Here are the state by state rooftop solar PV scenarios included in the Australian Market Operator’s 2015 National Electricity Forecasting Report. In almost every instance, the medium and long term forecasts have been upgraded significantly from last year.

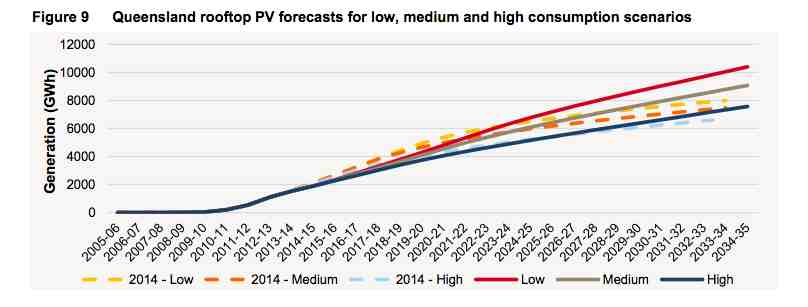

We begin with Queensland, where AEMO says that over the longer term revisions to its commercial PV forecasts dominate the growth in its longer term projections, resulting in higher forecasts than the previous NEFR. It says solar PV will shift the time of maximum demand from 17:00 to 19:30 over the forecast period.

And these are the range of scenarios from AEMO, from low to high, and how they have changed since last year.

In NSW, the uptake of rooftop solar is the second biggest in the country, but because of its relatively low penetration, it does not actually shift the time of maximum demand, according to AEMO’s forecasts.

And these are the range of scenarios from AEMO, from low to high, and how they have changed since last year.

And these are the range of scenarios from AEMO, from low to high, and how they have changed since last year.

In Victoria, as in other states, AEMO notes that residential rooftop PV uptake continues to be driven by the federal Small-scale Renewable Energy Scheme (SRES) and the “increasing economic viability” of rooftop PV.

It also notes that the programs that incentivised the historical uptake have helped to establish a local industry and drive a reduction in PV technology and installation costs.

The uptake in the commercial sector is being driven by a combination of programs such as the Clean Technology Investment Fund and SRES, as well as the continued decrease in PV costs. This is making the business case more attractive.

And these are the range of scenarios from AEMO, from low to high, and how they have changed since last year.

These are the forecasts for Tasmania, which has the lowest take-up of solar in any state.

Please see separate story for forecasts for South Australia. The state of Western Australia is not included in AEMO forecasts, as it is run by a different market operator. The ACT is included in NSW data.