductions – with scalable ambition.

How has the market reacted to change of government?

As flagged in our recent updates, the change of government will be supportive for the local carbon offset market, reflected in the return of positive sentiment to the ACCU spot market. In response to the election outcome, the ACCU spot price grew 18 per cent on Monday, closing at $35.50/t, up 5.50 from Friday’s close of $30/t. The ACCU price remains well below the record high of $57.50/t recorded under the former Coalition government in late January.

Three spot trades for Human Induced Regeneration (HIR) projects were also recorded at $37.50, a 5 per cent premium to the daily spot price. This continues to reflect increasing price stratification across ACCU project categories, underpinned by demand from voluntary buyers. RepuTex last week released two new indexes to track the daily premium for key ACCU methods, including HIR and Savannah Burning projects.

Where to next – will prices continue to rise?

Not necessarily.

While short-term sentiment is expected to remain positive, downside price risk remains ever-present. To this end, we continue to forecast that local ACCU price will be influenced by two key factors: the significant availability of ACCU supply from current projects; and the creation of new industrial SMC units where an entity “beats” its emissions baseline under the Safeguard Mechanism.

Price development will therefore depend on the timeline and scale of new demand entering the market, and the interaction of this demand with expected supply.

As announced by the Former Energy Minister Angus Taylor on March 4, holders of fixed delivery carbon abatement contracts (CACs) under the Emissions Reduction Fund will now be given the option to exit their contracts with the Commonwealth to access higher prices in the secondary market. We forecast this could see total ACCU availability grow to over 180 million by 2030 (from projects currently being credited e.g., issuance from optional and fixed delivery CACs, and registered uncontracted projects), subject to the prevailing market price.

Such a large pool of available supply is likely to weigh on market prices, particularly in scenarios where new sources of demand for ACCUs under the ALP’s Safeguard Mechanism 2.0 framework are lower than expected – for example should there be widespread creation of industrial SMCs. Reduced demand for ACCUs (usurped by SMCs) could therefore limit the market’s ability to absorb the expected surplus of ACCUs that will be issued over the next 5-10 years.

This pool of surplus ACCU supply may also support a more ambitious emissions target framework, with Australian carbon offsets now plentiful and well priced relative to high quality international alternatives [EnergyIQ: international offset prices].

Expectations that a change in government will “significantly increase” demand for ACCUs is therefore far from certain, with SMC creation – informed by policy design, industrial abatement costs, and investment decision making – to have considerable implications for forward ACCU price and market dynamics, even under a more supportive ALP policy environment.

Please refer to our latest Carbon Market Outlook for more detailed discussion of our ACCU price, supply and demand scenarios, including the potential impact of the Safeguard Mechanism on our medium- and long-term price expectations.

This article was initially published under RepuTex’s Australian carbon intelligence service.